(Updated 6/02/26)

Six months ago, the story was about relief finally arriving. Rates had eased off their 2024 highs, more listings were showing up, and the affordability math that punished buyers for three straight years was bending in the right direction. Now that we’re into the back half of the year, the question is different. It’s not whether affordability is improving anymore. It’s how long this window stays open.

Housing affordability in the second half of 2026 is holding up, but it’s no longer a clean upward trend. The first half of the year handed buyers some real gains. What happens between now and December depends on where mortgage rates settle, how much inventory keeps coming, and whether wages keep doing the quiet work of closing the gap. In the Memphis area, the picture looks better than the national headlines suggest, which is worth understanding before you make a move.

Mortgage rates are the wild card now

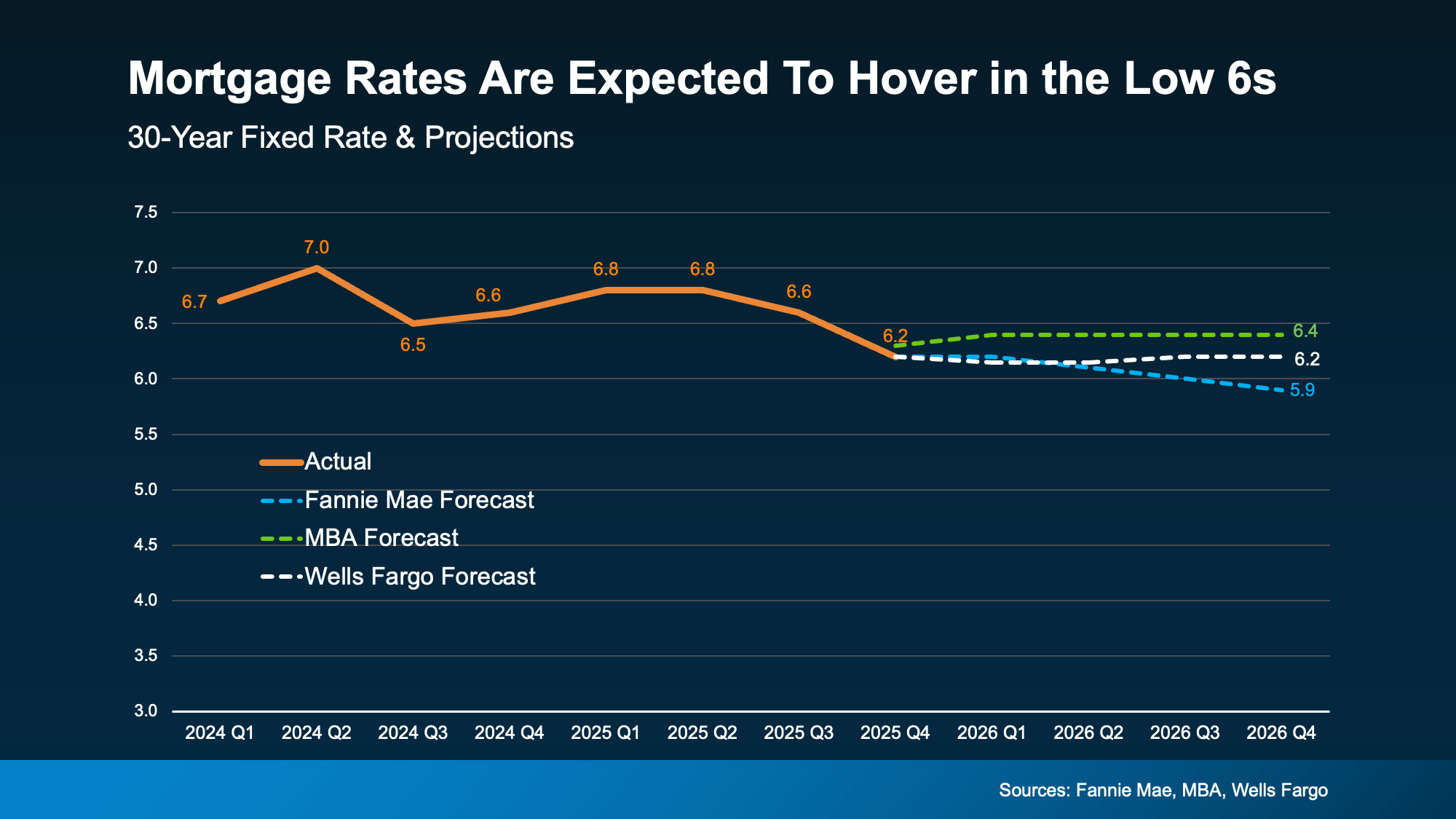

Through the first half of 2026, the average 30-year fixed drifted down into the low 6s, with some weeks dipping toward the high 5s. That move is most of the reason affordability improved at all. As of early summer, rates are sitting around 6.3% to 6.5%.

The forecasts for the rest of the year don’t agree, and that disagreement is the story. Fannie Mae and the Mortgage Bankers Association both expect rates to hold fairly steady, bouncing in the 6.1% to 6.3% range through December. Morgan Stanley takes the other side, projecting that rates could drift back up in the second half and into 2027 after the dip earlier this year. Most year-end averages land somewhere between 5.9% and 6.3%.

What that means in practice is that the cheap-money window some buyers were waiting for may have already come and gone in the spring. If you’ve been sitting on the fence expecting rates to keep falling all year, the data doesn’t back that bet. Planning around a steady glide toward 5% is a gamble.

On a $350,000 loan, the difference between 6.9% and 6.2% runs roughly $165 a month. Not life-changing, but enough to feel on a monthly budget, and enough that locking a decent rate when you find the right house beats holding out for a number that may never show.

