(Updated 6/19/26)

When someone asks me whether they should buy a home during a recession, they’re almost never reacting to a chart they saw in The Wall Street Journal. They’re reacting to a feeling. The headlines have been grim for weeks, a coworker just got laid off, and the idea of signing for a $300,000 house right now feels a little like jumping off a diving board you can’t see the bottom of.That fear is reasonable. But it’s worth separating from the actual numbers, because the two don’t always point the same direction.

The part that surprises people: in Memphis, recessions have historically been pretty good for buyers. Fewer competing offers. More homes sitting on the market. Sellers who suddenly remember how to negotiate. That’s not a sales pitch, it’s just what tends to happen when the economy cools and the frenzy drains out of the market.

The honest caveat, which we’ll keep coming back to, is that your personal situation matters more than any GDP report. Your savings. Your job. Whether you actually need to move or just feel like you should be doing something. Get those right and a downturn can work in your favor. Get them wrong and no amount of market timing will save you.

Let’s walk through it.

Why slowdowns tend to help Memphis buyers

In a hot market, you’re one of nine offers on a house, waiving the inspection and writing a love letter to a seller who’ll never read it. In a slow market, a lot of that pressure evaporates.

When buyer demand softens, the balance of power shifts. Homes take longer to sell. Sellers who were holding out for top dollar start getting realistic. And the things that were impossible to ask for during the boom suddenly land on the table.

We’ve seen sellers in slower stretches agree to cover closing costs, knock thousands off the price for repairs an inspection turned up, or throw in a home warranty to sweeten the deal. New-construction builders get especially creative. When they’ve got finished inventory sitting empty, they’d rather buy down your mortgage rate or cover points than let a house collect dust, because an unsold home costs them every single month.

Memphis inventory has loosened up compared to the white-knuckle years of the pandemic. More choices means more leverage at the negotiating table, which is exactly the environment where a patient, prepared buyer does well. If you want a fuller picture of how the local process works start to finish, our overview of buying a home in Memphis breaks it down step by step.

A cooler market trades the stress of competition for the upside of negotiation, and that trade usually lands in the buyer’s favor.

What’s fueling the recession talk in 2026

It helps to know why everyone’s nervous, because the reasons are real but they’re not the whole story.

A few things are stacking up. Tariff uncertainty has businesses cautious about spending. Job creation has slowed from the breakneck pace we saw coming out of the pandemic. And the long post-pandemic boom, the one that made everything from groceries to grills feel chaotic, is finally winding down. That cooling-off can feel like the floor dropping when really it’s the economy catching its breath.

Now the other side of the ledger. Unemployment is still low by historical standards. Mortgage rates have settled into the low-to-mid 6% range, which felt high three years ago and feels almost normal now. And affordability has quietly been improving in a lot of markets, with wages in many areas growing a bit faster than home prices for the first time in a while. We dug into that trend in our look at why affordability is expected to improve in 2026.

