(Updated 12/16/25)

So you snagged a mortgage rate under 3% a few years back. First off, congratulations. That’s honestly impressive, and you should feel good about that decision. With rates sitting above 6% these days, I totally get why you’d want to hold onto that golden ticket for as long as humanly possible.

But here’s the thing I want to chat with you about today. What if that amazing rate is actually keeping you stuck in a situation that’s no longer working for you? I know that sounds counterintuitive, but stick with me here. Let’s explore whether staying put is really the financially savvy move you think it is.

The Real Question

When people talk about moving, the conversation usually starts and ends with mortgage rates. But honestly, that’s looking at it backward. Most folks don’t wake up one day and think, “You know what? I want a higher interest rate!” That’s not how life works.

People move because their lives change. Your family grows. Kids head off to college. You land a new job across town. Your elderly parents need to move in with you. Maybe you’ve just outgrown your space, or perhaps you’re rattling around in a house that’s way too big now.

So instead of asking “Why would I give up my amazing rate?” try flipping it around. Ask yourself this instead: Where do you honestly see yourself five years from now?

A Hard Look at Your Future

Close your eyes for a second and really picture the next few years of your life. What does that look like? Are you planning to expand your family? Do you have teenagers who’ll be leaving for college soon? Is retirement creeping closer than you’d like to admit? Maybe you’re already tripping over each other in your current space.

If you can picture any major life changes on the horizon, that low rate might not be doing you the favor you think it is. Because here’s what a lot of homeowners don’t realize until it’s too late.

