There’s something magical about the start of a new year. It’s like turning to a blank page in your favorite notebook, full of possibility and promise. For many of us, this is when we start imagining what the next twelve months could look like, and sometimes that vision includes a completely new address.

If you’ve been thinking about buying or selling a home this year, you’re definitely not alone. The new year brings a unique energy that makes big decisions feel a little less scary and a lot more exciting. But here’s the thing—turning that dream into reality takes more than just wishing. It requires some planning, honest reflection, and the right team in your corner.

Let me walk you through everything you need to know about making your real estate goals happen in 2026, whether you’re looking to buy your first home, upgrade to something bigger, or finally downsize to that cozy bungalow you’ve been eyeing.

Understanding Your Real Motivation

Before you start scrolling through listing photos at midnight (we’ve all been there), you need to get crystal clear on why you want to move. I’m not talking about surface-level reasons here. I mean really digging into what’s driving this decision.

Maybe your family has grown and you’re constantly tripping over toys in your too-small living room. Perhaps you’re tired of paying rent and watching that money disappear each month instead of building equity. Or maybe you’ve been maintaining a big house since the kids moved out, and you’re ready for something more manageable that doesn’t require spending every weekend on yard work.

Your “why” is incredibly important because it becomes your North Star throughout the entire process. When you’re feeling overwhelmed by paperwork, when you see a house that’s almost perfect but not quite, when you’re negotiating and feeling the pressure—that’s when your why keeps you grounded and focused.

Think of it as your personal mission statement for this journey. Write it down. Put it somewhere you’ll see it regularly. Share it with your real estate agent so they truly understand what success looks like for you. Because here’s what I’ve learned: when you’re clear about your motivation, making decisions becomes so much easier. You’re not just looking at square footage and granite countertops anymore. You’re evaluating whether a property helps you achieve what you actually want out of life.

What You Actually Need

Once you know your why, it’s time to get practical. This is where a lot of people jump straight to Pinterest boards and dream home fantasies, which is fun but not super helpful when you’re actually house hunting.

Start by making two lists. The first list is your absolute must-haves—the non-negotiables that a home has to have or you won’t even consider it. The second list is your nice-to-haves—things you’d love but could live without if necessary.

Your must-haves might include things like the number of bedrooms you need. If you’ve got three kids, a two-bedroom house probably isn’t going to cut it, no matter how charming the kitchen is. Maybe you work from home and need a dedicated office space where you can close the door and take video calls without the dog barking in the background. Or perhaps you’ve got a beloved pet who needs a fenced yard to run around safely.

Nice-to-haves are different for everyone. Some people dream of a chef’s kitchen with a gas range and an island big enough to seat six. Others want a master bathroom with a soaking tub and separate shower. A three-car garage, a screened porch, hardwood floors throughout—these are all great features, but they’re bonuses rather than requirements.

Here’s why this distinction matters: in today’s market, affordability is still a real concern for many buyers. Having your priorities straight means you can be flexible where it counts. Maybe you’re willing to consider a neighborhood that’s a bit farther from downtown if the home checks all your essential boxes. Perhaps you’ll take a house that needs some cosmetic updates if the bones are solid and the layout works for your family.

Go over these lists with your real estate agent during your first meeting. A good agent will use this information to filter through properties and show you homes that actually match what you need, saving you time and preventing you from falling in love with places that don’t make sense for your situation.

Wrap Your Head Around the Numbers

Let’s talk about everyone’s favorite topic: money. I know, I know—it’s not as fun as imagining yourself hosting dinner parties in your new dining room. But understanding your financial picture is absolutely crucial if you want to make this happen.

Start by taking an honest look at your savings. How much do you have set aside for a down payment? The old rule was that you needed twenty percent down, but that’s not always the case anymore. There are programs available that require much less, sometimes as little as three to five percent. The trade-off is that you’ll likely pay private mortgage insurance if you put down less than twenty percent, but for many people, that’s worth it to get into a home sooner.

