For a lot of would-be first-time buyers, affordability is the wall. The income is steady, the desire is there, but the down payment and the monthly payment on a single salary just don’t line up with the price of a house. So some buyers have stopped trying to clear that wall alone. They’re teaming up with someone else and buying together, and co-buying a home is turning “someday” into a move-in date.

It isn’t a fringe move anymore, and it isn’t only for couples. Friends, siblings, unmarried partners, and parents buying with an adult child are pooling their money to get a foot in the door. In a market like Memphis, where the price of entry is already friendlier than most metros, two incomes working together can cover a lot more house than either person could reach alone.

This is a real path, not a workaround. But it comes with its own set of decisions, and the buyers who do it well treat it like the financial partnership it is. Here’s how co-buying works, why it’s catching on, and what to settle before you sign anything.

The dream is alive, the math just isn’t working

Younger buyers haven’t given up on owning a home. Far from it. Surveys keep putting homeownership near the top of the list of life goals for Gen Z and millennials. The wall isn’t desire. It’s the numbers.

By one widely cited figure from FirstHome IQ, 73% of Gen Z and millennial buyers point to affordability as the reason homeownership isn’t a near-term priority. And it shows in who’s buying. First-time buyers now make up just 21% of all home purchases, the lowest share since the National Association of Realtors started tracking it in 1981. A whole generation is stuck in the gap between wanting a house and affording one.

Co-buying is one of the ways people are closing that gap. It doesn’t change the price of the house. It changes how many shoulders carry it.

What co-buying a home means

Co-buying means purchasing a home with another person you’re not married to, and sharing the ownership, the loan, and the monthly costs. You combine incomes for the application, split the down payment, and divide the mortgage, taxes, insurance, and upkeep once you’re in.

