If you’ve been watching the housing market over the past few years, you know it’s been a wild ride. Maybe you’re thinking about buying your first home, or perhaps you’ve been waiting to sell because the timing just hasn’t felt right. Whatever your situation, you’re probably wondering the same thing everyone else is: what’s actually going to happen with real estate this year?

Here’s the good news—things are finally starting to shift in a positive direction. After years of watching affordability slip further and further out of reach, we’re seeing some welcome changes that could make 2026 the year you’ve been waiting for. Let’s break down what’s happening and what it means for you, whether you’re looking to buy, sell, or you’re just keeping an eye on the market.

The Problem We’ve All Been Dealing With

Let’s be honest for a second. The housing market has been frustrating for just about everyone lately. Buyers have been struggling with high costs and limited options. Sellers have felt trapped by the low mortgage rates they locked in during the pandemic, afraid to give them up even when they needed to move. And renters? They’ve been caught in the middle, watching rent prices climb while homeownership seemed increasingly out of reach.

The main culprit behind all this frustration has been affordability—or really, the lack of it. When you combine elevated home prices with higher mortgage rates, monthly payments have eaten up a much bigger chunk of people’s paychecks than they used to. We’re talking about typical mortgage payments now representing over 30% of median household income, compared to around 21% back in 2019. That’s a significant jump, and it’s kept a lot of people on the sidelines.

But here’s where things get interesting. After three years of these challenging conditions, we’re finally seeing some movement in the right direction. Multiple factors are coming together to create a more balanced, more accessible market than we’ve seen in quite a while.