Next, think about what monthly payment feels comfortable for you. And I mean actually comfortable, not “we could technically afford this if we never eat out and cancel all our subscriptions” comfortable. You want to buy a home you can enjoy, not one that keeps you up at night worrying about money.

Don’t forget about the other costs that come with homeownership. Property taxes, homeowners insurance, potential HOA fees, utilities, and maintenance all need to factor into your budget. A good rule of thumb is to expect to spend about one to two percent of your home’s value annually on maintenance and repairs. That might sound like a lot, but it’s reality, especially with older homes.

This is where working with professionals becomes absolutely essential. A local real estate agent can give you realistic expectations about what your money will buy in your target neighborhoods. They’ve seen countless transactions and can tell you whether your budget aligns with your wishlist or if some adjustments are needed.

A lender is equally important, maybe even more so. They’ll look at your income, debts, credit score, and savings to determine what you can actually borrow. Getting pre-approved for a mortgage isn’t just about knowing your budget—it also shows sellers you’re a serious buyer, which can make your offer more competitive.

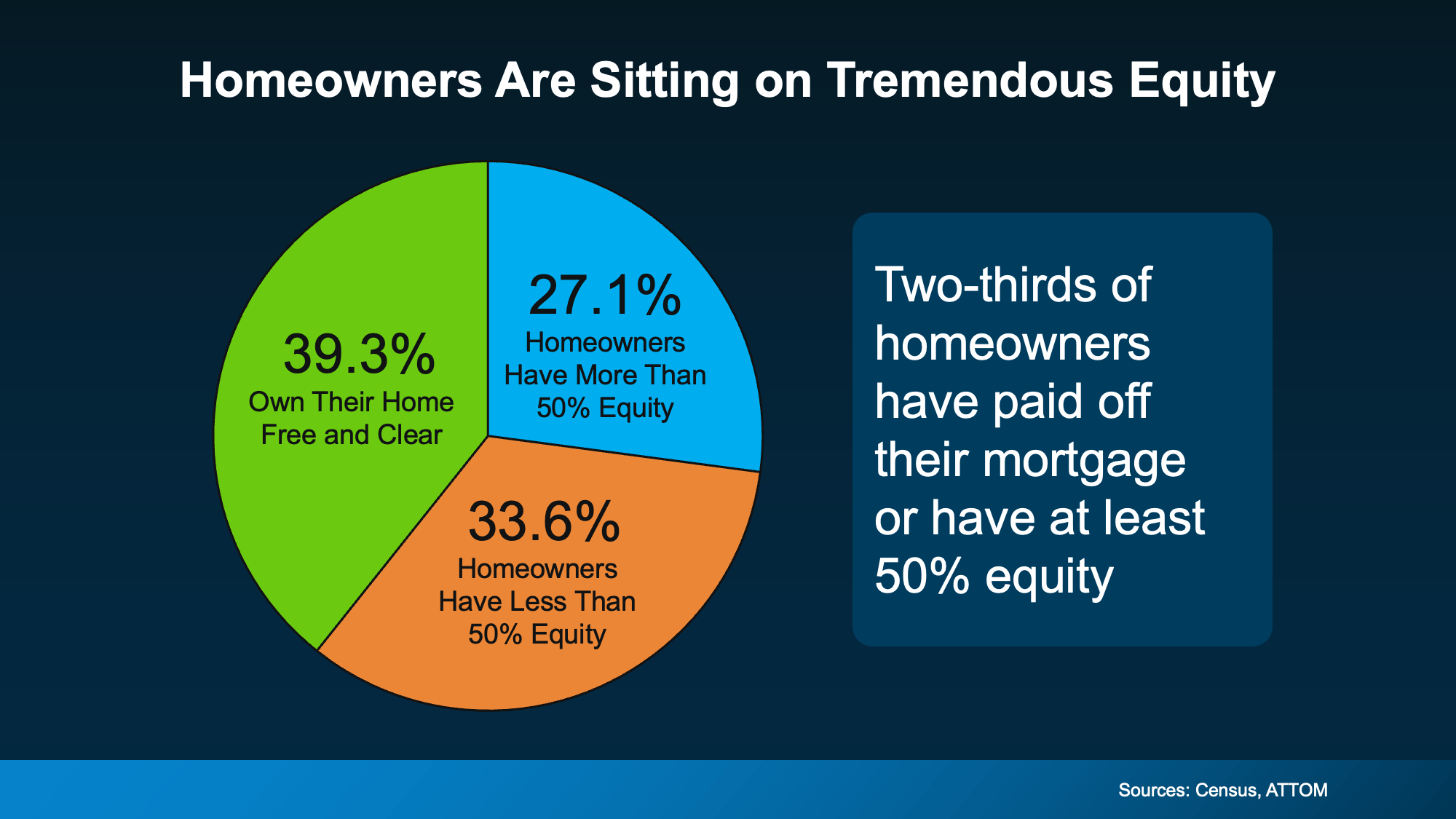

If you’re currently a homeowner looking to sell and buy, you’ll need to understand the equity you’ve built up in your current property. This equity can become your down payment on your next home, which is one of the significant advantages of homeownership. Your agent can help you understand current market values and timing strategies so you’re not stuck owning two homes at once or, worse, being homeless between properties.

Your Home Wishlist

Okay, now we get to the fun part—figuring out exactly what your dream home looks like. But let’s approach this strategically rather than just pinning pretty pictures on a board.

Think about size first. How much space do you genuinely need versus how much you think you want? A bigger house means higher utility bills, more to clean, more to furnish, and more to maintain. Sometimes people realize they’d be happier with a smaller, well-designed space than a sprawling home with rooms they never use.

Layout matters more than you might think. An open floor plan might be perfect if you love entertaining and want to chat with guests while cooking. But if you prefer defined spaces and closed doors, or if you work from home and need quiet, a more traditional layout might suit you better. Think about your daily routines and how you actually use your space.

