(Updated 7/21/26)

There’s a version of this question we used to hear all the time: “Is it safe to buy a home during a recession?” Lately we’re hearing the opposite one. Buyers who could purchase today are sitting on the sidelines on purpose, waiting for a recession to arrive so they can buy at a discount. The logic sounds sensible. Recessions mean falling prices, falling prices mean deals, so the patient buyer wins.

If that’s your plan, this article is for you, because the plan rests on one assumption that deserves a hard look: that a recession would push Memphis home prices down far enough, for long enough, to reward the wait. History says that assumption is shakier than it feels. And while you’re waiting for a discount that may never come, the meter is running on some very real costs.

Let’s walk through what recessions have historically done to home prices, what one would mean for you as a buyer, and how to tell the difference between waiting for the market and waiting for the right moment in your own life.

The waiting strategy, spelled out

The plan usually goes something like this. A recession hits sometime in the next year or two. Home prices drop hard, maybe 20 or 30 percent like they did after 2008. Mortgage rates fall as the Federal Reserve cuts. You swoop in with your saved-up down payment, buy the same Germantown or Bartlett house for tens of thousands less, and lock a low rate while everyone else is too scared to act.

Every piece of that plan can be found in a real historical moment. The trouble is that they all come from one moment, 2008 to 2011, and that stretch was the exception, not the pattern. Building a housing strategy around a rerun of 2008 is like planning your commute around the one day the bridge was out.

