(Updated 10/10/25)

Let’s talk about something that stops thousands of would-be homeowners dead in their tracks every single year: the down payment.

If you’ve ever looked at home prices and felt your stomach drop, thinking you’d need to save for decades just to get your foot in the door, you’re definitely not alone. There’s this persistent myth floating around that buying a home requires a massive pile of cash upfront, and honestly, it’s keeping way too many people stuck in rental cycles when they could actually be building equity in their own place.

Here’s what nobody seems to be talking about: most of what you’ve probably heard about down payments is outdated, misleading, or just plain wrong. And once you understand what’s actually required versus what people think is required, you might realize you’re already closer to homeownership than you ever imagined.

So let’s dive deep into the world of down payments, bust some myths wide open, and figure out what it actually takes to get the keys to your own home.

Why Down Payment Myths Keep Spreading

Before we get into the nitty-gritty details, it’s worth asking: why do these misconceptions stick around?

Part of it comes from older generations who bought homes decades ago when lending standards were completely different. Your parents or grandparents might have needed that hefty 20% down payment, and they’ve passed that “wisdom” along without realizing the landscape has totally changed.

Social media doesn’t help either. Everyone loves sharing their success stories about how they saved up massive down payments, but fewer people talk about the reality that most buyers today are putting down way less than that. It creates this skewed perception of what’s actually normal.

And let’s be honest, the mortgage industry hasn’t always done the best job of educating potential buyers about their options. Many people simply don’t know what they don’t know, and they’re too intimidated to ask.

The Big Down Payment Myth

Let’s start with the elephant in the room, shall we?

There’s this incredibly stubborn belief that you need to save up 20% of a home’s purchase price before you can even think about buying. And it’s literally preventing people from achieving homeownership when they’re actually ready.

