The latest inflation numbers came in higher, and the headlines did what headlines do. Before you read that as a reason to panic about buying or selling a home in Memphis, it helps to know what the report actually says, why it moves mortgage rates, and what you can do about it right now.

Short version: inflation is running warmer than the Federal Reserve wants, a chunk of that is tied to events overseas, and mortgage rates are likely to sit higher for longer than most people were hoping. None of that is a 2008 setup. Let’s walk through it.

What the inflation report actually said

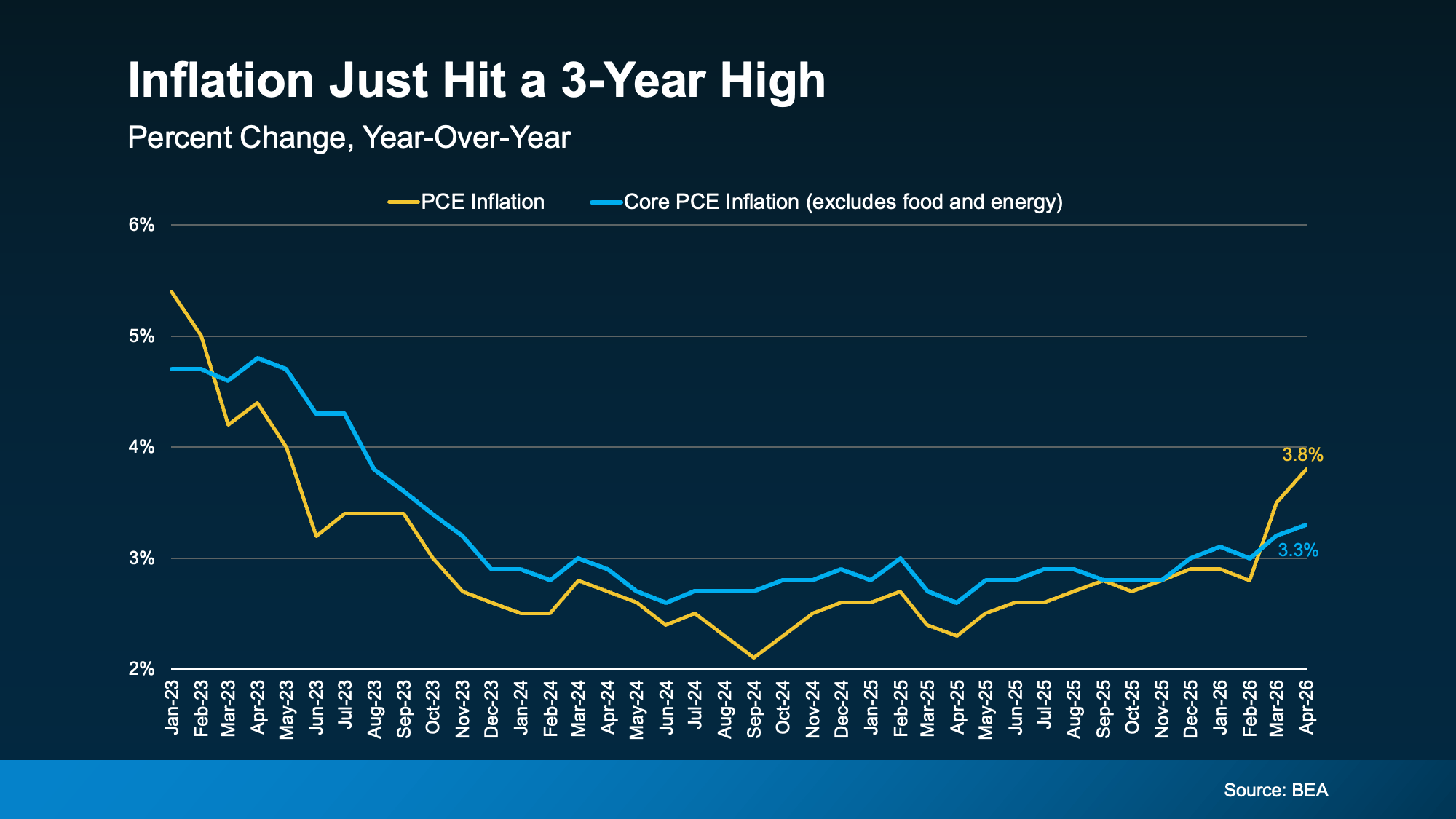

The government measures inflation a few different ways. The one everyone’s talking about right now is PCE, the Personal Consumption Expenditures Price Index. It tracks how much more, or less, people are paying for goods and services compared with a year ago. Look at your own grocery and gas receipts lately and you can probably guess which direction it’s been heading.