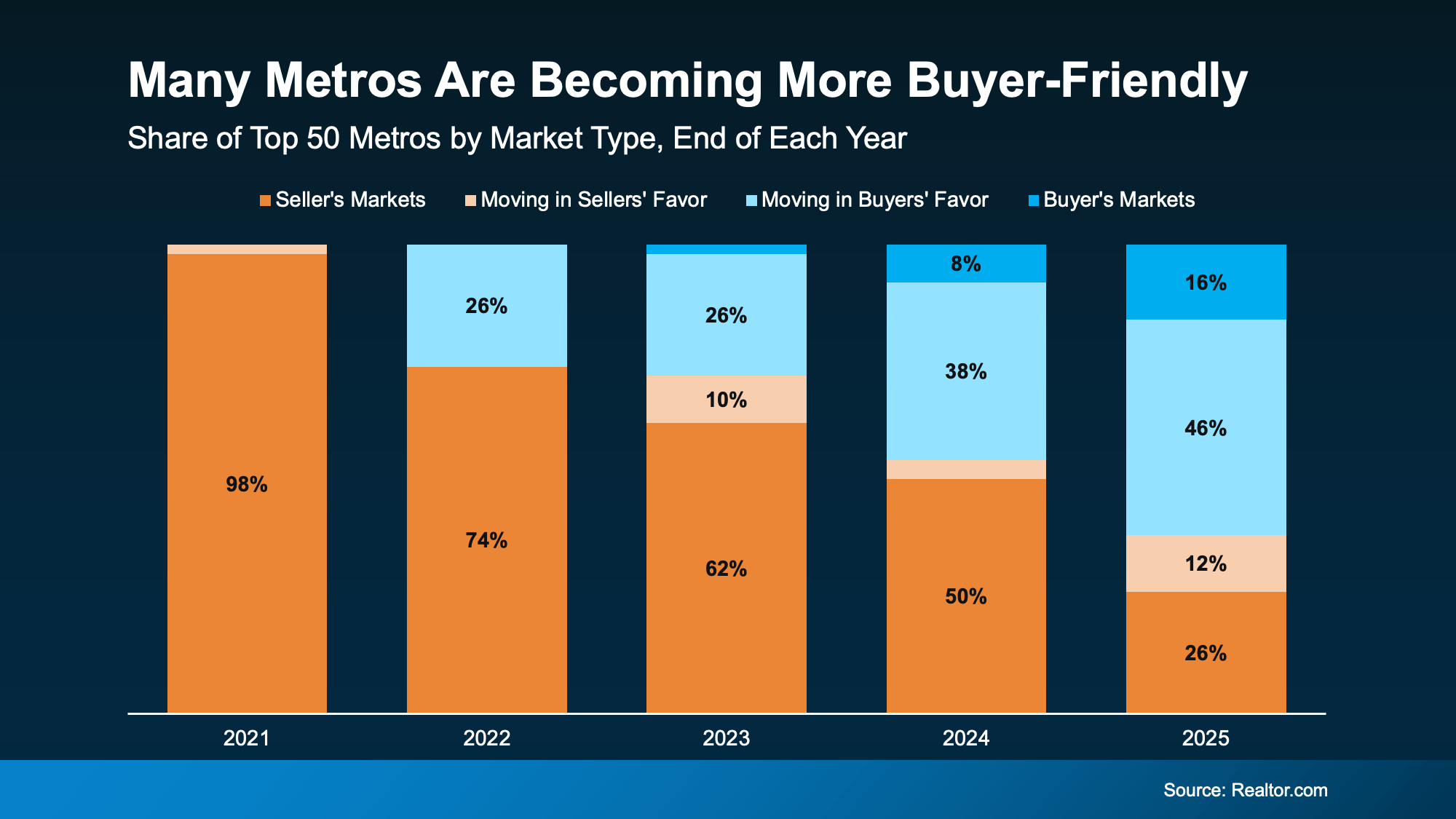

What recessions have historically done to prices

Go back through the recessions of the last several decades and a surprising pattern shows up: home prices usually held steady or kept rising. The early-1980s recessions, the early-90s downturn, the dot-com bust in 2001, the brief but severe 2020 pandemic recession, none of them produced a national collapse in home values. In 2020, prices accelerated straight through the recession. The 2008 crash stands nearly alone, and it was caused by something specific: a mortgage system that had spent years handing out loans to people who couldn’t repay them.