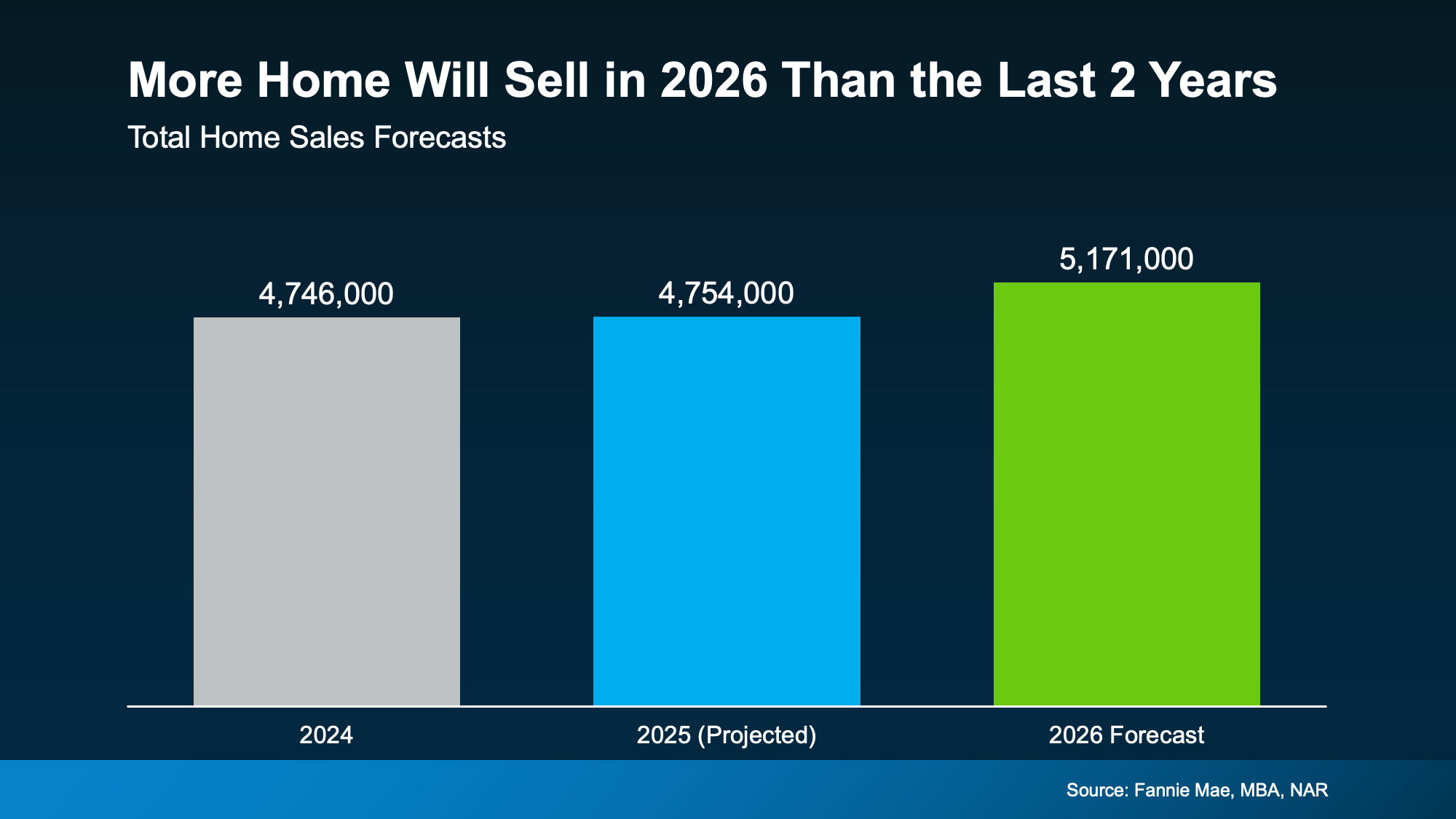

More homes, but still a tight market

Inventory is the brighter part of the story. Listings across the Memphis metro are up somewhere around 8% to 12% compared with a year ago, part of a national shift that’s been building since late 2025. After years of bare shelves, that’s a genuine change. Some of it traces back to the lock-in effect finally loosening as homeowners who’d been clinging to sub-4% mortgages decide life can’t wait any longer.

It’s still not a buyer’s market, and that’s the honest caveat. The metro is sitting around 3.9 months of supply, below the five to six months that signals true balance. Well-priced homes in good areas still move, and they’re closing at roughly 95% to 96% of asking. So buyers have more to choose from and a little more room to negotiate, but nobody’s getting steep discounts on the good stuff.

For the back half of the year, watch new construction and listing activity in the eastern suburbs. If the inventory bump holds through the fall, buyers keep their leverage. If it stalls, the advantage tilts back toward sellers heading into 2027.