That’s the yellow line in the chart below, and it has spiked since February. A big driver is the ongoing conflict in the Middle East, which has pushed gas and energy prices up hard.

The yellow line is overall PCE inflation, which has jumped since February. The blue line is core PCE, the same measure with gas and energy stripped out. Source: Bureau of Economic Analysis.

Now look at the blue line. That’s core PCE, the same measure with volatile gas and energy prices taken out. The Fed watches this one most closely, because energy prices swing around so much they can paint a misleading picture from month to month.

And this is the part worth holding onto. Core PCE is rising too, but nowhere near as fast as the overall number. That gap tells you a good share of the current spike is tied to what’s happening overseas rather than broad, sticky price growth at home. If that situation cools off, inflation could ease back with it.

Why an inflation report moves your mortgage rate

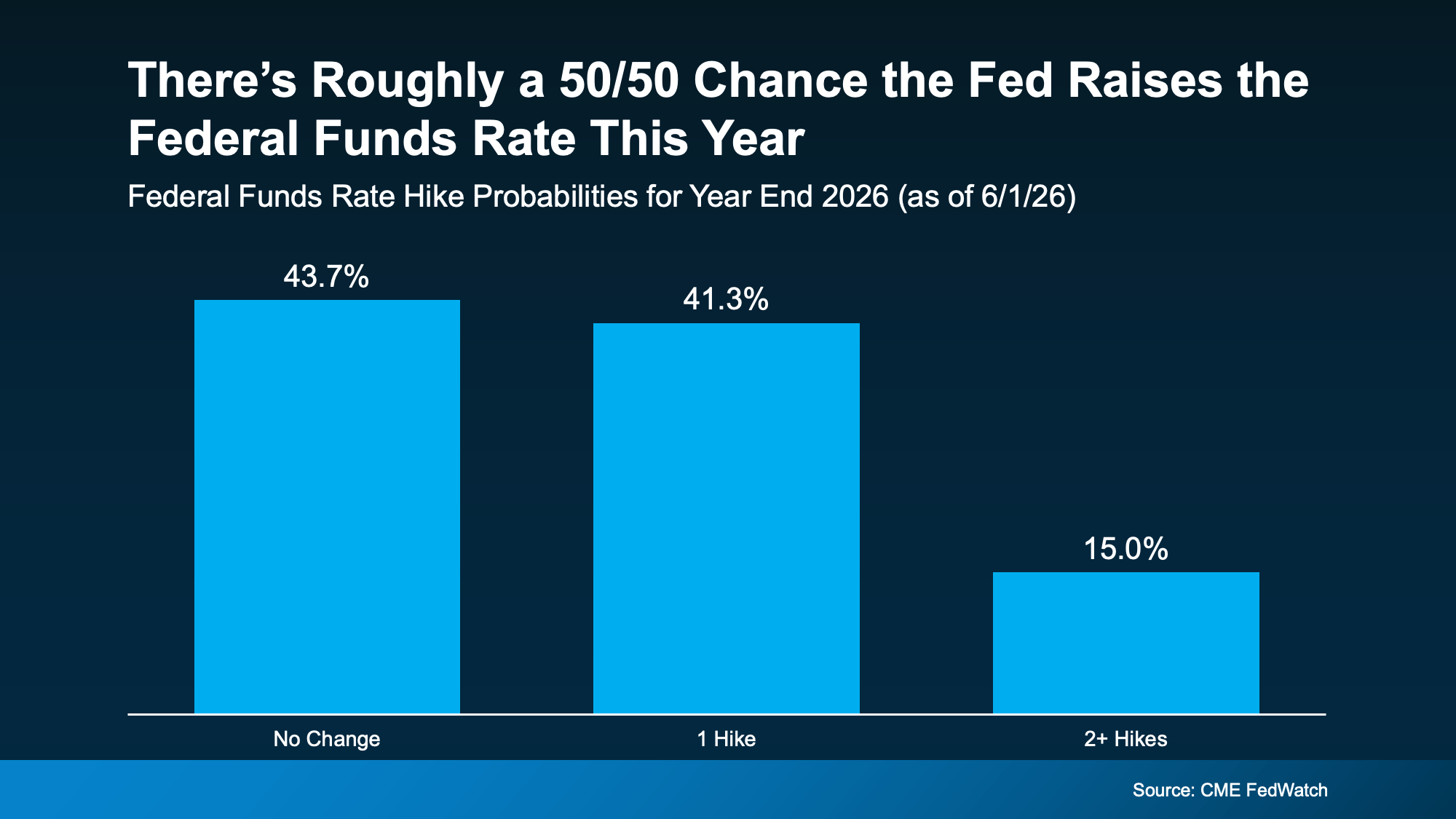

Here’s the housing connection. When inflation runs hot, the Fed tends to hold its benchmark rate, the Federal Funds Rate, high, or even raise it, to slow spending and bring prices back down. It isn’t a one-to-one relationship, but where that rate goes tends to pull mortgage rates along with it.

As of now, markets put it at roughly a 50/50 chance the Fed raises rates before the end of 2026, according to the CME FedWatch tool. A coin flip, basically.

Markets currently see about a coin-flip chance of a rate hike before year-end. Source: CME FedWatch.

It’s too early to call where this lands. But it does mean mortgage rates probably aren’t dropping as soon as a lot of buyers had penciled in. If you’ve been sitting out, waiting for rates to fall before you make a move, this report is a reminder that “higher for longer” is still very much in play. A lot of it rides on the economy from here. Bankrate put it plainly:

“Oil prices and bond yields have dropped a bit… but they’re still way up compared to the start of spring. Until there’s a resolution to the war, look for both inflation and mortgage rates to stay high.”

That’s the honest answer to the question I get most often, which is some version of is it smarter to buy now or wait for lower rates. Nobody can promise you a number. What we can say is that betting the whole plan on a quick drop looks shakier after this report than it did a month ago.

A tough economy is not a housing crash

This is where people’s minds go, so let’s meet it head-on. A rough stretch in the economy does not mean 2008 is coming back. The conditions that caused that collapse aren’t the conditions we have now, and the differences aren’t small.

Inventory is still tight. There’s no flood of homes hitting the market the way there was heading into the last crash. Memphis has loosened up some as the rate lock-in effect finally breaks, but we’re a long way from oversupply.