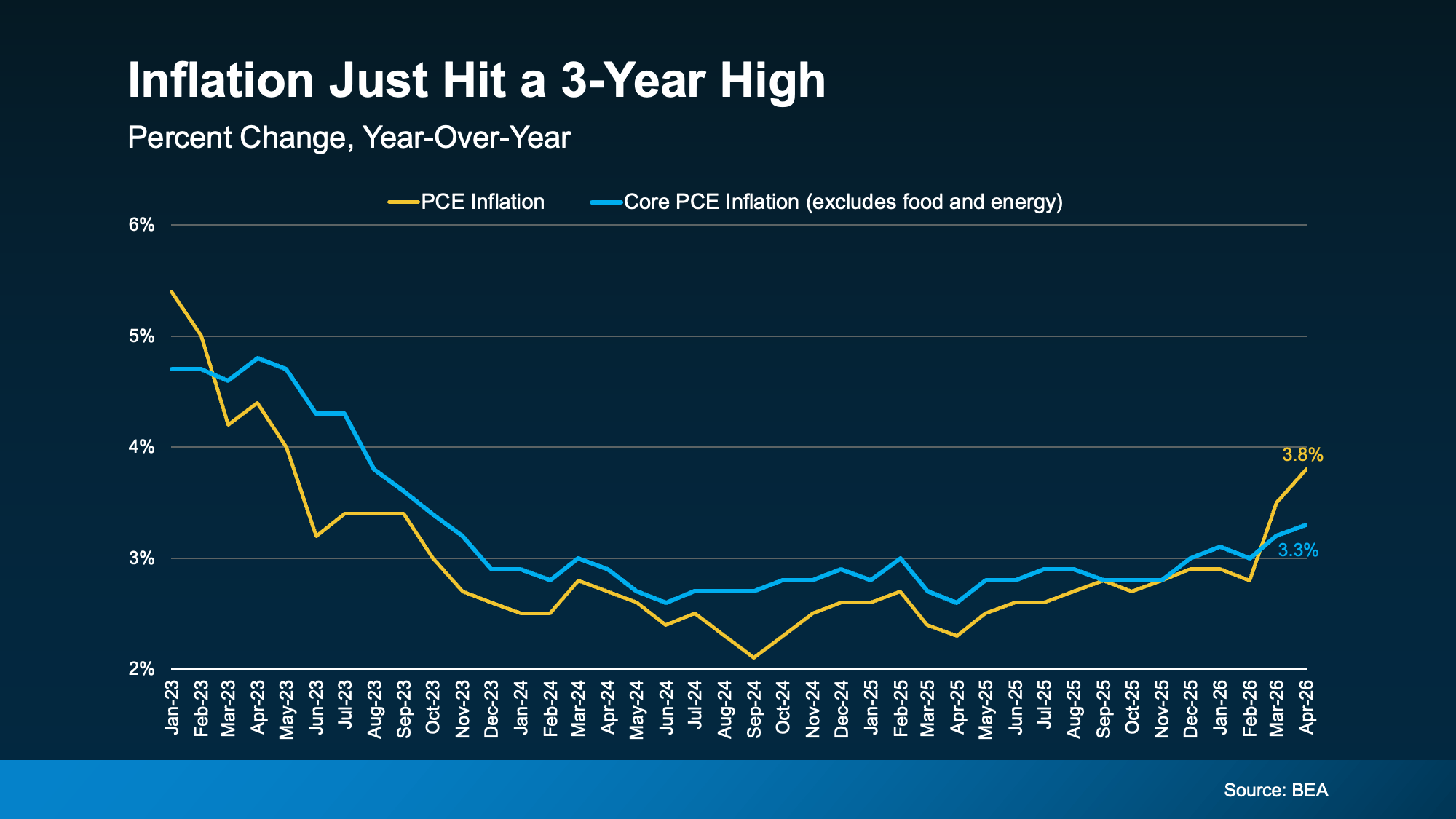

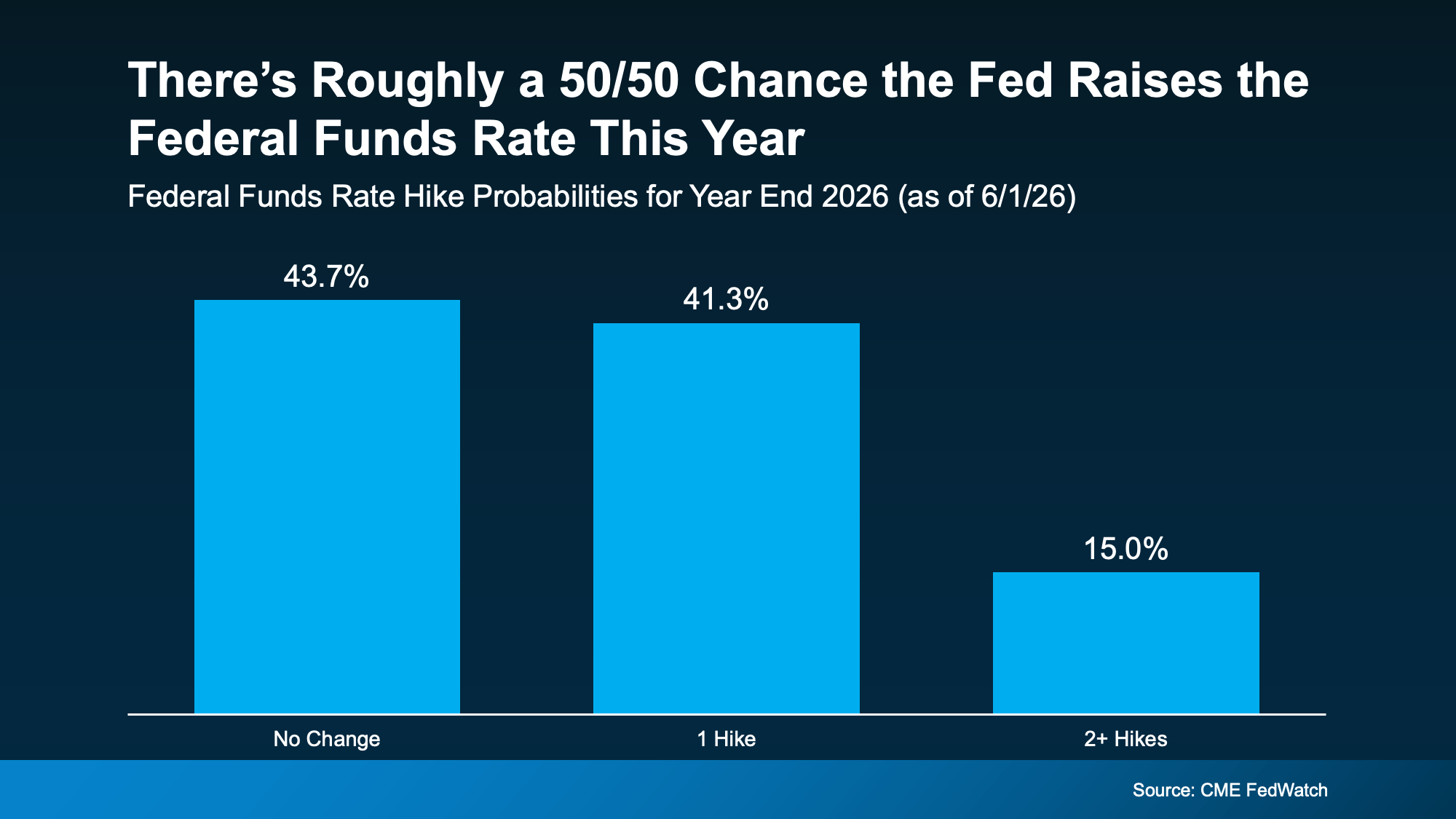

What recessions do reliably affect is mortgage rates, which tend to fall as the economy weakens and the Fed cuts. So the historically grounded version of the waiting strategy isn’t “wait for cheap houses.” It’s “wait for cheaper money.” And that’s a much weaker reason to wait, because you don’t need a recession to get it. If rates fall after you buy, you refinance and reset your payment downward. You can’t go back and buy the house you passed on. We dug into that math in our post on whether it’s better to buy now or wait for lower mortgage rates.

Why a 2008 rerun isn’t on the menu

The reason 2008 got so ugly is that forced sellers flooded the market. Millions of homeowners held loans they could never afford, and when the music stopped, foreclosures poured supply onto a market with no buyers. Price collapses need forced sellers, and today’s market is remarkably short of them.

Lending standards have been strict for over a decade now. Today’s homeowners documented their incomes, and the overwhelming majority are sitting on fixed rates below 5 percent with near-record equity cushions. Foreclosure activity is still running below historical norms, and a homeowner with 40 percent equity doesn’t get foreclosed on; they sell, pocket the difference, and move on. On top of that, the country has underbuilt housing for most of fifteen years, and the lock-in effect that froze inventory is only now starting to loosen. Tight supply is the opposite of the 2008 setup, and it puts a floor under prices even in a soft economy.

None of this means prices can’t dip in a recession. They can, and in some overheated Sun Belt markets they might. It means the specific thing the waiting strategy needs, a deep and lasting discount, requires a foreclosure wave that today’s lending math makes very hard to produce.

What a recession would give you as a buyer

Being fair to the other side: a recession wouldn’t give you nothing. Rates would likely fall. Some sellers would get nervous, and negotiating room would open up. Fewer buyers would compete for each listing, at least at first.

But look at how that plays out in practice. The moment rates drop meaningfully, the buyers who were priced out come flooding back, and they’re joined by everyone else who was “waiting for rates.” We’ve watched this movie in Memphis before: a rate dip turns a quiet listing into a multiple-offer situation in a single weekend. The discount window a recession opens tends to be narrow, crowded, and gone before the news stories about it finish running.