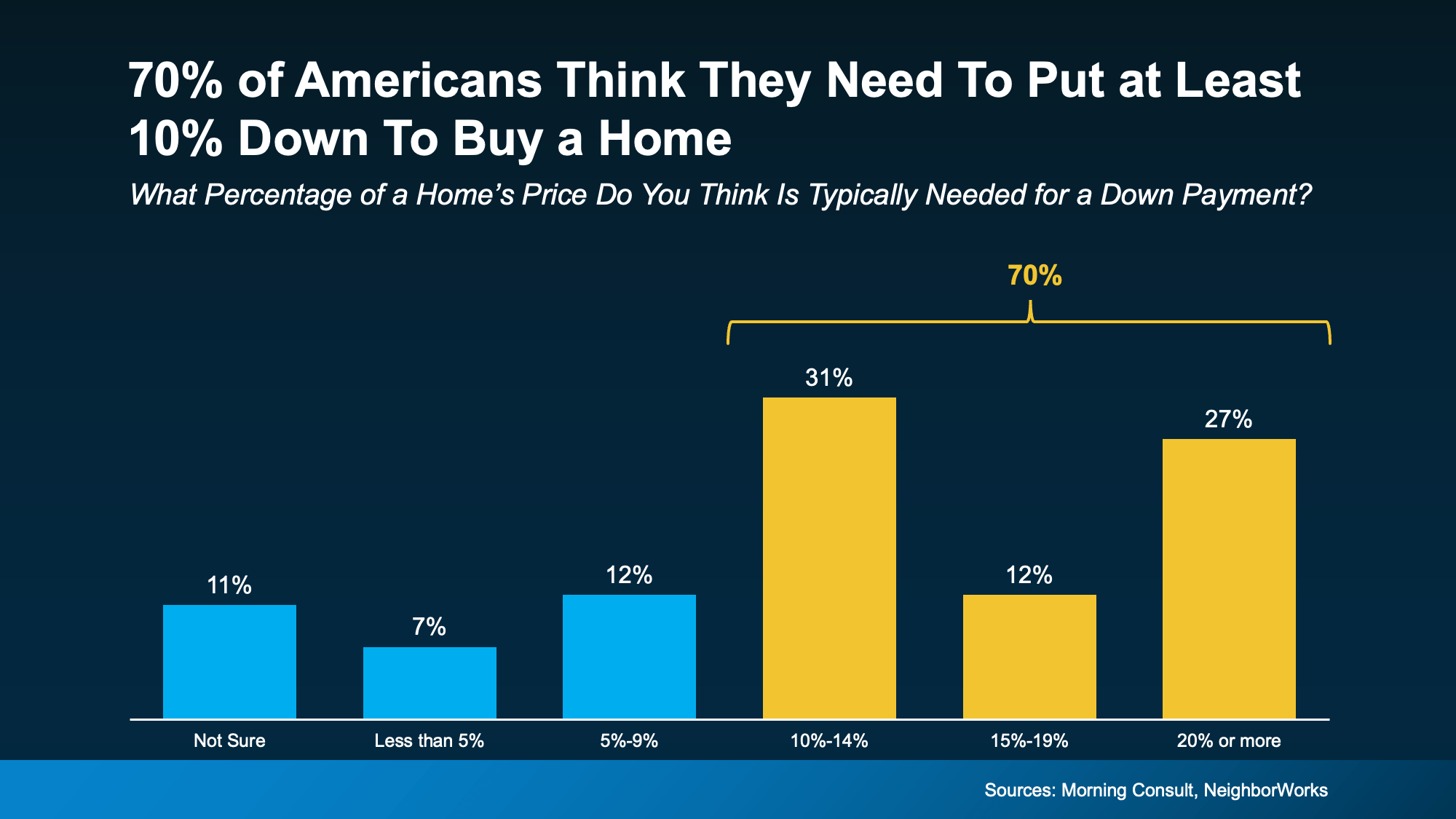

Recent surveys show that roughly 70% of Americans think they need at least 10% down to buy a home. Even more concerning, about 11% of people have no idea what’s actually required. That’s a whole lot of confusion keeping folks on the sidelines.

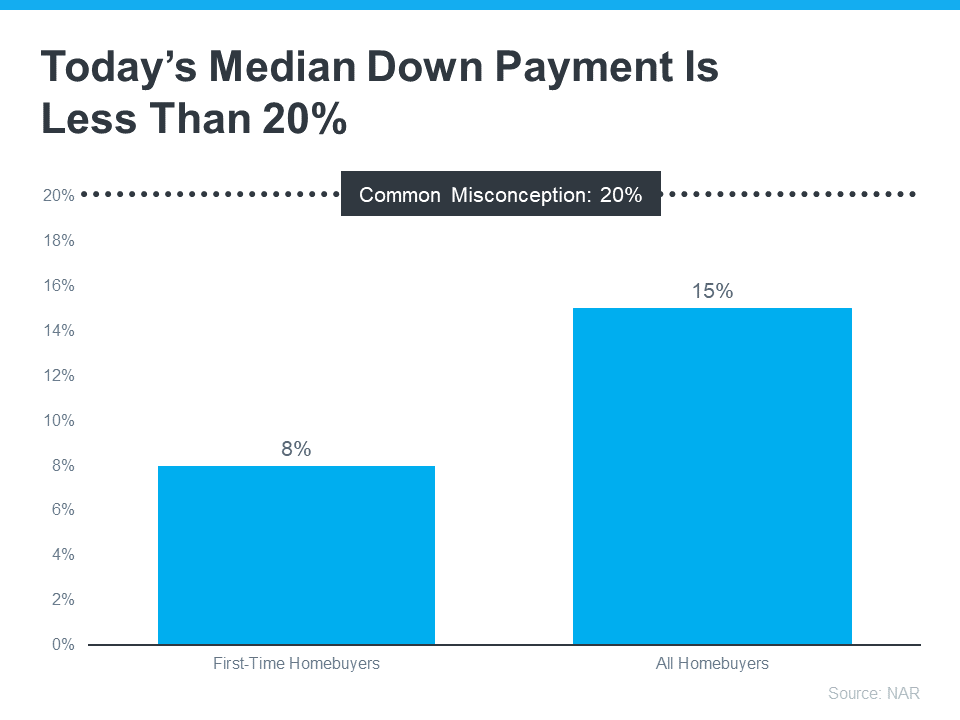

But here’s the reality check you need: the typical first-time homebuyer has been putting down between 6% and 9% since 2018. Not 20%. Not even close to 20%.

