(Updated 6/05/26)

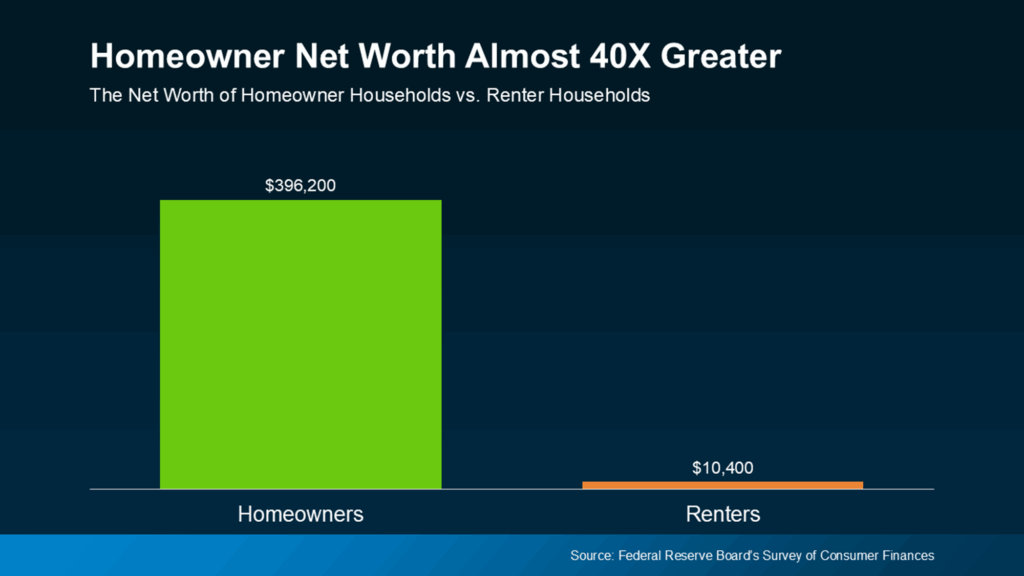

There’s a number from the Federal Reserve that does a better job of explaining the case for homeownership than any sales pitch ever could. The typical homeowner in America has a net worth around 40 times higher than the typical renter. Not 40 percent. Forty times over.

The figures behind it are roughly $396,200 for homeowners versus about $10,400 for renters, from the most recent Survey of Consumer Finances. That gap is the single clearest argument for buying a home, and it’s worth understanding before you renew another lease. It didn’t appear overnight, and it doesn’t close while you wait. It’s built slowly, payment by payment, while one group buys an asset and the other rents one.

If you’ve been weighing renting vs buying in Memphis, this is the math that should be in front of you. We’ve walked a lot of first-time buyers through this decision, and the gap between renting and owning is almost always wider over time than people expect going in. This breaks down why the gap exists, what drives it, and how to think about whether buying makes sense for your situation today.

The wealth gap between owners and renters

The 40x number sounds extreme until you trace where it comes from, and then it just looks like arithmetic. Every rent payment leaves your account and never comes back. Every mortgage payment splits in two: part covers interest, and part pays down what you owe, which means you own a little more of your home each month. Stretch that over 15 or 30 years and you end up holding a paid-down asset worth more than you paid for it, while a renter holds a folder of receipts.

Then there’s appreciation sitting on top of that. When your home’s value rises, your equity rises with it, and that shows up dollar-for-dollar in your net worth. A renter gets none of that lift. The landlord does. So the gap grows from two directions at once, principal you’re paying down and value the home is gaining, and renting captures neither.