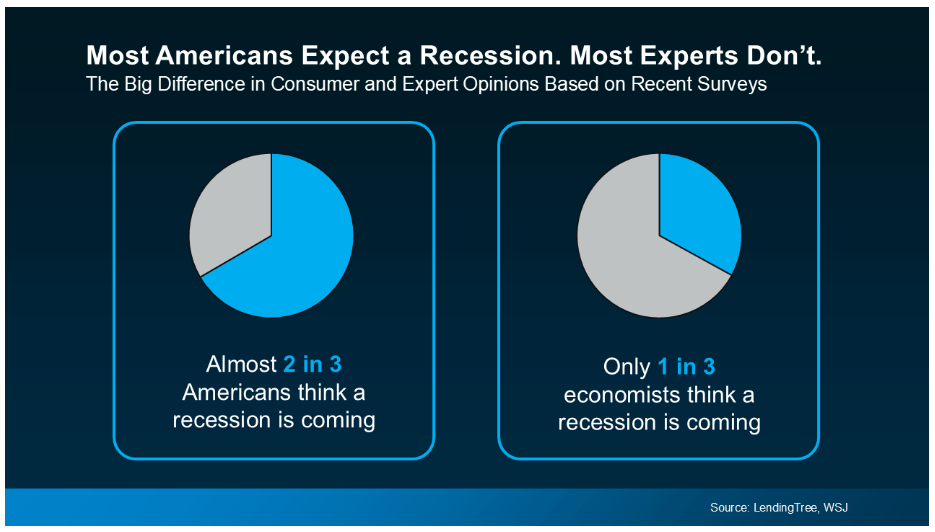

There’s also a telling gap in who’s actually worried. Surveys keep showing that roughly two-thirds of Americans expect a recession, while only about one in three economists do. That split says a lot. A big chunk of the recession fear is sentiment, not forecast. People feel a recession in their gut long before the data confirms one, and sometimes the data never does.

This is not 2008, and the difference is the whole ballgame

Almost everyone who hesitates to buy in a downturn is haunted by the same memory: 2008. Watching neighbors lose homes and prices crater is the kind of thing that sticks. So let’s address it directly, because 2008 was a very specific disaster that we are not set up to repeat.

The 2008 collapse was a lending crisis at its core. Banks were handing out no-documentation loans to people who couldn’t realistically pay them back, then bundling that risk and selling it off across the financial system. When the loans went bad, foreclosures flooded the market all at once. That tidal wave of distressed homes, not a normal recession, is what drove prices down 30% or more in some places.

Today’s setup looks almost nothing like that. Lending standards are strict. Lenders verify income, check debt, and document everything. Foreclosure activity has been running below normal historical levels, which means there’s no flood of distressed inventory waiting to drag prices down. If you want the data behind that, we covered it in our piece on why foreclosure activity is still lower than the norm.

On top of that, homeowners are sitting on near-record levels of equity. That matters more than it sounds. When people have real equity, a job loss or a rough stretch means they can sell and walk away with cash. In 2008, millions owed more than their homes were worth, so their only exit was foreclosure. That’s the engine that turned a recession into a housing collapse, and it isn’t running today.

Memphis has an extra layer of insulation. We never saw the wild price spikes that hit Austin, Phoenix, or Boise during the boom. Our market climbed steadily instead of going vertical. And markets that don’t balloon don’t have far to fall, which is part of why Memphis tends to ride out downturns more gently than the cities that made the breathless national headlines.

What mortgage rates do in a downturn

This is where a lot of buyers get tangled up, so it’s worth slowing down.

When a recession hits or threatens, the Federal Reserve typically responds by cutting its benchmark rate to keep money moving through the economy. Mortgage rates don’t track the Fed perfectly, but over time they tend to drift downward in that environment. In 2020 they fell below 3%, a number that still sounds made up. During the 2008-09 stretch they eased from around 6.5% down under 5%.

The catch is timing. Those drops don’t happen the day a recession is announced. There’s a lag, sometimes months, sometimes longer, and nobody rings a bell at the bottom.

So what does that mean for you if you buy now and rates fall later? You refinance. A refinance usually runs a few thousand dollars in costs, and when rates drop meaningfully, that math often pays for itself within a year or two. You lock in today’s price on the house, then reset your payment downward when the window opens.

A rough, illustrative example makes it concrete. Say you buy a $300,000 home with 10% down at around 6.5%. Your principal and interest would land somewhere near $1,700 a month. If rates eventually slide to, say, 5.5% and you refinance, that same loan drops to roughly $1,530, saving you close to $170 a month, or a couple thousand a year. The numbers are simplified and your actual figures will vary, but the shape of it holds: you bought at the lower price, then improved your rate later.

Now flip it. If you wait for rates to drop before you buy, you won’t be alone. Every other buyer who’s been sitting on the sidelines will jump in the same week, demand will surge, and prices will climb right along with it. You might win the rate and lose the price war. We laid out both sides of this in buy now or wait for lower mortgage rates, and the short version is that the “perfect” moment usually isn’t.