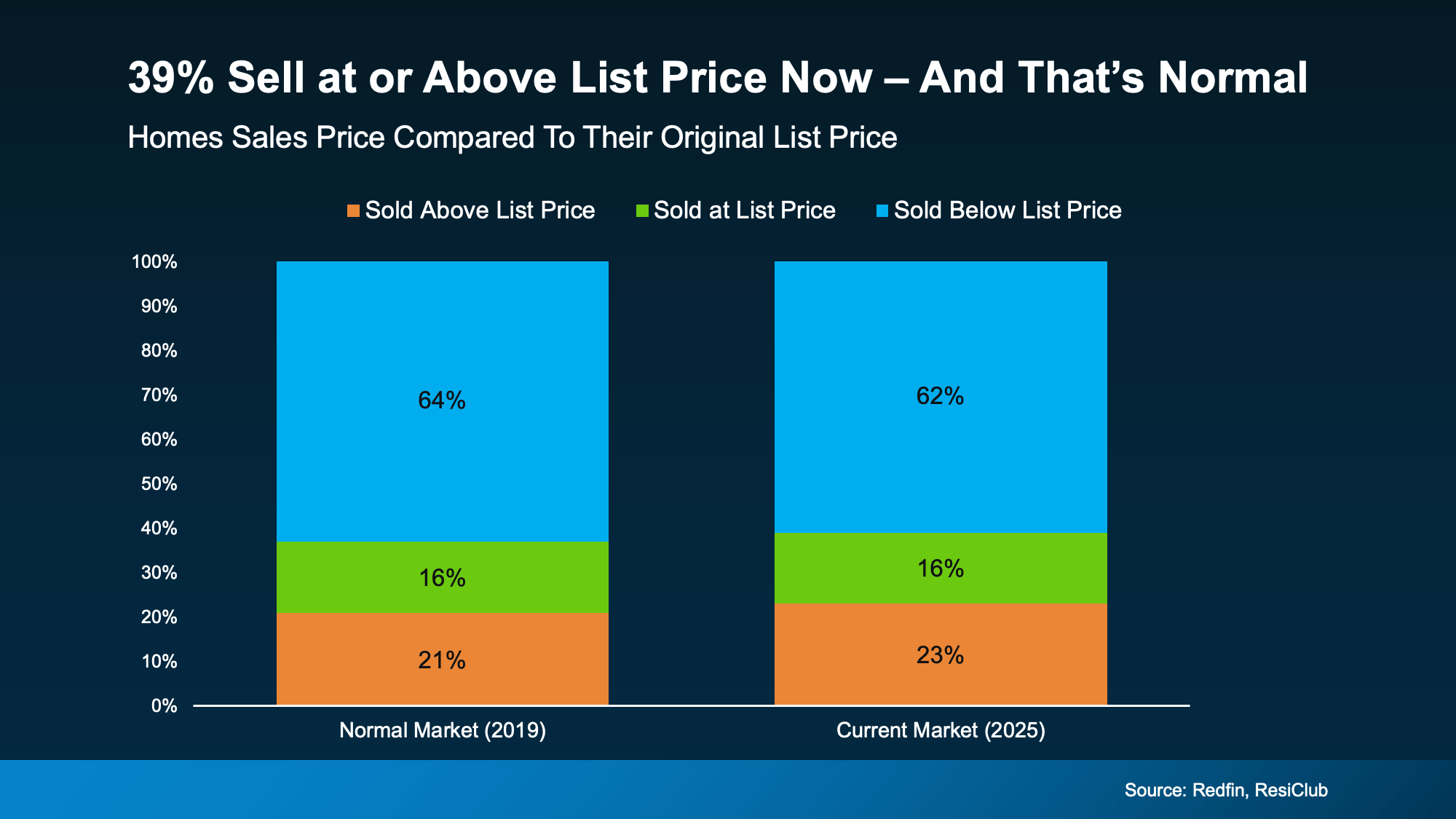

There’s also a quieter irony. Most of the negotiating power buyers are waiting for already exists in today’s market. Homes are sitting longer, sellers are covering closing costs and buying down rates, and inspection credits are back on the table. The balanced market you’d be waiting a recession to create is, in large part, already here.

What waiting costs while you wait

Waiting feels free. It isn’t.