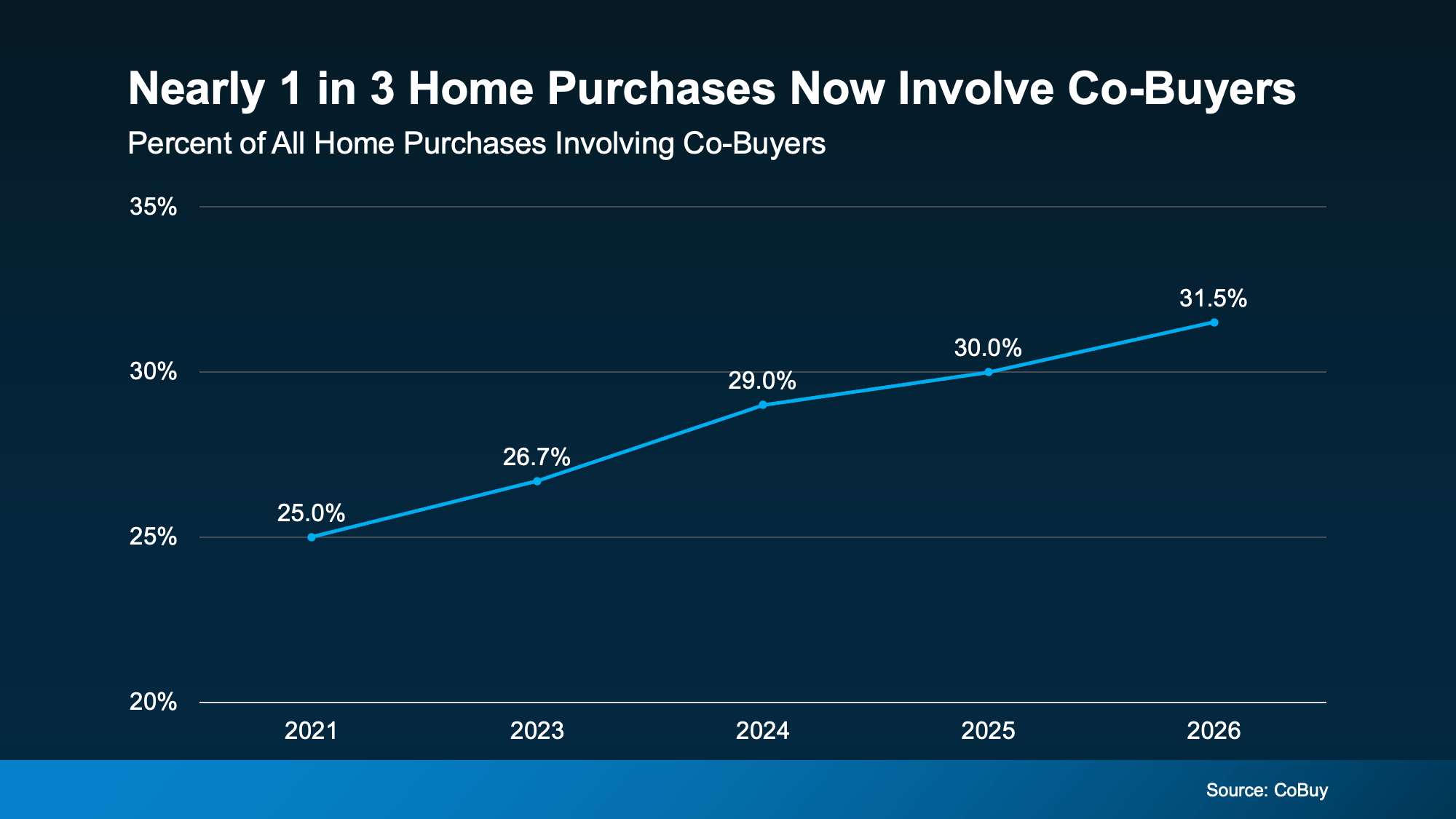

The trend has real scale behind it. CoBuy.io estimates that 64 million Americans now co-own a home with someone they aren’t married to, and that close to a third of home purchases involve co-buyers. Some of that is couples who haven’t married. A lot of it is friends and family deciding that two names on the deed beats waiting another five years for one.

The arrangement is flexible. Two friends splitting a duplex-style setup, two siblings inheriting the buying power their parents never had, a parent helping an adult child qualify while building equity instead of cosigning a lease. The common thread is simple: more than one person bringing money to the table.

Why buyers are teaming up

The appeal comes down to what a second income and a second savings account do to the math.

The fastest change is the timeline. Two people saving toward one down payment get there in roughly half the time, which means less time renting and more time building equity in something that’s yours. For buyers watching prices grind slowly higher, getting in sooner beats saving alone for years while the target keeps moving.

Then there’s buying power. With two incomes pointed at one mortgage, the price range opens up. That can mean a better neighborhood, a house that fits instead of one you’ll outgrow in two years, or a place in one of the stronger school zones that would be out of reach on a single salary. Teaming up often means getting the home you want rather than the one you can barely stretch to.

Qualifying gets easier too. Lenders look at the combined income of everyone on the loan when they calculate your debt-to-income ratio, the number that decides how much you can borrow. A second qualified borrower can be the difference between an approval and a polite no. And once you’re in, splitting the payment, the property taxes, and the cost of a new water heater two or three ways can land you below what either of you was paying in rent. The case for buying over renting gets stronger when the carrying cost is shared, and the equity you build instead of handing to a landlord compounds for everyone on the title.

How a co-buying mortgage works

This is the part the excitement tends to skip, and it’s the part that matters most. When you co-buy, everyone on the loan is usually on the title, and everyone on the loan is fully responsible for it. Mortgages are what’s called joint and several liability, which means each borrower is on the hook for the entire payment, not just their share. If your co-buyer stops paying, the lender looks to you for all of it, and it’s your credit that takes the hit alongside theirs.