Location is always going to be a major factor. How long of a commute are you willing to tolerate? Do you want to be walking distance to shops and restaurants, or do you prefer a quieter, more suburban setting? What about school districts if you have kids? Proximity to family and friends? These questions all matter.

Features and finishes are where personal preference really shines through. Some buyers won’t even look at a house without granite or quartz countertops. Others couldn’t care less and plan to renovate anyway. High-end appliances, a fancy backsplash, spa-like bathrooms—these things add to a home’s appeal and price tag, but only you can decide what’s worth paying extra for.

Don’t forget about outdoor space. A big backyard might be essential if you have kids or dogs. Or maybe you’re a gardening enthusiast who dreams of raised beds and a greenhouse. On the flip side, if you hate yard work, a low-maintenance property with minimal landscaping might be ideal.

Special rooms and features have become increasingly popular. A home office isn’t just a nice-to-have anymore for many people—it’s essential. A mudroom can be a game-changer for families with kids and pets. A butler’s pantry makes entertaining easier. A finished basement adds valuable living space. Think about which of these features would genuinely improve your daily life.

Here’s a pro tip: tour some homes before you get too attached to your wishlist. Sometimes you’ll discover that something you thought was essential actually doesn’t matter that much, or you’ll fall in love with a feature you hadn’t even considered. Real-world experience beats theoretical planning every time.

Don’t Get Overwhelmed

The internet has made house hunting simultaneously easier and more complicated. You’ve got access to incredible resources, but you can also go down rabbit holes that leave you feeling more confused than when you started.

Start with the basics. Online real estate platforms let you search for homes in your target areas, filter by your criteria, and get a sense of what’s available in your price range. You can take virtual tours, look at neighborhood photos, and sometimes even see historical price data. These tools are fantastic for getting oriented and developing a sense of what different areas offer.

But don’t stop there. Research the neighborhoods themselves, not just the houses in them. What are the schools like? What’s the crime rate? Are there parks, walking trails, and community amenities? What’s the vibe of the area—is it more families with young kids, young professionals, retirees, or a mix?