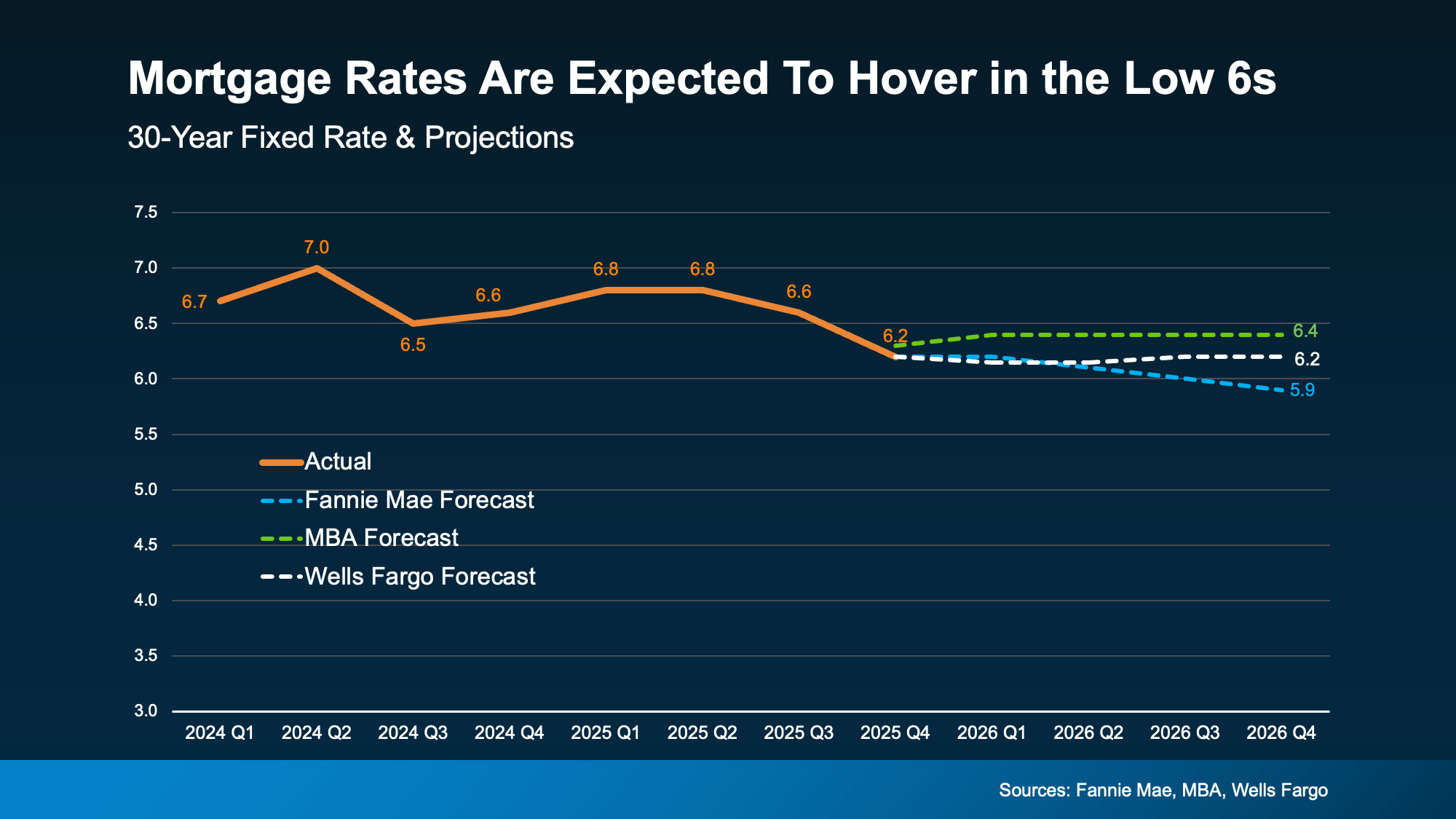

Mortgage Rates Have Come Down

Remember when mortgage rates were flirting with 7% or higher? Those days are behind us, at least for now. Over the past year, rates have dropped by nearly a full percentage point. That might not sound like much when you say it out loud, but the impact on your monthly payment is substantial.

Right now, rates are hovering in the low-to-mid 6% range, and most experts expect them to stay somewhere around there throughout 2026. The forecasts generally point to an average of about 6.3% for a 30-year fixed-rate mortgage. Now, I know what you might be thinking—”6% is still pretty high compared to a few years ago.” And you’re absolutely right. But here’s the thing: those ultra-low rates we saw during the pandemic were exceptional circumstances, not the norm.

What really matters is that rates are already lower than they were a year ago, and that makes a real difference in what you can afford. Even a small decrease in your interest rate can save you hundreds of dollars each month and potentially tens of thousands over the life of your loan.

Of course, where rates go from here depends on several factors outside anyone’s direct control. The overall economy, employment numbers, inflation trends, and decisions made by the Federal Reserve all play a role. If the job market weakens or inflation continues to cool down, we might see rates dip a bit lower. If the opposite happens, they could tick back up. The key point is that we’re in a better place than we were, and that’s already opening doors for more people.

What Lower Rates Mean for You

If you’re a buyer, this rate environment means your purchasing power has improved. You can afford more house for the same monthly payment, or you can keep your payment lower than it would have been with higher rates. Either way, it’s working in your favor.

For sellers, it’s probably time to adjust expectations. Rates in the 6% range might just be the new reality, at least for the foreseeable future. But if you’ve been holding off on selling because you didn’t want to give up your low rate, remember that you’ve likely built up substantial equity in your home. That equity can help you make your move work, even with a higher rate on your next property.

More Houses Are Coming to Market

One of the biggest frustrations of recent years has been the severe shortage of homes for sale. When there aren’t enough houses to go around, buyers end up in bidding wars, prices get pushed higher, and everyone feels the pressure. But we’re starting to see that dynamic shift.

Throughout 2025, the inventory of available homes improved by roughly 15%. That’s a pretty significant increase, and it made a noticeable difference in how the market operated. Buyers suddenly had more options to choose from, more time to make decisions, and more room to negotiate. It was a refreshing change after years of having to move quickly or lose out.

The good news continues into 2026. While experts don’t expect inventory gains to be quite as dramatic as last year, we should still see continued improvement. Current projections suggest the supply of homes for sale will grow by another 8.9% this year. That might not sound as exciting as a 15% jump, but it’s still meaningful progress in the right direction.

Why Inventory Matters

Why does this matter so much? More inventory creates balance. When buyers have options, they don’t feel as pressured to accept less-than-ideal terms or overpay just to secure a home. They can take their time, compare properties, and make more informed decisions. This also means sellers need to be more competitive—pricing your home correctly and presenting it well becomes essential to attracting buyers when they have other choices.

For buyers, this expanding inventory is great news. You’re more likely to find a home that actually meets your needs rather than settling for something that’s just “good enough.” You’ll have more negotiating power, which could mean getting a better price, requesting repairs, or securing other concessions that weren’t available in the ultra-competitive market of recent years.

For sellers, the increased competition means you need to approach your sale strategically. Your home needs to stand out, whether that’s through competitive pricing, great presentation, or both. Working with an experienced local agent becomes even more valuable in this environment because they can help you understand what buyers in your specific area are looking for.