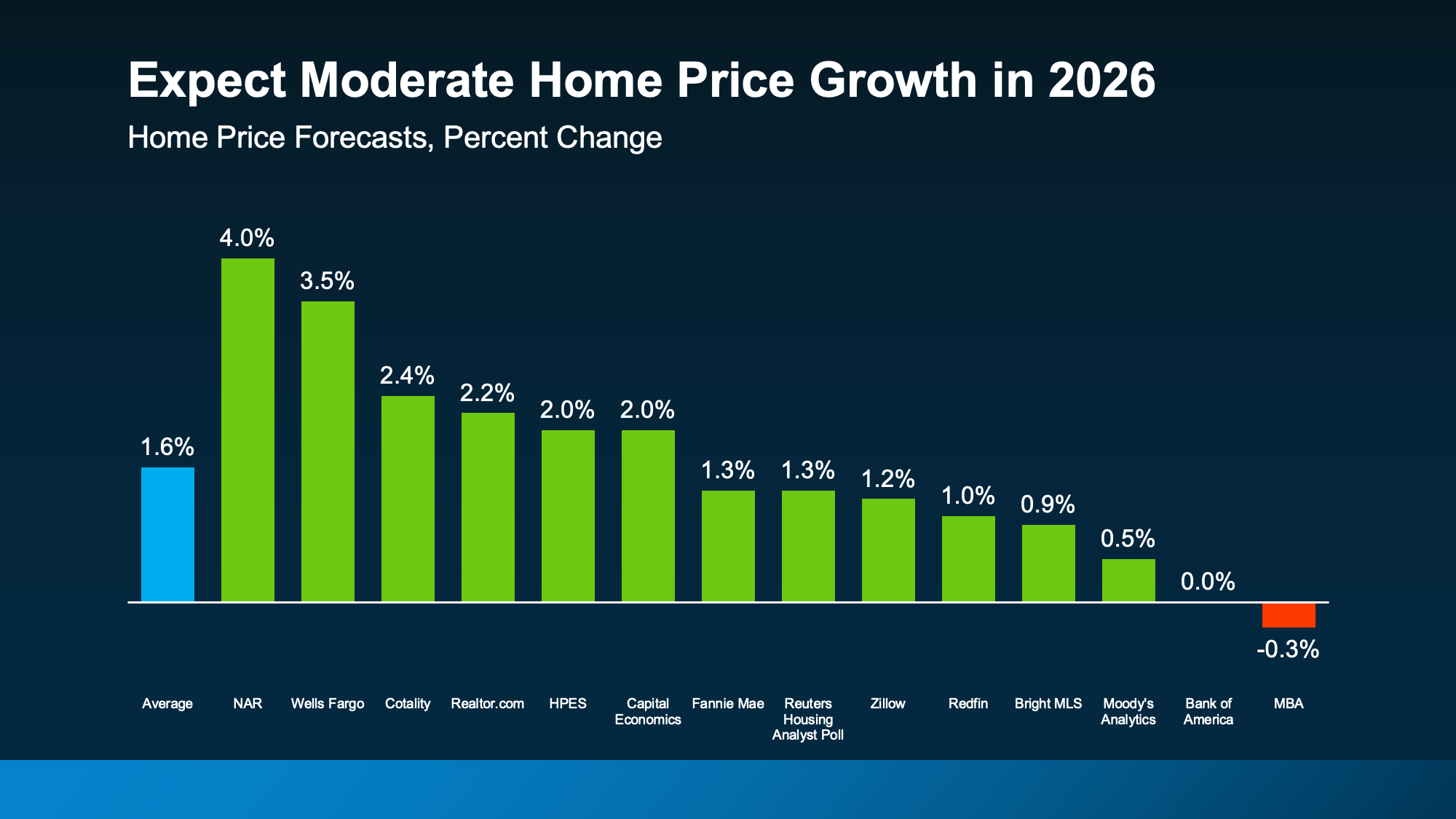

Prices are still climbing, just slowly

National home prices are up around 30% from where they sat in early 2020, and they haven’t given that back. What’s changed is the pace. Forecasts put Memphis-area appreciation somewhere in the 2% to 4% range for the year, a long way from the double-digit jumps of the pandemic.

Slow, steady price growth is the quiet good news for affordability. When prices crawl instead of sprint, the time you spend house-hunting stops working against you. You’re not watching your target move $10,000 out of reach every month you take to decide.

For sellers, modest appreciation means your equity is still growing, just at a calmer pace. If you bought before 2022, you’re almost certainly sitting on a solid gain regardless of the slowdown.

Why affordability held up at all

The piece that doesn’t make headlines is income. Wages have been growing a little faster than home prices through 2026, and that gap counts for a lot. When your paycheck rises 3% to 4% and home prices in your market rise 2% to 4%, your buying power inches forward even if rates barely move.

That’s the actual engine behind affordability improving this year. It isn’t a rate crash or a price drop. It’s the slow grind of incomes catching up after years of falling behind.

It helps to be realistic about the ceiling, though. Getting back to 2019-level affordability would take something dramatic on rates, income, or prices, and none of that is on the table for the second half of 2026. The improvement is real. It’s also incremental, and it’s strongest for buyers who are ready to act on it.

A national supply problem sits underneath all of this too. The country is short something like half a million homes priced under roughly $260,000, the exact range first-time and middle-income buyers shop in. That shortage is part of why entry-level homes still feel competitive even as overall inventory loosens.