Here’s something many buyers don’t think to do: actually spend time in the neighborhoods you’re considering. Drive through at different times of day and on different days of the week. Stop by on a Saturday morning and see what the energy feels like. Grab coffee at a local shop. You might discover that a neighborhood that looked perfect online doesn’t actually feel right, or you might fall in love with an area you hadn’t seriously considered.

Mortgage options deserve their own research time. There are conventional loans, FHA loans, VA loans if you’re a veteran, USDA loans for rural areas, and various state and local programs designed to help buyers, especially first-timers. Each has different requirements, down payment expectations, and benefits. Your lender can walk you through the options, but doing some preliminary research helps you ask better questions.

Don’t be afraid to adjust your expectations based on what you learn. Maybe you discover that the neighborhood you had your heart set on is completely out of your price range, but there’s a neighboring area that’s more affordable and actually has better schools. Flexibility is your friend in this process.

Save More Than You Think You’ll Need

One of the biggest mistakes buyers make is underestimating how much money they’ll need, both upfront and after moving in. Let’s talk about the real costs involved.

Your down payment is the obvious one, but it’s not the only upfront cost. You’ll also need money for closing costs, which typically run between two and five percent of the purchase price. That includes things like appraisal fees, title insurance, attorney fees, and various other charges that add up quickly.

Then there’s moving itself. Whether you’re hiring professional movers or renting a truck and bribing friends with pizza, moving costs money. If you’re moving to a new area, you might need temporary housing while you search, which is another expense to plan for.

Once you’re in your new home, some immediate costs pop up. Utility deposits are usually required when you set up new accounts. You might need window treatments if the previous owners took theirs. Many homes require at least some minor repairs or updates right away—maybe the fence needs fixing, or you discover the dishwasher doesn’t work properly.

Maintenance and repairs are ongoing realities of homeownership. Even a brand new home will eventually need things fixed or replaced. Older homes might need attention sooner rather than later. Setting aside money each month for inevitable repairs isn’t pessimistic—it’s smart planning. When the water heater dies or the AC needs servicing, you’ll be glad you have that cushion.

Landscaping is another expense people often forget about. Maybe the yard needs basic maintenance equipment like a lawn mower and trimmer. Perhaps you want to add some curb appeal with plants and mulch. Or maybe you’re dealing with more significant needs like tree removal or drainage issues.

The bottom line is this: save more than you think you’ll need. If you calculate that you need fifteen thousand dollars for your down payment and closing costs, try to save twenty thousand. That buffer will save you stress and give you options if unexpected expenses arise.

Work With Real Estate Pros Who Have Your Back

You could theoretically buy a home without professional help, but I wouldn’t recommend it. Real estate transactions are complex, legally binding, and involve more money than most of us deal with in our daily lives. Having experts guide you isn’t a luxury—it’s smart strategy.

Your real estate agent is your advocate, adviser, and navigator throughout this journey. A good agent brings local market knowledge that you simply can’t get from browsing online. They know which neighborhoods are up-and-coming, which have hidden issues, and which offer the best value. They understand market dynamics—when it’s a buyer’s market versus a seller’s market, and how to position you accordingly.

But it’s more than just knowledge. A great agent also brings negotiation skills to the table. They’ve handled countless transactions and know how to structure offers, negotiate repairs, navigate inspection issues, and push for terms that benefit you. They can read situations and people in ways that help you make strategic decisions.

Just as importantly, an agent manages the overwhelming amount of detail involved in buying or selling. There are deadlines to track, documents to sign, contingencies to monitor, and communications to coordinate between all the different parties. Your agent keeps everything moving forward so nothing falls through the cracks.

Your lender is equally crucial. They don’t just approve you for a loan—they help you understand your options and choose the mortgage product that best fits your situation. They can explain the difference between a fifteen-year and thirty-year mortgage, help you understand adjustable versus fixed rates, and calculate different scenarios so you can make informed decisions.

Good lenders are also educators. If your credit score needs work before you can qualify for the best rates, they’ll tell you what steps to take. If your debt-to-income ratio is too high, they’ll help you understand what you need to change. They want you to succeed because your success is their success.