The Hidden Price of Waiting

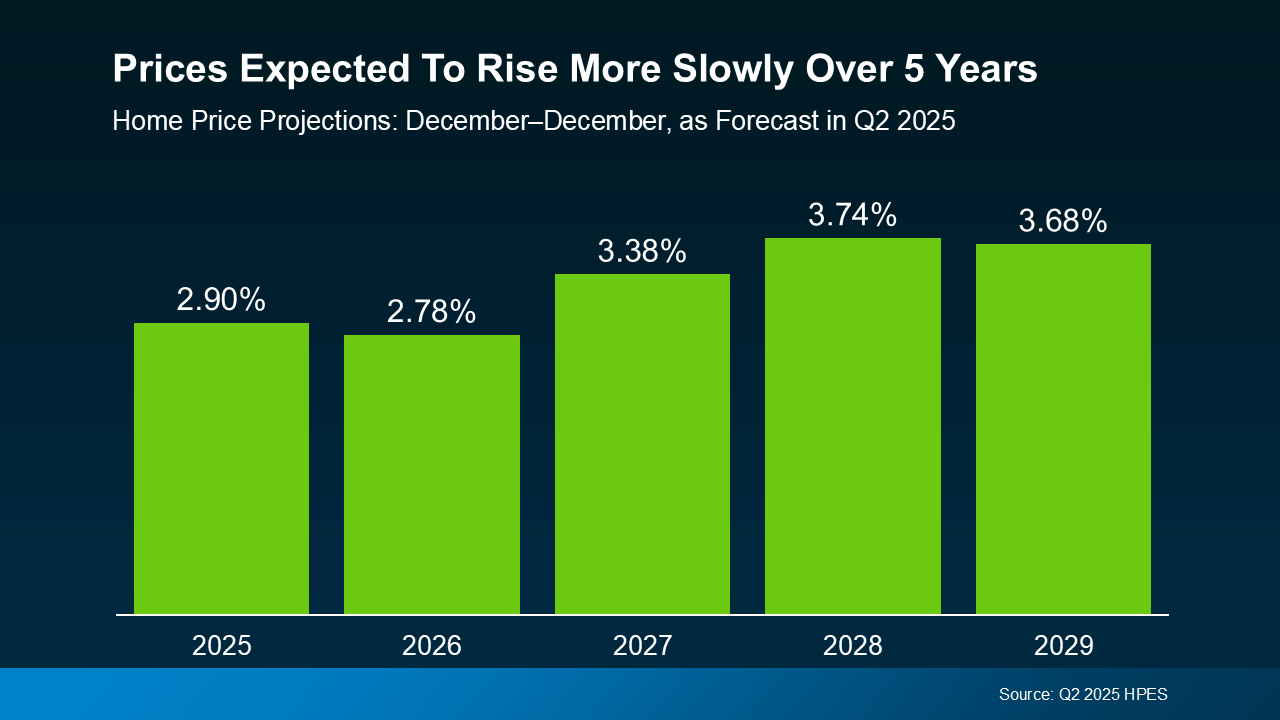

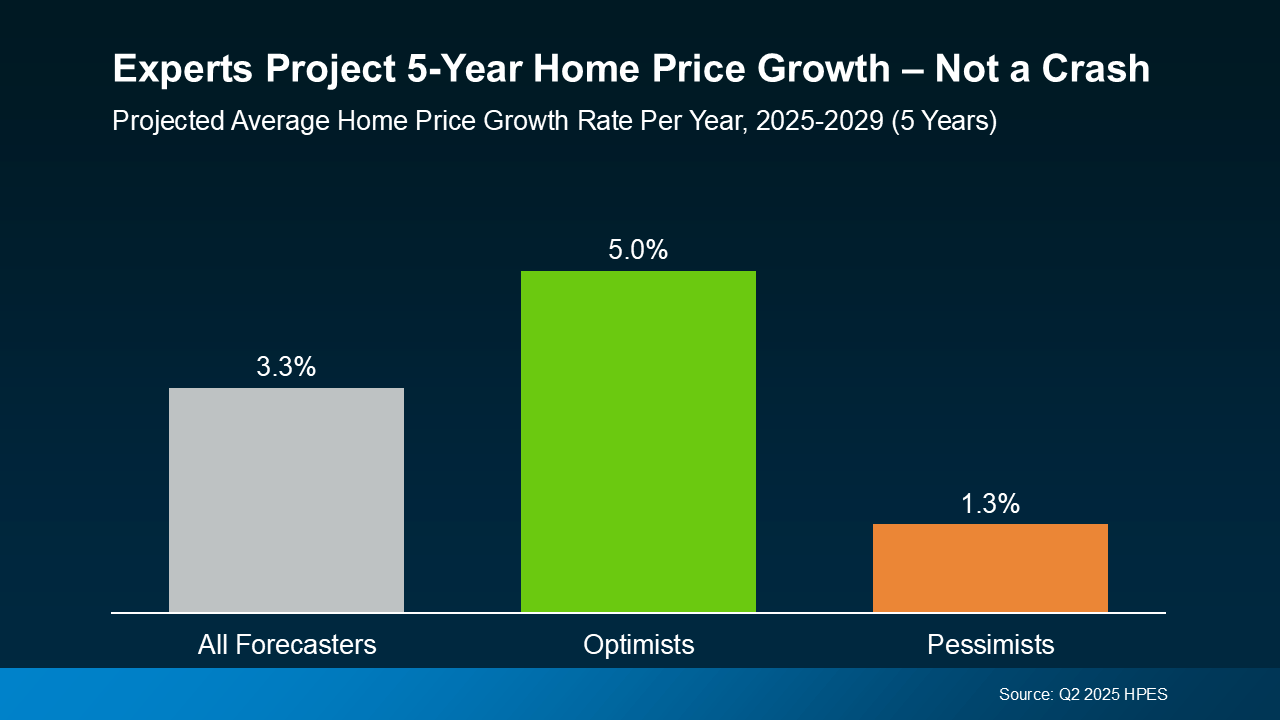

Home values don’t just sit still while you’re debating whether to move. They keep climbing, year after year. And that means the house you’re eyeing today will cost substantially more down the road.