Start with rent, which doesn’t pause for economic uncertainty. A renter who waits two years might be paying $200 to $300 more a month by then, with exactly zero equity to show for the outlay. We laid out the net worth gap between renting and buying, and it’s the single most lopsided number in this whole conversation: the average homeowner’s net worth runs many times a renter’s, and the gap is built one mortgage payment at a time.

Then there’s the appreciation on the house you didn’t buy. If prices in your target neighborhood rise even modestly while you wait for a crash, the “discount” has to beat that gain plus the rent you paid just to break even. And the affordability picture you’re waiting on may improve without any recession at all: forecasts already point to affordability improving in 2026 through a combination of easing rates, rising incomes, and more inventory. If that’s the fix, the waiting buyer pays two years of rent for a market they could have had anyway.

The timing problem nobody prices in

Suppose the recession does come, and prices do soften. Now ask the uncomfortable question: is that the moment you’ll be able to buy?

Recessions don’t just discount houses. They discount job security, and yours is part of the purchase. The moment prices finally dip is the same moment layoffs peak, and no discount makes buying wise when your own paycheck feels shaky. It’s also the moment lenders get stingy. Credit tightens in downturns, and the same bank that would approve you comfortably today may want a bigger down payment and a cleaner file right when the “deal” appears. The recession discount is real for the small group of buyers who are still fully employed and fully confident at the bottom. That’s a hard group to guarantee your way into two years ahead of time.

Worth keeping in perspective: even in the worst stretch of 2008-09, unemployment peaked around 10 percent, which means roughly nine out of ten workers stayed employed. The recession that wrecks everyone is mostly a headline creature. But you don’t need a national catastrophe for tightened credit and a nervous employer to wreck your personal window.

The Memphis wrinkle

One more problem with waiting for a national crash: you wouldn’t be buying the national market. You’d be buying in Memphis, and the Memphis area has a long record of not swinging the way coastal boomtowns do. Our prices didn’t inflate like Austin’s or Boise’s on the way up, which leaves less air to come out on the way down. The local economy leans on healthcare, logistics, FedEx, and education, sectors that keep functioning through downturns.

The established suburbs are steadier still. Places with strong schools, Collierville, Germantown, Bartlett, Arlington, Lakeland, hold their value through soft stretches because there’s a permanent line of families who want in. Those are exactly the neighborhoods recession-waiters are hoping to buy into at a discount, and exactly the ones least likely to offer it. The deep-discount scenario, if it ever arrives, tends to show up in the housing nobody was fighting over to begin with.

When waiting really is the smarter move

Everything above is an argument against waiting for the market. It is not an argument against waiting until you’re ready, which is a different thing entirely.

Wait if you don’t have an emergency fund that could cover several months of expenses, including a mortgage payment. Wait if your credit needs a year of repair work that would meaningfully drop your rate. Wait if there’s a real chance you’d relocate within two years, because the transaction costs of buying and selling that fast usually eat any gains. And wait if your job genuinely feels unstable, not headline-nervous but your-department-is-shrinking unstable. That signal outranks anything an economist says on television.

Notice that every item on that list is about your life, not the business cycle. That’s the point. A first-time buyer who’s financially solid in a so-so economy is in a far better spot than a shaky buyer in a booming one. If you’re not sure which one you are, our first-time Memphis buyer guide walks through the readiness checklist in detail.

Ready beats perfectly timed

Here’s the honest summary. Recessions reliably lower rates, unreliably lower prices, and reliably raise the odds that something in your own financial life gets complicated. A buyer who waits for a recession is betting on the least likely part of the package while exposing themselves to the most likely one. Meanwhile, today’s market is quietly offering much of what they’re waiting for: negotiating room, seller concessions, and time to think, with a refinance available if rates fall later.

So buy when your finances are ready, your timeline is five years or longer, and the payment works at today’s rates without heroic assumptions. Then let the economy do whatever it’s going to do. If you want to pressure-test your own situation against the current Memphis market, honestly and without a sales pitch, reach out and let’s talk it through. The right time to buy has a lot more to do with you than with the business cycle.