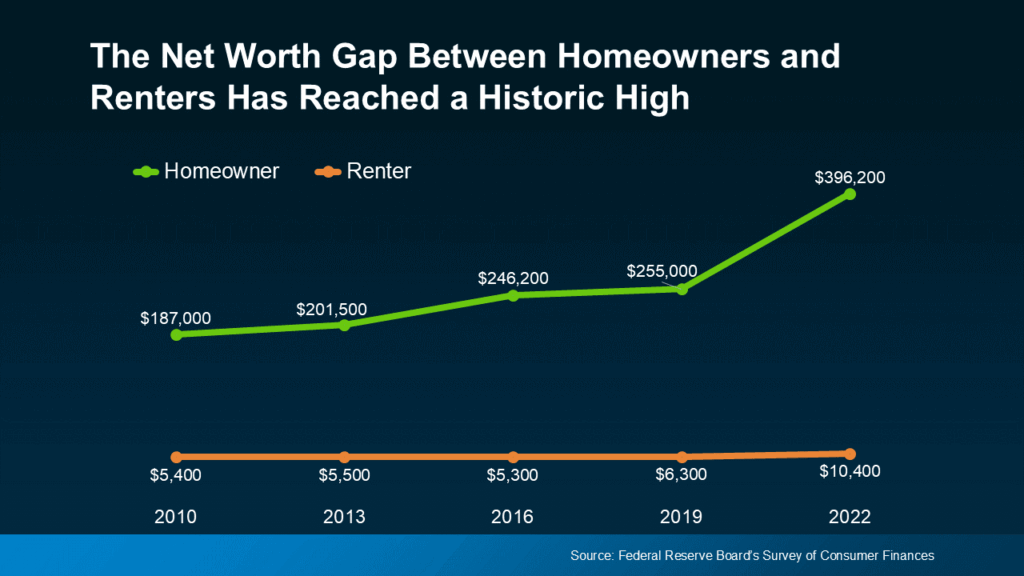

What built the homeowner wealth jump

The Federal Reserve called the 2019 to 2022 stretch the largest three-year jump in median net worth in the history of the survey, and a big share of it came straight from home equity. Prices climbed fast, mortgage rates sat low for part of that window, and anyone who already owned watched their net worth rise without lifting a finger.

That particular window has closed. Rates are higher now, price growth has cooled, and nobody’s forecasting another run like that one. But the engine underneath didn’t change. Owners still build equity with every payment, and homes still tend to appreciate over time. The gap just widens at a calmer pace now instead of a dramatic one, which is arguably a healthier place for a buyer to step in.

Home values climb over the long run

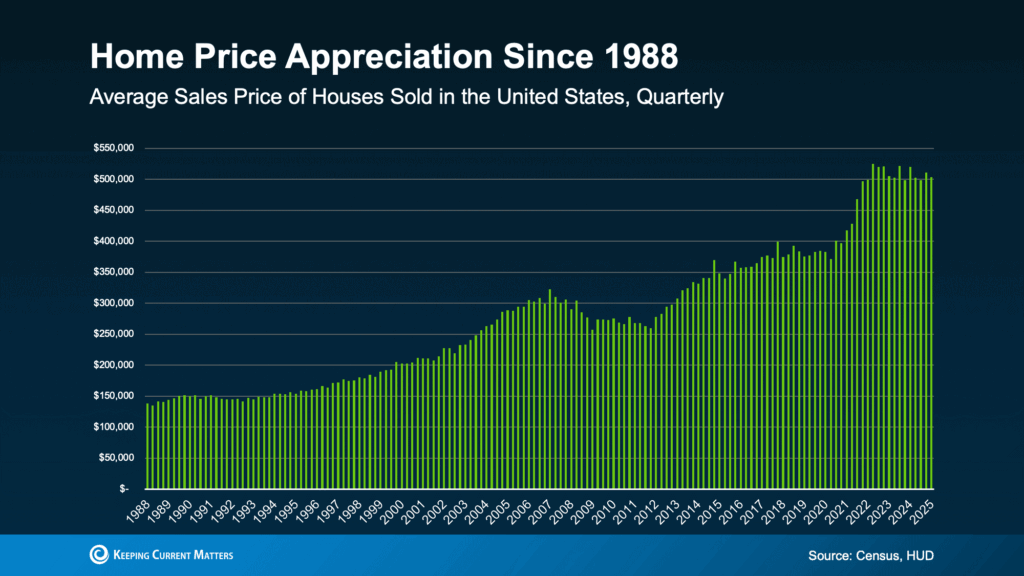

There’s a stubborn myth that home prices are a coin flip. Zoom into any two-year stretch and sure, they can dip or spike. Pull back across decades of Federal Reserve data and the line is hard to argue with: values trend up. The 2008 crash that felt apocalyptic at the time shows up as a dip that prices later climbed right past.