What it means for Memphis, Germantown, and Collierville

National averages only get you so far. Real estate is local, and the Memphis metro keeps landing on the friendlier side of the affordability map.

Memphis remains one of the more affordable major metros in the country. A family buying here gets meaningfully more house for the money than the same household would in Nashville, Atlanta, or Charlotte, and Tennessee’s lack of a state income tax stretches a paycheck further on top of that. For first-time buyers especially, those are the conditions that turn renting into owning.

Germantown

Germantown’s schools and established neighborhoods keep demand steady, so homes here sell at a premium to the metro median. The upside for the back half of 2026 is choice. With more listings coming online, buyers searching for homes in Germantown have more room to be picky about neighborhood, lot, and price than they did a year ago.

Collierville

Collierville pulls buyers with its town square, top schools, and a mix of new construction and older neighborhoods. Newer developments tend to price a notch above Germantown, but the value holds up once you factor in school quality. The slower pace of price growth shows up here too, which gives people looking at homes in Collierville a bit more time to make a decision without feeling rushed.

Memphis and the surrounding suburbs

If value is your priority, Memphis proper and suburbs like Bartlett and Cordova still offer entry points below the metro median. The affordability edge is real enough that a lot of households can buy here while they’d still be stuck renting in a peer city. That’s the whole ballgame for first-time buyers, and it’s a big reason the local market keeps drawing people relocating from higher-cost areas.

If you’re buying in the back half of 2026

The case for buying now comes down to leverage that may not last. You’ve got more inventory than you’ve seen in years and a little negotiating room, while prices are still climbing slowly enough that waiting doesn’t pay.

The risk in waiting is the rate forecast. If the buyers betting on sub-5% rates are wrong, and the data suggests they might be, then holding out costs you months of rent and lost equity for a discount that never arrives. The smarter play hasn’t changed: buy when your finances and your life are ready, lock a rate you can live with, and refinance later if the chance comes. If 6.3% works in your budget today, the home search is worth starting now rather than gambling on December.

If you’re selling in the back half of 2026

Selling into this market is still a strong position, with one adjustment. You’re no longer the only listing on the block. Buyers have choices again, so your home has to earn its price instead of riding scarcity.

That puts all the weight on pricing and presentation. Homes priced to current comps and shown well are still closing near asking in a couple of weeks. Homes priced to last year’s peak sit, pile up days on market, and end up taking a cut anyway. The gap between those two outcomes is as wide as it’s been since before the pandemic. If you’re weighing a move, the prep work matters more now than it did in 2022, so clean, declutter, handle the deferred maintenance, and price to where the market is today before you list your home.

The equity side still favors you. Most owners who bought before 2022 are sitting on real gains even after the cooldown, and selling near today’s values beats gambling on another leg up the forecasts don’t promise. A quick home valuation is the right first step before you commit to anything.

What to watch between now and December

A few things could swing affordability before the year closes. The Federal Reserve’s rate decisions will steer where mortgage rates land by fall, and with the forecasts split the way they are, that’s genuinely uncertain. If the economy softens, rates could ease and give buyers another opening. If inflation reheats, rates hold or climb and the spring window closes for good.

Locally, keep an eye on inventory and hiring across the metro. Steady employer growth and a continued flow of new listings would keep the back half buyer-friendly. A pullback in either would tighten things up fast.

Bringing it together

Housing affordability in the second half of 2026 is better than it’s been in years, but it’s a window, not a trend you can count on widening. Rates have stopped falling and may even tick up. Inventory is healthier but still tight. Prices keep grinding higher, slowly. The one steady tailwind is income, and it’s doing more of the work than most people give it credit for.

The mistake right now is the same one it’s been all year: waiting for perfect conditions that aren’t coming. Sub-4% rates are gone. The combination of more choice, calmer prices, and rising wages means the math works better today than it did a year ago, especially in the Memphis area where the affordability edge runs deeper than the national numbers show. If you want to know what that looks like for your specific situation, reach out to our team and we’ll walk through the numbers that matter for your move.