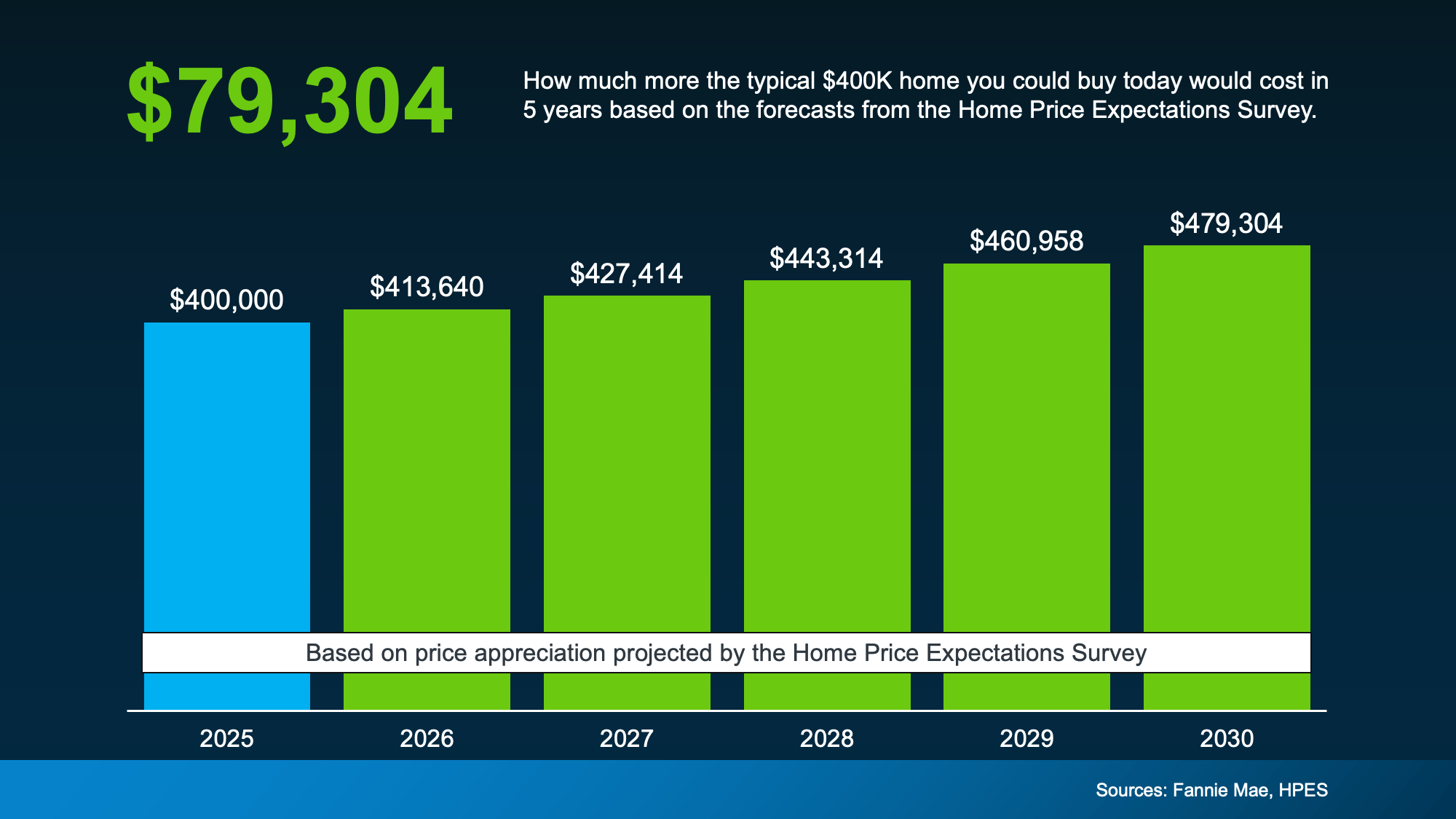

Let me break this down with some real numbers because I think it’ll surprise you. Say you’re looking at homes around the $400,000 mark right now. Based on what housing experts are predicting, if you wait five years to make that purchase, you could be looking at paying nearly $80,000 more for a comparable property. Eighty thousand dollars. That’s not pocket change.

Think about what else you could do with $80,000. That’s a college fund for your kids. That’s a serious chunk of your retirement nest egg. That’s multiple dream vacations. The point is, every year you wait, that future home gets more expensive. The gap keeps widening.

Mortgage Rate Reality Check

Now, I know what you might be thinking. “But rates will come back down eventually, right? Maybe I should just wait for that.” I wish I had better news for you, but I need to be straight with you here.