There’s a related shift worth knowing about too. A lot of homeowners who locked in ultra-low rates years ago have been frozen in place, unwilling to sell and give up that rate. That logjam is starting to ease, which means more of those homes are finally hitting the market. We tracked it in the lock-in effect breaking in 2026. The old line still holds up: marry the house, date the rate. You can’t refinance a price you missed.

Income risk beats price risk

Let’s be blunt about what can hurt you in a recession. It’s not a 4% dip in your home’s paper value over a year you weren’t planning to sell anyway. It’s losing the income that pays the mortgage. That’s the real exposure, and it’s why your job situation deserves more attention than any economic forecast.

The reassuring part is how rare widespread job loss is, even in bad recessions. Unemployment peaked around 10% in the worst of 2008-09, which sounds brutal, until you flip it: more than 90% of working people kept their jobs through the worst downturn in modern memory. Milder recessions are gentler still, often nudging unemployment from something like 4% up to 6%. Most people stay employed even when the news makes it feel like the sky is falling.

Memphis has a sturdier-than-average foundation here. Our economy leans heavily on industries that don’t vanish when the broader economy stumbles. Healthcare anchors a lot of it, with Methodist Le Bonheur, St. Jude, and the wider medical corridor employing tens of thousands. FedEx keeps its global headquarters here. Education and logistics round it out, and people keep needing doctors, schools, and packages no matter what the GDP is doing.

That’s a meaningfully different risk profile than a city built on tech, oil, or tourism, where a single bad quarter can ripple through the whole local job market at once. Memphis tends to wobble rather than crater. Protect against income loss first, because that, not a temporary dip in home values, is what turns a recession personal.

Renting won’t shield you from a recession

A lot of nervous would-be buyers default to renting, figuring it’s the safe play until things calm down. It feels safe. It often isn’t, at least not financially.

Rent doesn’t pause during a recession. Landlords don’t lower it out of solidarity with a soft economy. Their costs, property taxes, insurance, maintenance, don’t fall when GDP does, so rents tend to keep climbing right through downturns. Memphis rents have risen steadily for five years running, and nothing about a slowdown reverses that.

A fixed-rate mortgage, by contrast, locks your principal and interest for 15 or 30 years. Your payment in year ten is the same as your payment in year one, even as rents around you keep marching up. That stability is one of the most underrated benefits of owning, and it’s especially valuable when everything else feels unpredictable.

Run the numbers and the gap shows up fast. A renter who waits two years “for things to settle” might be paying $200 to $300 more a month by the time they finally buy, and they’ll have built exactly zero equity in the meantime. We put real figures to this in our breakdown of the renting vs buying net worth gap, and the spread over time is bigger than most people expect.

None of this means renting is wrong. If you might relocate soon, or your job genuinely feels shaky, the flexibility of renting is worth real money. That’s a smart, situational choice. But renting purely out of recession anxiety, with no other reason behind it, usually costs you more than it saves. Renting buys you flexibility and not much else, so make sure flexibility is what you actually need.

A quick word on buyer psychology

There’s a reason disciplined buyers tend to come out ahead in downturns, and it has less to do with spreadsheets than with nerves.

When the market is roaring, fear of missing out drives people to overpay, overreach, and waive protections they shouldn’t. When the market cools, the opposite fear takes over. People freeze. The same buyer who was ready to fight over a house in a frenzy now can’t pull the trigger even when conditions have tilted in their favor.

The buyers who do well aren’t braver than everyone else. They’ve just decided in advance what they can afford and what they need, so they can act on facts instead of reacting to headlines. Confidence in a downturn doesn’t come from predicting the market. It comes from knowing your own numbers cold.

How to buy smart when things feel shaky

If your situation is solid and you’re leaning toward buying, the goal is to do it in a way that builds in margin for error. A few moves matter most.

Build a bigger cash cushion

In normal times, three to six months of expenses in reserve is the standard advice. In an uncertain stretch, push toward six months or more if you can. That cushion is what lets you keep paying the mortgage if your income hiccups, and it’s the single best protection against the one risk that genuinely matters. Buy a little less house than the bank approves you for so the cushion has room to exist.