Let that sink in for a minute. While you’ve been stressing about saving up tens of thousands of dollars, the average person buying their first home is putting down less than half of what you thought was necessary.

And it gets even better than that.

Loan Programs

If you qualify for an FHA loan, which is specifically designed for first-time buyers and people without perfect credit, you might only need 3.5% down. That’s it. On a $300,000 home, that’s $10,500 instead of $60,000. That’s a game-changing difference.

For veterans and active military service members, VA loans typically require zero down payment. Read that again: zero. If you’ve served your country, you might be able to buy a home without putting any money down at all.

Even conventional loans these days often allow down payments as low as 3% to 5% for qualified buyers. Lenders have realized that requiring massive down payments was shutting out perfectly capable buyers who could absolutely afford their monthly mortgage payments.

The point is, there are legitimate, mainstream options available that require way less cash upfront than most people realize. You just need to know they exist and which ones you might qualify for.

What Actually Happens With Your Down Payment

Let’s take a step back and talk about what a down payment actually is, because understanding the purpose helps demystify the whole process.

When you buy a home, you’re making an initial upfront payment from your own savings or gifts from family members. This money shows the lender that you’re serious about the purchase and have some skin in the game. It’s your immediate equity in the property.

Traditionally, larger down payments were preferred because they reduced the lender’s risk. If you put 20% down and immediately have that much equity, you’re statistically less likely to walk away from the mortgage if times get tough. Plus, if the lender had to foreclose, they’d be more likely to recoup their losses.

But here’s the thing: just because something was traditional doesn’t mean it’s necessary.

Lending institutions have evolved. They’ve developed better ways to assess risk, including credit scores, employment history, and debt-to-income ratios. They’ve realized that someone who puts 5% down but has stellar credit and stable income is actually a great borrower.

The 20% rule was never a legal requirement anyway. It was just a threshold where you could avoid paying private mortgage insurance, which we’ll talk about in a minute.

The Time Factor Nobody Talks About

Another myth that deserves to be smashed: the idea that it’ll take forever to save up for a down payment.

Sure, saving takes time and discipline. But it might not take nearly as long as you’re imagining, especially if you’re not trying to hit that unnecessary 20% mark.

The timeline varies dramatically depending on where you live. In some states with lower home prices and decent median incomes, saving up for a 10% down payment might only take a few years. In more expensive markets, it might take longer, but remember—you probably don’t even need 10%.

Let’s do some quick math to put this in perspective. Say you’re looking at a $250,000 home. If you’re shooting for 5% down, that’s $12,500. If you can save $500 a month, you’ll hit that goal in 25 months—just over two years. If you can bump that up to $750 a month, you’re looking at less than 17 months.

Compare that to trying to save $50,000 for a 20% down payment. At $500 a month, that’s more than eight years. At $750 a month, it’s still almost five and a half years.

That’s a lot of time spent paying rent instead of building equity. And here’s the kicker: home prices are generally trending upward. While you’re saving up for that bigger down payment, the house you want might be getting more expensive. You could actually end up further from your goal than when you started.