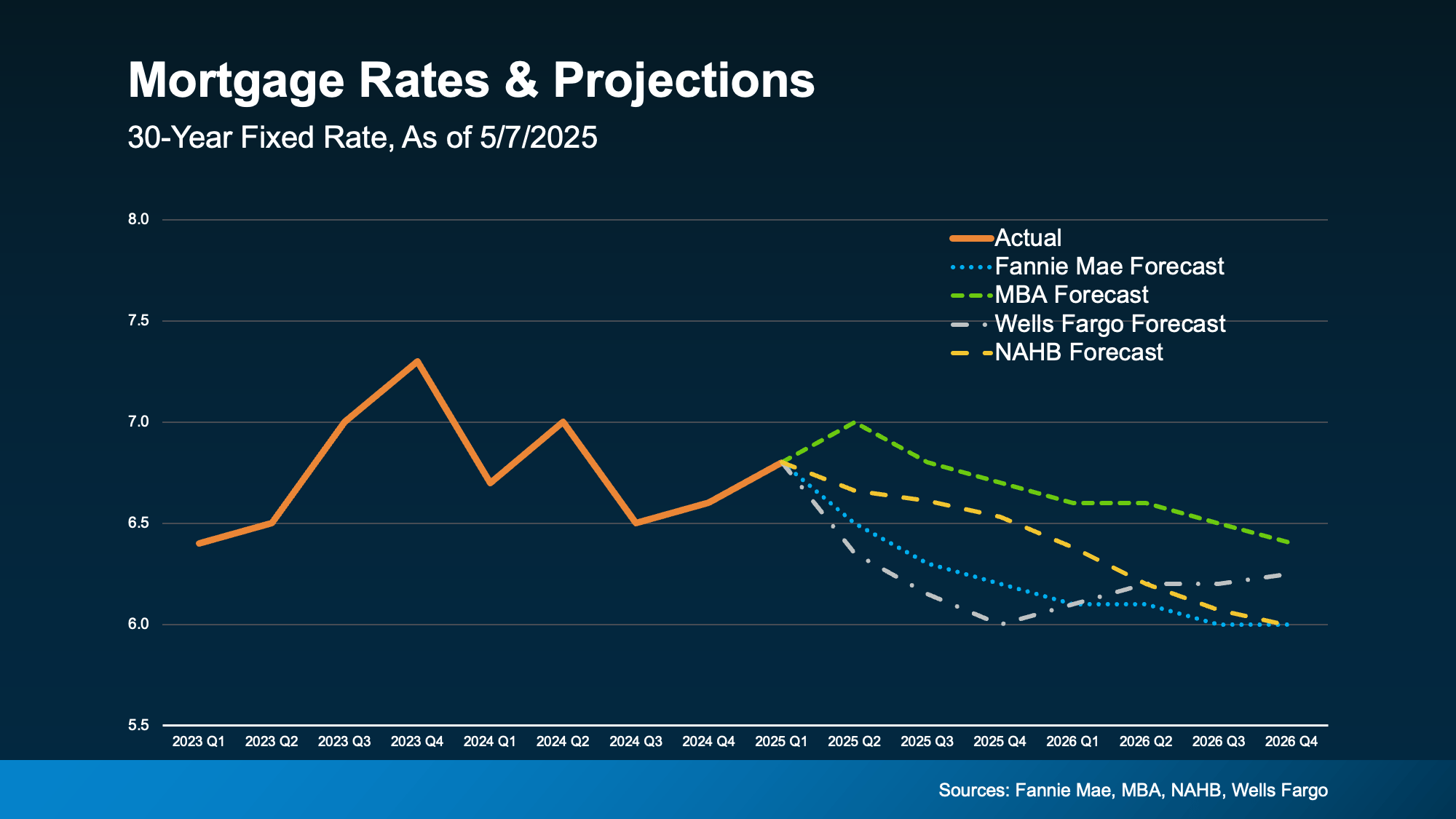

Virtually every major housing expert and economist out there agrees on one thing. We’re not going back to the days of 3% or even 4% mortgage rates. Those days are behind us. Could rates drop a bit from where they are now? Sure, most forecasts show them settling somewhere in the 5.5% to 6% range over the next few years. But we’re not looking at a dramatic plunge.