When choosing professionals, don’t just go with the first person you meet. Interview a few agents and lenders. Ask about their experience, their communication style, and their approach to working with clients. You want people who listen to you, respect your goals, and make you feel confident rather than pressured.

Check references and reviews, but remember that every client is different. What matters is whether their approach aligns with your needs and communication preferences. Some people want an agent who’s constantly checking in, while others prefer less frequent updates. Some buyers want to see every possible option, while others want their agent to pre-filter and only show the best matches. Find professionals whose style works for you.

Realistic Timelines

Real estate doesn’t happen overnight, and trying to rush the process usually leads to mistakes and regret. Let’s talk about realistic timelines and pacing.

If you’re starting from scratch—meaning you haven’t talked to a lender yet and you’re still saving for a down payment—you might be looking at several months before you’re ready to seriously house hunt. That’s not a bad thing. Use that time to improve your financial position, research neighborhoods, and get clear on what you want.

Getting pre-approved typically takes a few weeks once you submit your application and documents. Don’t confuse pre-approval with pre-qualification. Pre-qualification is a quick estimate based on the information you provide. Pre-approval involves actually verifying your finances and gives you a much stronger position as a buyer.

The house hunting phase varies wildly depending on your market and how specific your criteria are. Some buyers find their perfect home in the first weekend. Others search for months. On average, most buyers look at about ten homes before making an offer, but there’s no right or wrong here. You’ll know it when you find it.

Once you’re under contract, expect about thirty to forty-five days until closing, though this can be shorter or longer depending on various factors. This period includes the home inspection, appraisal, finalizing your mortgage, and handling any negotiated repairs. There’s a lot happening behind the scenes, even when it feels like nothing is moving forward.

If you’re selling your current home and buying another, timing gets trickier. Ideally, you’d close on your sale and your purchase on the same day or very close together. Your agent can help strategize this, potentially including contingencies in your contracts to protect you.

Here’s some honest advice: don’t put artificial pressure on yourself with arbitrary deadlines. Yes, there might be timing considerations like school schedules or lease expirations, but within reason, it’s better to take the time to find the right home than to settle for something that doesn’t really work just to meet a deadline.

The market itself also affects timing. If inventory is low and competition is fierce, finding the right home takes longer. If there are lots of options and fewer buyers, you might move more quickly. Your agent can help you understand current conditions and adjust your expectations accordingly.

Making the Actual Move

All the planning in the world doesn’t mean much if you don’t take action. So let’s talk about the practical steps to turn your goal into reality.

Start by getting your finances in order. Request your credit reports and check them for errors—you’d be surprised how often there are mistakes that can be easily corrected. Pay down high-interest debt if possible, as this improves your debt-to-income ratio. Build up your savings consistently, even if it’s just a little bit each month.

Connect with a real estate agent and lender early, even if you’re not quite ready to buy. They can give you a roadmap of what you need to do and help you set realistic timelines based on your situation. Think of these initial conversations as consultations where you’re gathering information and building relationships.

If you’re selling your current home, you’ll need to prepare it for market. This might involve decluttering, making minor repairs, fresh paint, and professional staging. Your agent will walk through your home and give specific recommendations for what will provide the best return on investment.

For buyers, attending open houses is valuable even before you’re ready to make an offer. You’ll start developing a sense of what you like and don’t like, what your money buys in different areas, and what compromises you’re willing to make. You’ll also get better at quickly assessing whether a property is worth a closer look.

When you find a home you want to make an offer on, your agent will help you determine a fair price based on comparable sales and current market conditions. In competitive situations, you might need to think creatively about making your offer attractive—maybe a flexible closing date, a personal letter to the sellers, or limiting contingencies if you’re comfortable doing so.

The inspection period is your chance to learn everything about the condition of the home. Hire a qualified home inspector and attend the inspection if possible. They’ll find issues you never would have noticed. How you handle inspection findings depends on their severity—major problems might lead to requesting repairs or a price reduction, while minor issues you might just accept.