The Secret Weapon

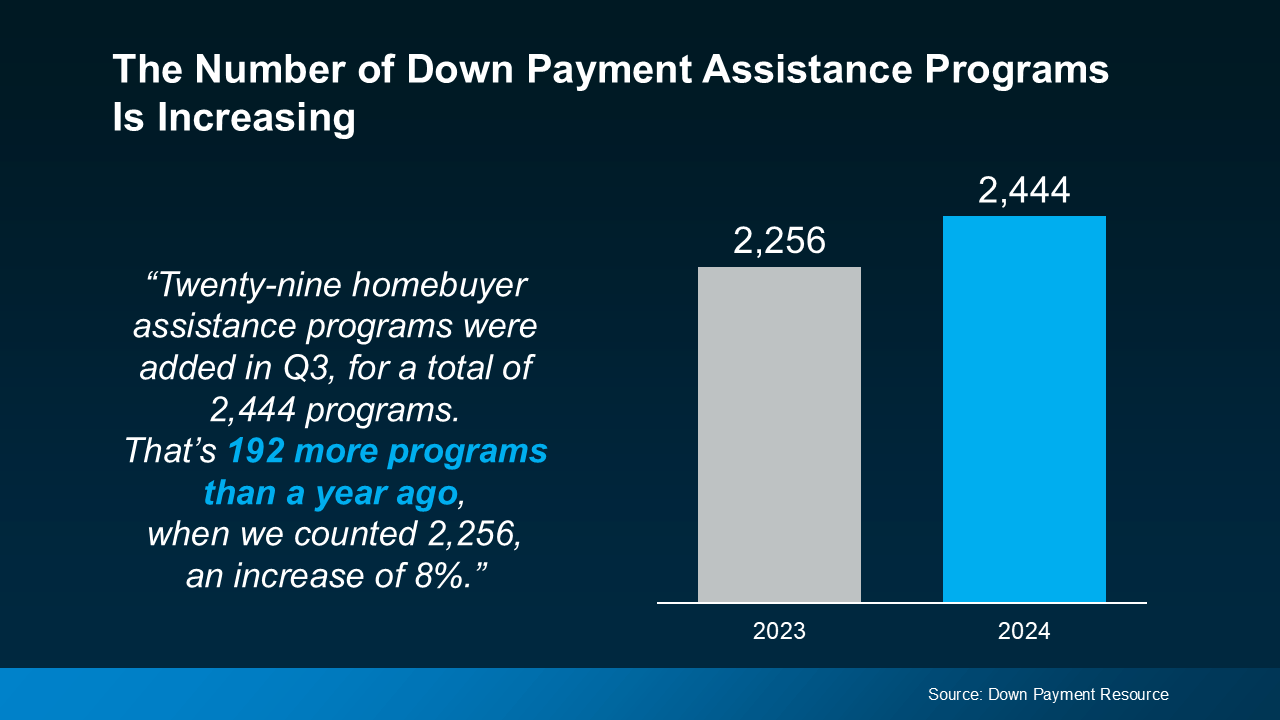

Ready for something that might blow your mind? There are literally thousands of down payment assistance programs across the country, and a massive 39% of potential buyers don’t even know they exist.

Let that sink in. Almost four out of ten people who could benefit from these programs have never heard of them. That means a huge number of potential homeowners are struggling unnecessarily, thinking they have to do everything on their own.

These assistance programs come in various forms. Some offer grants that you never have to pay back. Others provide low-interest or forgivable loans that might be forgiven after you live in the home for a certain period. Some are targeted at specific professions like teachers, firefighters, or healthcare workers. Others focus on first-time buyers or people buying in specific neighborhoods.

The typical benefit from these programs averages around $17,000. Seventeen thousand dollars! For many buyers, that’s the entire down payment plus some closing costs covered.

And it’s not just about first-time buyers anymore. Many newer programs are expanding to support affordable housing initiatives, including manufactured homes and condos. The net is widening, which means more people than ever can qualify for help.

Rising Interest Rates

In today’s market, with interest rates higher than they’ve been in years and home prices still climbing in many areas, down payment assistance has become more essential than ever before.

Think about it this way: when both prices and rates are up, your buying power is squeezed from both directions. You need more money for the down payment because homes cost more, and your monthly payment is higher because of the interest rate.

This is exactly when assistance programs become absolutely critical. They can help bridge that gap and make homeownership possible even when market conditions aren’t ideal.

The number of these programs has actually been growing. In just the past year, hundreds of new assistance programs have been added across the country. State and local governments, along with nonprofit organizations, are recognizing that homeownership is increasingly out of reach for regular people, and they’re creating programs to help.

Finding Programs

Alright, so these programs exist and they can provide serious financial help. But how do you actually find them?

This is where working with professionals becomes absolutely crucial. Your real estate agent and mortgage loan officer should be your guides through this maze. They deal with these programs regularly and know what’s available in your specific area.

Different programs have different eligibility requirements. Some are based on income limits. Others require you to buy in certain neighborhoods or zip codes. Some prioritize specific professions or demographics. The rules vary wildly from program to program.