The Federal Reserve, major banks, housing economists, they’re all singing the same tune. That era of ultra-low rates was a unique moment in history, driven by extraordinary circumstances. Waiting around hoping for a return to 3% rates is like waiting for gas prices to drop back to what they were in 1995. It’s just not realistic.

When Staying Becomes More Expensive Than Moving

Here’s something that doesn’t get talked about enough. Just because you have a low monthly mortgage payment doesn’t mean your house is actually saving you money. Let me explain what I mean.

Older homes come with their own set of expenses that add up fast. You’ve got ongoing maintenance that never really stops. Things wear out. Systems break down. And if your home doesn’t fit your needs anymore, you start throwing money at it trying to make it work.

Renovation Trap

Maybe you’re constantly remodeling, trying to squeeze more functionality out of your space. Adding a home office here. Converting a closet into storage there. Finishing the basement because you desperately need more room. These projects aren’t cheap, and they often don’t add enough value to make the investment worthwhile.

I’ve seen people pour $50,000, $75,000, even $100,000 into homes trying to make them work, when that money could have been a substantial down payment on a place that already meets their needs. The math on that rarely works out in your favor.

The Opportunity Cost

There’s also the daily cost of living in a space that doesn’t work for you. Are you constantly reorganizing just to make things fit? Have you stopped having friends over because your place feels too cramped? Are you spending money on storage units because you’ve run out of space?

These aren’t just financial costs, they’re quality-of-life costs. And they add up in ways that are harder to see on a spreadsheet but are very real in how you experience your daily life.

What Getting Educated Means

Look, I’m not here to push you into making a decision you’re not ready for. But I am going to encourage you to get educated about your options. And the best part? This education is completely free.

Talk to a Real Estate Agent

A good local agent can give you a realistic picture of your current home’s value and what you could actually afford in today’s market. They know your neighborhood, they understand the inventory, and they can show you what’s actually out there that might fit your needs better.

This conversation costs you nothing, and you’re not committing to anything. You’re just gathering information. Think of it as doing your homework before making one of the biggest financial decisions of your life.

Talk to a Mortgage Lender

This is equally important. A lender can show you exactly what your payment would look like with today’s rates, based on your specific financial situation. They’ll look at your credit, your equity, your income, and give you real numbers to work with.

But here’s what a lot of people don’t know. There are strategies that can help make the math work better in your favor. Rate buydowns, where you pay points upfront to lower your rate. Adjustable-rate mortgages that start lower and might make sense if you don’t plan to stay forever. Different loan terms that can adjust your monthly payment.

A knowledgeable lender will walk you through all these options and help you understand the trade-offs. They can also calculate your break-even point, which tells you how long it would take for a move to make financial sense given all the costs involved.

Home Equity

Here’s something that might surprise you. While you’ve been sitting on that low rate, chances are you’ve also been building up some serious equity in your current home. Depending on when you bought and where you live, you might have way more buying power than you realize.

That equity becomes your down payment on your next place. It can significantly offset the impact of a higher rate because you’re borrowing less money overall. Sometimes, the equity alone can make a move financially viable even with higher rates.

But you won’t know what you’re working with until you have those conversations with an agent and lender. They’re the only ones who can give you a clear picture of your actual financial position.

The Timing Concern

One of the biggest fears people have about moving is the logistics. “What if I sell my house but can’t find something to buy? What if I’m stuck homeless with my stuff in storage?” I get it. That’s a legitimate concern.

But here’s the thing, you have way more flexibility than you might think. Yes, contingent offers (where you only buy if you sell first) can be tougher in competitive markets. But there are other strategies that give you breathing room.

You can list your current home, accept an offer, and then negotiate a closing date that’s 60 or 90 days out, which gives you time to find your next place. You can include a rent-back provision where you pay the buyers to stay in your home for a month or two after closing while you complete your purchase. Some sellers even arrange temporary housing as a bridge between homes.