Closing day is exciting but involves signing a mountain of paperwork. Read everything carefully and don’t be afraid to ask questions if something doesn’t make sense. Bring a valid ID and whatever payment method your closing attorney requires for your portion of the costs.

Embracing Your Fresh Start

The day you get the keys to your new home is incredibly special. All the stress of searching, negotiating, and coordinating suddenly feels worth it when you walk through that door knowing it’s yours.

But here’s something people don’t always think about: moving into a new home is both exciting and overwhelming. There’s unpacking to do, systems to learn, new routines to establish. Give yourself grace during this transition period. You don’t need to have everything perfect immediately.

Take time to actually settle in before jumping into major projects. Live in the space for a while and figure out how you use each room. That grand renovation plan might change when you realize your initial ideas don’t match how you actually function in the space.

Get to know your neighbors and your neighborhood. Introduce yourself to the people next door. Find your new favorite coffee shop and grocery store. Locate the nearest park, the best pizza place, and where to get your car serviced. These small acts of integration help a new place start feeling like home.

If you’re selling and buying, there’s often an emotional component to leaving your old home, especially if you’ve made wonderful memories there. That’s completely normal and okay. You can honor what that place meant to you while being excited about this new chapter.

Why This Year Makes Sense

So why tackle this now? Why make 2026 the year you finally make your real estate dreams happen?

First, there’s something powerful about using the new year as a starting point. It provides natural momentum and a clear beginning to your journey. Instead of vaguely thinking “someday we should move,” you’re committing to making it happen this year.

Second, waiting rarely makes things easier. Markets fluctuate, and while nobody can predict the future, waiting for the “perfect” time often means missing out on opportunities. If homeownership or a new home would genuinely improve your quality of life, the best time to start is now.

The longer you wait, the longer you delay the benefits of being in the right home. If you’re currently renting and that money could be building equity instead, each month that passes is a missed opportunity. If you’re in a home that doesn’t work for your needs, every day you stay there is another day of frustration.

Starting early in the year also gives you the entire year to work with. If you encounter obstacles or it takes longer than expected, you’ve got time to navigate challenges without feeling rushed. There’s breathing room in your timeline.

Finally, taking action feels good. Even if the actual transaction doesn’t happen until later in the year, knowing you’re moving toward a meaningful goal creates positive momentum in your life. You’re not just thinking about change—you’re creating it.

Your Next Steps Start Today

Here’s what I want you to take away from all this: buying or selling a home doesn’t have to be overwhelming. Yes, it’s a big decision. Yes, it involves money and paperwork and more decisions than you probably realize right now. But it’s also completely doable, especially with the right preparation and the right team supporting you.

Start by getting clear on your why. Write it down. Share it with your partner or whoever else is part of this decision. Let that motivation guide everything that follows.

Make your lists of must-haves and nice-to-haves. Be honest with yourself about what you actually need versus what would just be cool to have.

Look at your finances realistically and start talking to professionals who can help you understand what’s possible. Get pre-approved so you know exactly where you stand.

Do your research, but don’t get paralyzed by information overload. At some point, you need to move from learning to doing.

Find a real estate agent who gets you, who listens to your goals, and who you trust to guide you through this process. That relationship makes all the difference.

And then take it one step at a time. You don’t need to have everything figured out from day one. This is a journey, and like any journey, you figure things out as you go.

The vision of yourself in a new home in 2026 doesn’t have to stay a vision. With intention, preparation, and the right support, you can absolutely make it your reality. And here’s the best part: a year from now, you could be celebrating your first holiday season in your new place, making new memories in a home that truly works for your life.

So if this is something you’ve been thinking about, if moving has been in the back of your mind, or if you’re ready to take the leap, don’t wait. Start having those conversations. Reach out to professionals who can help. Take that first step.

Your 2026 could look very different from your 2025, and it starts with deciding that this is the year you’re going to make it happen. The fresh start you’re imagining is absolutely within reach. Let’s make this the year you turn that dream address into your real address.