Your loan officer is particularly important here because they can tell you which programs you actually qualify for and how they’d work with your specific loan type. There’s no point in getting excited about a program only to find out you don’t meet the criteria.

And here’s a pro tip: don’t assume you won’t qualify for anything. Many people think these programs are only for very low-income buyers, but that’s not true at all. Middle-class families often qualify, especially in higher-cost housing markets where the income limits are adjusted for local conditions.

Different Types of Loans

Let’s break down the main loan types you’ll encounter and what each one requires for a down payment, because understanding your options is half the battle.

Conventional Loans

These are the standard loans that aren’t backed by the government. They typically offer the most flexibility, but they also tend to have stricter credit requirements.

The minimum down payment for a conventional loan can be as low as 3% for qualified first-time buyers. More commonly, you’re looking at 5% down. If you put down less than 20%, you’ll need to pay private mortgage insurance, or PMI, which protects the lender if you default.

PMI usually runs about 1% of your loan balance annually, divided into monthly payments added to your mortgage. It’s an extra cost, sure, but it’s temporary. Once you’ve paid down your loan enough to have 20% equity, you can request to have PMI removed.

Conventional loans come in both fixed-rate and adjustable-rate varieties. Fixed-rate means your interest rate stays the same for the entire loan term, making budgeting predictable. Adjustable-rate mortgages start with a lower rate that can change over time based on market conditions.

FHA Loans

Federal Housing Administration loans are specifically designed to help people who might not qualify for conventional loans. They’re incredibly popular with first-time buyers.

The big advantage of FHA loans is that they allow down payments as low as 3.5%, and they’re more forgiving of lower credit scores. If your credit score is in the 580-620 range, you might still qualify for an FHA loan when conventional lenders would turn you away.

The trade-off is that FHA loans require mortgage insurance both upfront and monthly, and the monthly insurance doesn’t go away when you hit 20% equity like it does with conventional loans. But for many buyers, especially those without perfect credit, this is still the best path to homeownership.

VA Loans

If you’re a veteran, active-duty service member, or qualifying surviving spouse, VA loans are an absolute game-changer. They require no down payment and no monthly mortgage insurance.

Let me say that again for emphasis: you could potentially buy a home with zero money down and no extra insurance premiums. The VA backs the loan, which gives lenders confidence to offer these generous terms.

There is a one-time funding fee, but it can be rolled into your loan amount so you don’t need cash upfront for it. And if you have a service-related disability, even that fee might be waived.

If you’re eligible for a VA loan, it’s almost always your best option. The terms are simply unbeatable.

USDA Loans

USDA loans are another zero-down-payment option, but they’re limited to rural and some suburban areas. The exact boundaries can be surprising—some areas you wouldn’t think of as “rural” actually qualify.

Like VA loans, USDA loans are backed by the government, in this case the U.S. Department of Agriculture, as part of their rural development programs. There are income limits for USDA loans, but they’re generally pretty reasonable, especially for smaller households.

Your Credit Score

Your credit score isn’t just a number—it’s the key that unlocks different doors in the mortgage world.

With a strong credit score, typically 740 or above, you’ll qualify for the best interest rates and have the most loan options available. Lenders will be more flexible about down payments because your credit history proves you’re reliable.

With a mid-range score, say 620-740, you’ll still have plenty of options, but your interest rate might be higher, and lenders might require a larger down payment to offset their perceived risk.

Below 620, your options narrow considerably. You might need to look specifically at FHA loans or work on improving your credit before buying. But even with a 500 credit score, homeownership isn’t impossible—it’s just harder and more expensive.

Here’s something many people don’t realize: if your credit score is borderline, it might be worth spending a few months improving it before applying for a mortgage. Even a 20-30 point improvement can sometimes move you into a better rate category, potentially saving you thousands of dollars over the life of your loan.

Putting More Money Down

While we’ve established that you don’t need 20% down, let’s talk about whether you should put more down if you can afford it.

The advantages of a larger down payment are real. Your monthly payment will be lower because you’re borrowing less. You’ll pay less interest over the life of the loan. If you put 20% or more down on a conventional loan, you’ll avoid PMI entirely, which saves you money every month.