Your agent can help you structure a strategy that works for your specific situation. The point is, you don’t have to feel trapped by the logistics. There are ways to make the transition work.

A Personal Story That Might Resonate

Let me share something with you. There’s a family I know, and the mom described herself as the “financial one” in the household. She was the spreadsheet person, the one who ran all the numbers and kept everyone on budget. They had locked in a rate under 3% on their 1,400 square foot home.

Meanwhile, her family was dreaming out loud. The kids wanted a pool. Everyone wanted more space. They talked about possibilities. But she couldn’t get past that interest rate. In her mind, the math didn’t work. They’d already invested heavily in their current home too, new AC, new roof, screened porch, all those updates that are supposed to make a house feel perfect.

But something was still missing. The walls felt like they were closing in. Then one day, they found the right property. At first, she resisted hard. The numbers in her head screamed that it was the wrong decision. But then she watched her family light up. She saw them excited about picking out design features. She saw the pride of ownership in a space that actually fit them. She watched them use the community pool without the maintenance headache of owning one.

Here’s what she said looking back: The happiness and sense of ownership her family feels now far outweighs the interest rate she was clinging to. Sometimes the best investments aren’t just about the numbers on paper. Sometimes they’re about your family’s everyday joy and quality of life.

I’m not saying everyone should do what they did. But I am saying that when you’re making a decision this big, you need to look at the whole picture, not just one number on a loan document.

The Benefits of a Better-Fitting Home

Let’s talk about what you might actually gain from moving to a home that’s a better fit. Because it’s not just about square footage or fancy features.

Energy Efficiency Savings

Newer homes are typically way more energy-efficient than older ones. Better insulation, more efficient HVAC systems, modern windows, all of this adds up to lower utility bills month after month. Depending on where you live and how old your current home is, this could save you hundreds of dollars monthly.

Lower Maintenance Costs

When you move into a newer home, you’re not dealing with the constant maintenance parade of an older property. New roof. New water heater. New appliances. New HVAC system. These things typically come with warranties, and they’re not going to fail on you anytime soon. That peace of mind has real value.

Better Functionality

Modern homes are designed differently than homes built 20 or 30 years ago. Open floor plans. Home offices. Better storage solutions. Larger primary suites. These aren’t just luxuries, they reflect how people actually live today. When your home works with your lifestyle instead of against it, that’s worth something.

Mental and Emotional Benefits

Don’t underestimate the value of loving where you live. Coming home to a space that feels right, that has room for everyone to spread out, where you can comfortably entertain friends and family, that impacts your daily happiness in ways that are hard to quantify but very real.

Current Market Realities

As of late 2025, mortgage rates are hovering in the mid-6% range for most borrowers with good credit. That’s roughly double what people were getting a few years ago, and I’m not going to sugarcoat it, that hurts when you’re comparing numbers.

But here’s some context that’s important. Interest rates sitting in the 6% to 7% range isn’t historically unusual. If you look at mortgage rate history over the past 40 or 50 years, what we’re seeing now is actually closer to normal. The 3% rates were the outlier, not what we have today.

Does that make it easier to swallow? Maybe not. But it does help put things in perspective. Generations of homebuyers built wealth through real estate with rates in this range and higher. It’s still possible to make smart real estate moves in this environment.

Running Your Own Numbers

Here’s my challenge to you. Stop thinking in hypotheticals and get some real numbers to work with. Schedule those conversations with an agent and lender. Give them permission to show you what’s actually possible.

Ask them to run specific scenarios:

- What’s my home worth right now?

- How much equity do I have after paying off my current mortgage?

- What would my payment be on a $400,000 home with 20% down at today’s rates?

- What about with 30% down using more of my equity?

- How does a 15-year mortgage change the picture versus a 30-year?

- What would a rate buydown cost, and how much would it save me monthly?

Once you have real numbers in front of you, you can make an informed decision instead of guessing or going off general assumptions that might not apply to your specific situation.

The Lock-In Effect Is Real

What you’re experiencing has a name in the housing industry. They call it the “lock-in effect,” and it’s having a measurable impact on the entire market right now.