Get pre-approved early, with a local lender

Pre-approval tells you what you can really afford and signals to sellers that you’re serious. In a market with fewer buyers, a clean pre-approval can be the thing that gets your offer taken seriously over a wishy-washy competitor. A local Memphis lender often carries extra weight here, because listing agents know they’ll close on time and answer the phone, which matters when a seller is choosing between offers.

Negotiate beyond the sticker price

Price is just one lever. In a slower market you can often win more by asking for closing-cost credits, repair concessions after the inspection, a home warranty, or a builder rate buydown on new construction. Speaking of inspections, don’t skip yours, and know what to watch for. Our guide to home inspection red flags covers the issues worth walking away over. And if you do find yourself up against another offer, winning multiple offers without overpaying lays out how to stay competitive without blowing your budget.

Pick locations that hold their value

Where you buy shapes how well your home holds up if the market softens. In the Memphis area, the established suburbs have a strong track record. Homes in Collierville and homes in Germantown tend to stay desirable through downturns, anchored by top-rated schools and steady demand. Homes in Bartlett offer a similar stability at a different price point, and growing communities like Arlington and Lakeland have been drawing steady interest. Strong school districts are about as close to recession-resistant as residential real estate gets, because families will always pay to live where the schools are good, no matter what the economy is doing.

Don’t try to nail the exact bottom

Nobody catches the bottom on purpose, including the professionals who do this all day. The good news is you don’t have to. If you’re planning to stay in a home five years or more, the specific month you buy barely registers in the long run. A great house in a great neighborhood that you hold for years will almost always beat a slightly cheaper version you waited two anxious years to find. Time in the market beats timing the market.

A gut-check before you sign

Before you commit either way, sit with a few honest questions. Not the market’s questions, yours.

Do you have an emergency fund that could carry the mortgage for several months if your income paused? Is your job reasonably stable, or are there real signs of trouble where you work? Do you plan to stay in this home for at least five years? Could you cover the payment comfortably if rates didn’t drop and you never got to refinance? And are you buying because the timing fits your life, or because anxiety is telling you to either rush in or run away?

If you’re a first-time buyer, give yourself extra grace on these. The leap feels enormous because it is, and the loan programs, down-payment options, and assistance available to first-timers can change the math more than you’d guess. Our guide for your first home in Memphis walks through what that path looks like. And if the numbers feel tight on your own, more buyers are teaming up than ever, purchasing with a partner, a sibling, or a close friend to combine incomes and split the cost. It isn’t for everyone, but it’s a legitimate way into ownership that’s worth a real conversation.

When waiting really is the smarter move

I’d rather you wait than stretch into a purchase that puts you at risk, so let’s be just as clear about when sitting tight is the right call.

Wait if you don’t have an emergency fund yet. That cushion isn’t optional in a shaky stretch, and buying without it is the gamble, not the other way around.

Wait if your credit needs work. A better score can mean a meaningfully better rate, and a few months of cleanup can save you far more over the life of the loan than buying right this second ever would.

Wait if you’re not sure you’ll stay put. If a job change, a move, or a major life shift might be coming inside a couple of years, the costs of buying and selling can eat any gains.

And wait if your employment genuinely feels unstable. If your company is laying people off and your department feels like it could be next, that’s a real signal. Shore up your situation first. The house will still be there. Waiting isn’t losing. Buying from a position of weakness is.

Talk it through with someone who’ll be straight with you

The right answer to “should I buy during a recession” isn’t a blanket yes or no. It depends on your savings, your job, your timeline, and what you actually need, which is exactly why a generic headline can’t answer it for you.

What helps is a real conversation about your specific numbers. Not a pitch, not pressure, just an honest read on whether buying makes sense for you right now or whether you’re better off waiting a season. Sometimes we’ll tell you to hold off, and that’s the point.

If you’re weighing this in the Memphis or Germantown area, reach out. We’ll look at your situation clearly and tell you the truth, even when the truth is “not yet.”