A larger down payment also gives you more equity from day one, which means more cushion if you need to sell quickly or if the market dips. And in competitive markets, sellers sometimes prefer offers with bigger down payments because they see them as more stable.

But there are also good reasons to put less down even if you could afford more.

Keeping more cash in your savings account gives you flexibility for emergencies, home repairs, and renovations. Remember, once you put money into your house, it’s not liquid anymore. You can’t easily get it back out if you suddenly need it.

If you can get a low interest rate on your mortgage, you might be better off investing extra cash elsewhere where it could earn higher returns. This is especially true if your employer offers a 401k match—capturing free money from your employer might be smarter than putting extra money into your house.

And for some buyers, putting less down means being able to buy sooner rather than waiting years to save up a larger down payment. Those years of building equity instead of paying rent can be valuable.

Other Costs

Let’s talk about something crucial that often gets overlooked in down payment discussions: the down payment isn’t your only upfront cost.

You’ll also need to cover closing costs, which typically run 2-5% of the loan amount. These include things like appraisal fees, title insurance, origination fees, and various other charges. On a $250,000 loan, that could be $5,000 to $12,500 right there.

Many buyers also need to put down earnest money when their offer is accepted, typically 1-2% of the purchase price. This eventually gets applied to your down payment or closing costs, but you need it available upfront.

Then there are moving expenses, initial home repairs or improvements, and the reality that you’ll probably want to buy some things for your new place. You might need to budget for new appliances, window treatments, or basic maintenance tools if you don’t already own them.

A good rule of thumb is to budget at least 25-30% beyond your down payment amount for these other costs. If you’re planning a 5% down payment on a $300,000 home, that’s $15,000 for the down payment, but you should probably have at least $20,000-$25,000 total in your house fund.

Some of these costs can be negotiated or rolled into your loan, and some assistance programs help with closing costs too, but it’s better to be prepared.

Don’t Wait Too Long

Here’s an uncomfortable truth that might change how you think about saving up a bigger down payment: waiting too long could actually cost you more money in the long run.

While you’re diligently saving up for that bigger down payment, several things are happening. Home prices are generally increasing. Rent is money that disappears forever instead of building equity. And you’re missing out on years of appreciation on the home you could have owned.

Let’s imagine you’re currently paying $1,500 a month in rent. Over three years, that’s $54,000 that simply vanishes. If you had bought a home with a smaller down payment, even with PMI factored in, much of that money would have gone toward building equity instead.

And if home prices increase even 3% annually during those three years, the home you were looking at buying for $250,000 is now $273,000. You need a bigger down payment for the same house, and you’ve paid rent all along.

This doesn’t mean you should rush into buying before you’re ready. But it does mean you shouldn’t unnecessarily delay because you’re holding out for some magical down payment number that might not even be required.

Start Saving For Your Down Payment

Alright, let’s get practical. You understand the myths now, and you know you probably need less than you thought. But you still need to save up something. How do you actually do that?

Start by setting a realistic target based on the home prices in your area and the type of loan you’ll likely qualify for. If you’re a first-time buyer looking at $280,000 homes, and you’ll probably use an FHA loan, your target is 3.5% plus closing costs. That’s roughly $10,000 for the down payment and another $8,000-ish for closing costs. Let’s call it $18,000 total.

Now work backward. If you want to buy in two years, you need to save $750 a month. If that seems impossible, maybe you’re looking at a three-year timeline at $500 a month. Be honest with yourself about what’s achievable.

Set up a separate savings account specifically for your house fund. Make it automatic—schedule transfers from your checking account right after you get paid, before you can spend the money on other things.

Look for ways to boost your savings rate. Can you pick up a side gig? Sell stuff you don’t use? Cut back on subscription services or eating out? Every extra $100 a month you can redirect to your house fund shaves weeks or months off your timeline.

Don’t forget about windfalls. Tax refunds, work bonuses, cash gifts for birthdays or holidays—throw them into the house fund instead of spending them.

And explore whether your employer offers any homebuyer assistance programs. Some companies provide grants or forgivable loans to employees buying homes, especially in expensive markets where recruiting is challenging.