Research shows that the vast majority of current homeowners, something like 99%, have mortgage rates below the current market rate. More than a quarter of homeowners have rates at or below 3%. Almost three-quarters are below 4%.

This has created a really unusual situation where inventory is constrained because people don’t want to sell. New listings in some markets have dropped by 40% or more compared to typical years. This lack of inventory is one reason prices keep climbing, which creates more urgency for people who do want to move.

Some homeowners are finding creative solutions. They’re keeping their low-rate properties and converting them to rentals when they move. That way, they preserve that great financing while still getting the new home they need. It’s not the right move for everyone, but it’s an option worth considering if you have the financial capacity to manage a rental property.

Your Rate Was Smart Then, But What About Now?

Nobody’s questioning whether getting a 3% rate was smart. It absolutely was. You made a great decision based on the market conditions at that time. Give yourself credit for that.

But being smart with your money isn’t about making one good decision and then never revisiting it. It’s about continually evaluating whether your financial choices still make sense for where you are now and where you’re headed.

The mortgage that was perfect for you three years ago might not be the right financial choice for your life today. And that’s okay. Circumstances change. Needs evolve. Smart money management means being willing to adapt when it makes sense to do so.

What Financial Advisors Say

If you talk to financial planners and real estate economists, most of them will tell you the same thing. They’re not encouraging people to jump ship from low rates just for the sake of it. But they are encouraging people to make decisions based on their life needs, not just their interest rate.

A 3% mortgage on a home that doesn’t fit your life isn’t necessarily better than a 6% mortgage on a home that does. The “best” financial decision is the one that balances all factors, including your quality of life, your family’s needs, and your long-term goals.

Some advisors also point out that home equity is a form of savings. If you’re sitting on $200,000 in equity in a home that’s making you miserable, that’s not smart money management. That’s being penny-wise and pound-foolish.

Questions to Ask Yourself

Before we wrap up, I want to leave you with some questions worth pondering. Be honest with yourself about the answers:

How much are you spending annually on maintenance and repairs to keep your current home functional? If you added it up over the next five years, what would that total look like?

Are you constantly compromising on how you live because your space doesn’t work? What’s the cost of that, not just in money but in stress and daily frustration?

If you knew for certain that you’d be moving within five years, would you still make the same decision to stay put now? Or would you move sooner rather than later to take advantage of today’s prices?

What opportunities are you missing by staying in your current location? A shorter commute? Better schools? Closer to family? A community that better fits your lifestyle?

If you remove the mortgage rate from the equation entirely, would you still want to live in your current home? If the answer is no, that tells you something important.

Make the Decision That’s Right for You

Look, I’m not going to tell you whether you should move or stay. That’s your decision, and it depends on a whole bunch of factors that are unique to your situation.

What I am saying is that you deserve to make that decision based on complete information, not just one piece of the puzzle. Your mortgage rate is important, sure. But it’s not the only thing that matters. It might not even be the most important thing when you look at the bigger picture.

The smartest thing you can do right now? Get educated. Have those conversations. Run the numbers. Look at real properties that interest you. Understand what moving would actually cost and what it would get you. Then you can make a choice you feel confident about, whatever that choice turns out to be.

Your low mortgage rate was a win, no question about it. But if you’re feeling stuck, cramped, or compromised in your current home, it might be time to look beyond that one number and consider the full picture.

Home prices are climbing every year. Expert forecasts suggest rates aren’t dropping back to 3% anytime in the foreseeable future. Meanwhile, your life is happening right now, not five years from now. The question isn’t really “Why would I move?” It’s more like “When should I move?” And for some people, the answer might be sooner than they think.

The only way to know for sure is to do your homework. Talk to professionals who can give you real numbers based on your actual situation. Look at what’s available in your market. Calculate the true cost of staying versus moving. Then make an informed decision that takes everything into account.

You were smart enough to lock in that great rate. Trust yourself to be smart enough to figure out what the right move is now. And remember, sometimes the wisest financial decision is the one that improves your life, not just the one that looks best on a spreadsheet.

Whatever you decide, make sure it’s based on the full picture of your life, your goals, and your genuine needs. That’s how you make money decisions you won’t regret, regardless of what the interest rates are doing.