Most homeowners are sitting on real equity. After years of price growth, the typical owner has a substantial cushion, not an underwater loan. That alone changes the whole picture, because equity is what keeps people from being forced to sell at a loss.

Lending standards are far stricter than they were in the mid-2000s. The loose, no-documentation lending that fueled the last bubble is gone. The people who bought over the past several years generally had to prove they could afford it.

And the core problem today is affordability, not a wave of distressed sellers. Buyers are stretched by prices and rates, which is a real strain, but it’s a different animal from millions of owners underwater and defaulting at once. Uncomfortable and unhealthy aren’t the same thing. The market feels hard right now. Hard and crashing are not the same word, and the difference matters if you’re trying to decide what to do. If a shaky economy is what’s giving you pause, it’s worth reading how buying during a downturn actually tends to play out before you talk yourself out of a move.

You still have moves to make

High rates don’t put homeownership out of reach. They change the path a little, and there are real strategies that help depending on where you’re starting from.

Talk to your lender about the loan itself. An adjustable-rate mortgage or a rate buydown can lower your monthly payment in the early years, which sometimes bridges the gap while you wait for a chance to refinance. These aren’t right for everyone, but they’re worth understanding before you rule them out.

Chase down the help that exists. First-time buyer programs, down payment assistance, and seller concessions can each knock real money off what you need up front. If you’re newer to all of this, our guide to buying your first home in Memphis walks through where to start.

Stay close to an agent and a lender you trust. Rates will move. When they do, the buyers who already have their financing lined up and their search dialed in are the ones who can act before the window closes. The families who’ve been waiting for affordability to improve don’t want to be starting from scratch the day it does.

The right strategy for your situation matters far more than nailing the perfect moment, because the perfect moment usually only looks perfect in hindsight.

Strategy beats timing

Inflation is still above where the Fed wants it, so mortgage rates are likely to stay elevated for a while yet. That’s the reality this report points to. But for anyone who actually needs to move, whether life is pushing you or the numbers finally work, a smart plan built around your budget will do more for you than trying to time the market ever could.

Want to know what this means for your specific situation in Memphis? Reach out and let’s talk it through. Even if you’re just running the numbers, it’s worth having a real answer instead of a headline.