Memphis behaves a little differently from the coasts, and mostly in a buyer’s favor. Our price swings tend to be gentler, our appreciation steadier, and our entry prices still within reach for people who’d be locked out in other metros. A first-time buyer in Bartlett or Cordova can still find starter homes at prices a normal income can actually support, which is a big reason the area keeps drawing buyers priced out elsewhere. Right now appreciation across the metro is running in the low single digits, slow enough that you’re not racing a moving target while you shop.

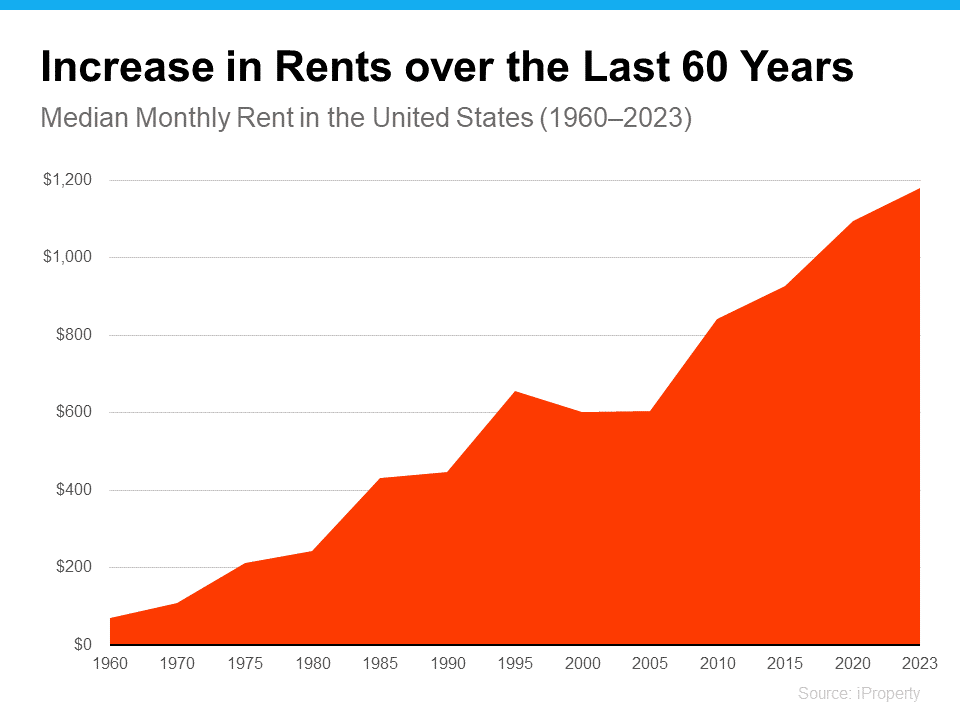

Rent keeps rising, your mortgage doesn’t have to

Any renter feels this one in their gut. The lease comes up, the new number is higher, and the direction never reverses for long. Some years it’s a gentle bump, some years it stings, but the trend line only points one way.

A fixed-rate mortgage breaks that cycle in a way renting simply can’t. Lock one in and your principal and interest payment is the same in year 15 as it was in year one. Meanwhile your friends who kept renting are 15 years into compounding increases, paying far more each month than they did when they signed that first lease. Your taxes and insurance may drift up over time, but the core of your housing cost is frozen, and that stability is worth real money when you stretch it across a decade or two.

When buying beats renting on the math

This is the part that surprises people. In a lot of markets, including much of the Memphis area, buying costs less month to month than renting the moment you need two or more bedrooms. National figures from Realtor.com and the National Association of Realtors have shown this pattern for a while.

Picture what a two-bedroom rental runs in Germantown or East Memphis today, then set it next to the monthly payment on a starter home with a reasonable down payment at current rates. The two numbers often land within a few hundred dollars of each other. The difference is that one payment builds your equity and the other builds your landlord’s. If you’re starting a family, working from home, or just tired of paying for storage units, the math tilts toward buying about the time you need more than one bedroom, and that’s before you count a dollar of equity.

The quiet wealth machine of owning

Pull far enough back and the whole thing clarifies. Rent vanishes the second you pay it. A mortgage payment shrinks what you owe and, eventually, hands you a house you own outright. Pair that with appreciation and you’ve got a wealth-building machine running in the background of your life whether you think about it or not.

Surveys of younger homeowners keep finding the same top reason for buying: building their own equity instead of their landlord’s. That’s the entire idea in one sentence. Your housing cost exists either way. The only question is whose asset it’s filling up. For most households, housing is the single biggest line in the monthly budget, so pointing that money at something you own compounds into real net worth over the years. Pointing it at rent produces a roof that costs more next year.