Credit is the other piece people underestimate. Lenders typically price the loan off the lowest median credit score among the borrowers, not the average. So if one of you has excellent credit and the other is still rebuilding, the rate you get reflects the weaker score. It’s worth pulling both credit reports and talking honestly about debts and history before you shop, because the loan treats you as a single financial unit even though your finances are separate.

The upside of that same rule is the qualifying power covered above. All the income counts, which is what makes the approval possible in the first place. The trade is that all the risk is shared too. Going in clear-eyed about that is the whole game.

How you hold the title matters

Two co-buyers can own the same house in very different ways, and the one you choose decides what happens when life changes.

Joint tenancy splits ownership equally and includes a right of survivorship, meaning if one owner dies, their share passes automatically to the other. That fits couples and close family who want the simplest path. Tenancy in common is the more common choice for friends and business-minded co-buyers, because it lets you hold unequal shares, say 60/40 if one person put down more, and each owner can sell or will their share independently. If you’re putting in different amounts of money, tenancy in common is usually the structure that keeps it fair. A real estate attorney can walk you through which one fits your situation before closing.

Put it in writing before you buy

A co-ownership agreement is the single smartest thing co-buyers do, and skipping it is the most common regret. Think of it less as a legal formality and more as the game plan for your investment, written while everyone still likes each other and nobody’s under pressure.

A good agreement spells out the things that feel obvious now and won’t later. How is ownership split, and does it match who paid what? Who covers which bills, and how do you handle a month when one person is short? What happens if someone wants out, gets a job in another city, gets married, or simply changes their mind? Most agreements give the staying owner a first right to buy the other out, set a method for valuing the home so there’s no fight over the number, and lay out how you’ll sell if it comes to that. The hard questions, including what happens if an owner dies or can’t pay, are far easier to answer on paper in advance than in a crisis. Spend the money on an attorney to draft it. It’s cheap insurance against losing both the house and the friendship.

Where co-buying makes sense in Memphis

The local market is part of why this works as well as it does here. Memphis and its suburbs still offer entry points below what you’d pay in Nashville, Atlanta, or Charlotte, and Tennessee’s lack of a state income tax stretches every paycheck a little further. That affordability edge is exactly what makes co-buying powerful, because two incomes go further in a market that’s already reasonable than in one where you’re both priced out to begin with.

It’s the same affordability story playing out across the metro. As housing affordability in the second half of 2026 holds up and more listings come online, buyers have more room to choose, and co-buyers get to aim higher together. Two people teaming up can realistically look at homes in Germantown or Collierville, with their school zones and steadier values, that a solo first-timer would have to skip. For anyone working through the basics, our guide to buying your first home in Memphis pairs naturally with a co-buying plan.

The risks worth weighing

Co-buying isn’t free of downside, and the honest version includes the parts that can go wrong. You’re tying your biggest asset and your credit to another person’s choices for years. If they lose a job, run into debt, or want out before you’re ready, your finances feel it directly. Selling a co-owned home takes agreement from everyone on the title, so a stalemate can trap you in a house you want to leave.

And there’s the relationship itself. Money has a way of testing friendships and family ties, and a missed payment or a disagreement over a renovation can sour both the deal and the bond. None of this is a reason to avoid co-buying. It’s the reason to do it only with someone you trust, whose finances you understand, and with the agreement in writing before you start. The buyers who get burned are almost always the ones who treated a financial partnership like a casual favor.

Whether co-buying is your way in

Affordability is real, but it doesn’t have to mean waiting on the sidelines indefinitely. For the right pair of buyers, with aligned goals, honest finances, and a plan in writing, co-buying turns a down payment that felt years away into a closing date you can circle on the calendar. It’s how a lot of first-time buyers are finally getting in.

If you’re wondering whether it could work for your situation, that’s a conversation worth having with someone who knows the local market. Reach out to our team and we’ll help you figure out your path to owning, whether you’re going it alone or teaming up to make the numbers work. You can also start your home search whenever you’re ready to see what’s out there.