Gifts and Family Help

For many first-time buyers, help from family makes homeownership possible sooner than it would be otherwise.

Lenders generally allow you to use gift money for all or part of your down payment, but there are rules. The gift needs to be documented properly with a gift letter stating that the money doesn’t need to be repaid. The donor might need to show where the money came from to prove it’s not an undocumented loan.

Different loan types have different rules about gifts. FHA loans are pretty lenient about gift funds. Conventional loans might require you to contribute at least some of your own money. VA and USDA loans are generally fine with gifted down payments.

If family help is going to be part of your plan, have honest conversations early. Make sure everyone understands the documentation requirements and the timeline. The gift usually needs to be in your account for at least 30-60 days before closing, or you’ll need extra documentation.

And remember, family help doesn’t have to mean your entire down payment. Even a few thousand dollars can make a meaningful difference in your timeline or the type of home you can afford.

Making Your Down Payment Work For You

At the end of the day, your down payment strategy should align with your overall financial picture and homeownership goals.

If you have excellent credit and stable income but limited savings, a low-down-payment loan might be perfect. The slightly higher monthly payment from PMI might be totally manageable for you, and buying sooner means building equity sooner.

If you have some money saved but want to keep a cushion for emergencies or home improvements, maybe a 5-10% down payment makes sense even if you could afford more. Financial flexibility has real value.

If you’re a veteran, use those VA loan benefits. There’s literally no reason to put money down if you don’t have to.

If you’re in a slower market where homes sit for a while, you might have room to negotiate, and a smaller down payment might be fine. In a competitive market, a larger down payment might make your offer stronger, but weigh that against assistance programs you might qualify for.

Talk to a loan officer early in your process, even before you’re actively house hunting. They can help you understand which loan programs you qualify for, what down payment you’ll actually need, and what your buying power looks like. This conversation doesn’t commit you to anything—it just gives you information to make better decisions.

Moving Forward

So where does all this leave you? Hopefully feeling more empowered and less overwhelmed.

Here’s your practical next steps:

First, check your credit score and credit reports. You can get free reports annually from each bureau. If your score needs work, start addressing it now. Pay down high balances, dispute any errors, and stop opening new credit accounts.

Second, figure out what you can realistically save each month and set up that automatic transfer to a dedicated house fund.

Third, research what’s happening in your local housing market. What do homes actually cost in neighborhoods you’d consider? Are prices rising fast or relatively stable?

Fourth, explore down payment assistance programs in your area. Your state housing finance agency is a great starting point. Many have searchable databases of programs you might qualify for.

Fifth, connect with a mortgage loan officer to understand your options. Come prepared with questions about loan types, down payment requirements, and assistance programs. A good loan officer will educate you, not pressure you.

Sixth, once you understand your financial picture and loan options, connect with a buyer’s agent who works with first-time buyers regularly. They’ll understand the programs available and can guide you through the process.

The Core Truth

Let’s bring this all home with the core truth: you probably don’t need as much as you think you do, and there’s more help available than you realize.

The 20% down payment myth needs to die. It’s keeping too many qualified, ready buyers on the sidelines unnecessarily. The median down payment for first-time buyers has been under 10% for years. You don’t need to be an outlier putting down massive amounts of money.

There are legitimate loan programs from reputable lenders that allow 3-3.5% down, and even zero down for qualified buyers. These aren’t sketchy subprime loans—they’re established programs from major institutions.

Thousands of assistance programs exist specifically to help buyers like you. They’re not just for extremely low-income buyers. Middle-class families regularly qualify and benefit.

Yes, you’ll need to save up something in most cases. Yes, you need to be financially ready for homeownership beyond just the down payment. And yes, there are trade-offs to consider with different down payment amounts.

But the barrier is lower than you thought. The timeline is shorter than you feared. And the help available is more substantial than you imagined.

If you’ve been putting off homeownership because the down payment felt like an insurmountable mountain, it’s time to take a fresh look at your options. You might discover that the dream is more attainable than you ever realized.

The question isn’t whether you can eventually save up some arbitrary percentage. The question is: if the down payment wasn’t actually the obstacle you thought it was, what’s really holding you back from starting your homeownership journey today?