The cost of staying put

A Bank of America survey found that 70% of aspiring homeowners worry about what long-term renting does to their finances, and 72% worry that rising rent will squeeze them now and later. Both groups have it right.

Rent increases don’t just pinch this month’s budget. They make next year’s down payment harder to save, because every $200 rent hike is $200 that didn’t go into a house fund. At the same time, home prices are usually creeping up in the background. So a renter watches the target drift further away while the tank they’d use to reach it drains a little each year. That’s the trap, and the longer you sit in it, the harder it is to climb out. Breaking the cycle often means moving a bit earlier than feels comfortable, with a little less saved than you’d like, just to step off the treadmill.

It’s not only about the money

Owning comes with things that never show up on a Federal Reserve chart but matter to how you live day to day. You can paint a bedroom dark blue because your kid asked. You can hang heavy shelves, put in a dog door, or redo the kitchen on your own timeline without a landlord’s signature. (An HOA may have rules about the outside, but the inside is yours.)

There’s privacy in it, too. No quarterly inspections, no notice that the place is going on the market and you’ll be hosting showings next weekend. And there’s room to grow into, a home office, a workshop, a garden, space for a family, without wondering whether your lease gets renewed. Over the years you put down roots, get to know your neighbors, and invest in a place that invests back in you. The day you get the keys to your first home tends to stick with people. That part isn’t on the spreadsheet, but it’s real.

Is now the right time for you?

Let’s be straight about the market. It isn’t easy for first-time buyers right now. Rates are sitting in the low-to-mid 6s, higher than the bargain years, and prices in the most desirable Memphis neighborhoods haven’t fallen the way some people hoped. Competition in places like Collierville and Germantown stays real, though more listings have come online lately than buyers have seen in years. If you’re weighing those trade-offs, our Memphis suburbs comparison guide is worth a read, and so is our look at where affordability sits in the second half of 2026.

But “hard” and “impossible” aren’t the same word. The real question isn’t whether the market is easy, it’s whether your numbers work. If your income, credit, and savings can carry a mortgage on a home you’d happily stay in for several years, the long-term math still favors buying, even at today’s rates. You can refinance a rate later. You can’t go back and buy at last year’s price.

And if your numbers don’t work yet, that’s fine too. The right move then is a plan: clear the high-interest debt, build the down payment, and be ready when the math lines up. We work with buyers at every stage of that, including the ones who are a year or two out.

How to make the rent vs buy call

The sharper question isn’t “can I cover the monthly payment.” It’s “how many more years am I willing to pay down someone else’s mortgage instead of my own.” Every year of renting is another year the gap grows the wrong way for you.

A few things worth thinking through honestly:

- How long you plan to stay is the big one. Most buyers break even on closing costs within three to five years, so if you’re moving in a year, renting probably wins, and if you see yourself here five years or more, buying usually does.

- Your debt picture counts too. High-interest credit card balances make everything about buying harder, so clear those first and the rest gets easier.

- Income stability is what underwriting looks for. Job changes and self-employment aren’t dealbreakers, they just change the paperwork.

- And keep the first home realistic. First homes are starter homes, the place that gets you building equity, not the forever home, and that mental shift opens up a lot of options.

If owning still feels out of reach, the first step isn’t house hunting. It’s getting clear on your actual numbers with someone who knows this market. A local agent working alongside a good loan officer can usually tell you within one conversation whether you’re six months or three years out, and exactly what needs to change.

The core idea

Renting feels safer in the moment. It’s flexible, and some months the number is genuinely lower. Stretch the view to 10 or 20 years, though, and the math turns hard to ignore. A fixed-rate mortgage locks your housing cost, equity builds with every payment, your net worth rises as the home appreciates, and you get to live in the place on your own terms.

Homeowners holding roughly 40 times the net worth of renters isn’t a fluke or a statistical trick. It’s the predictable result of aiming your housing budget at something you own. The gap is real, it’s documented, and it compounds. The good news is that the distance between renting now and owning your first home is usually smaller than it looks from inside the rental. When you’re ready to find out what it looks like for your situation, get in touch and we’ll be straight with you about where you stand.