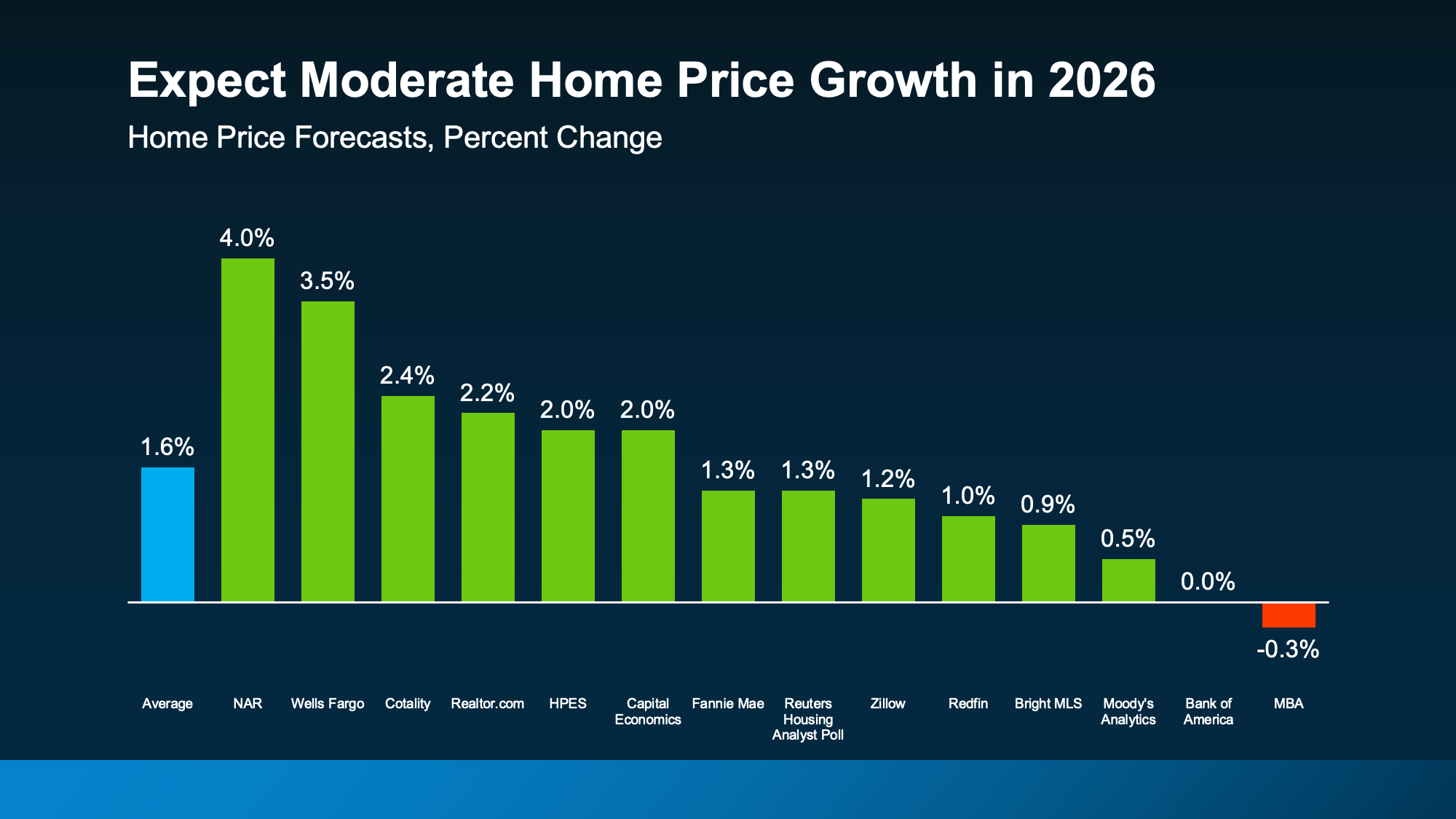

Home Prices Are Slowing Down, Not Crashing

Let’s address the elephant in the room—what about home prices? If you spend any time on social media, you’ve probably seen dramatic predictions about an impending housing crash. Spoiler alert: that’s not what’s happening.

Here’s the reality. With more homes on the market, there’s less upward pressure on prices. We’ve seen this play out over the past year, with price growth slowing considerably compared to the rapid appreciation we experienced a few years ago. The overwhelming consensus among housing experts is that prices will continue to rise nationally, just at a much more moderate pace.

On average, forecasts suggest national home prices will increase by somewhere between 1% and 2.2% in 2026. Some forecasts even predict essentially flat growth, with increases of around half a percent. That’s a far cry from the double-digit annual appreciation we saw during the pandemic era, and that’s actually a healthy thing.

Moderate price growth is sustainable. It allows incomes to gradually catch up, making homes more affordable over time without causing the kind of sharp corrections that can destabilize the market. Think of it as a gentle landing rather than a sudden drop.

Local Markets Tell Different Stories

But here’s something really important to understand: these national figures mask significant regional variation. Some local markets will see stronger price growth, while others might experience slight declines. The housing market isn’t one big monolithic thing—it’s actually thousands of individual local markets, each with its own dynamics, supply and demand factors, and economic conditions.

That’s why working with a knowledgeable local real estate agent is so valuable. They understand the nuances of your specific market and can give you insights that national statistics simply can’t provide. Maybe your area is experiencing job growth that’s driving demand, or perhaps new construction is adding enough supply to ease price pressures. These local factors matter much more than national averages when you’re making a decision about a specific property.

For buyers, this slower price growth environment means more predictability. You’re less likely to face those frustrating situations where homes are selling for tens of thousands over asking price or where you need to waive contingencies just to compete. You can take a more measured approach, do your due diligence, and make offers that make financial sense.

For sellers, the good news is that slower growth doesn’t mean your equity is at risk. Your home’s value is still expected to increase or at least hold steady in most markets. The difference is that you might need to be more patient and realistic about pricing. The days of listing high and getting multiple offers within hours are largely behind us, at least in most markets.

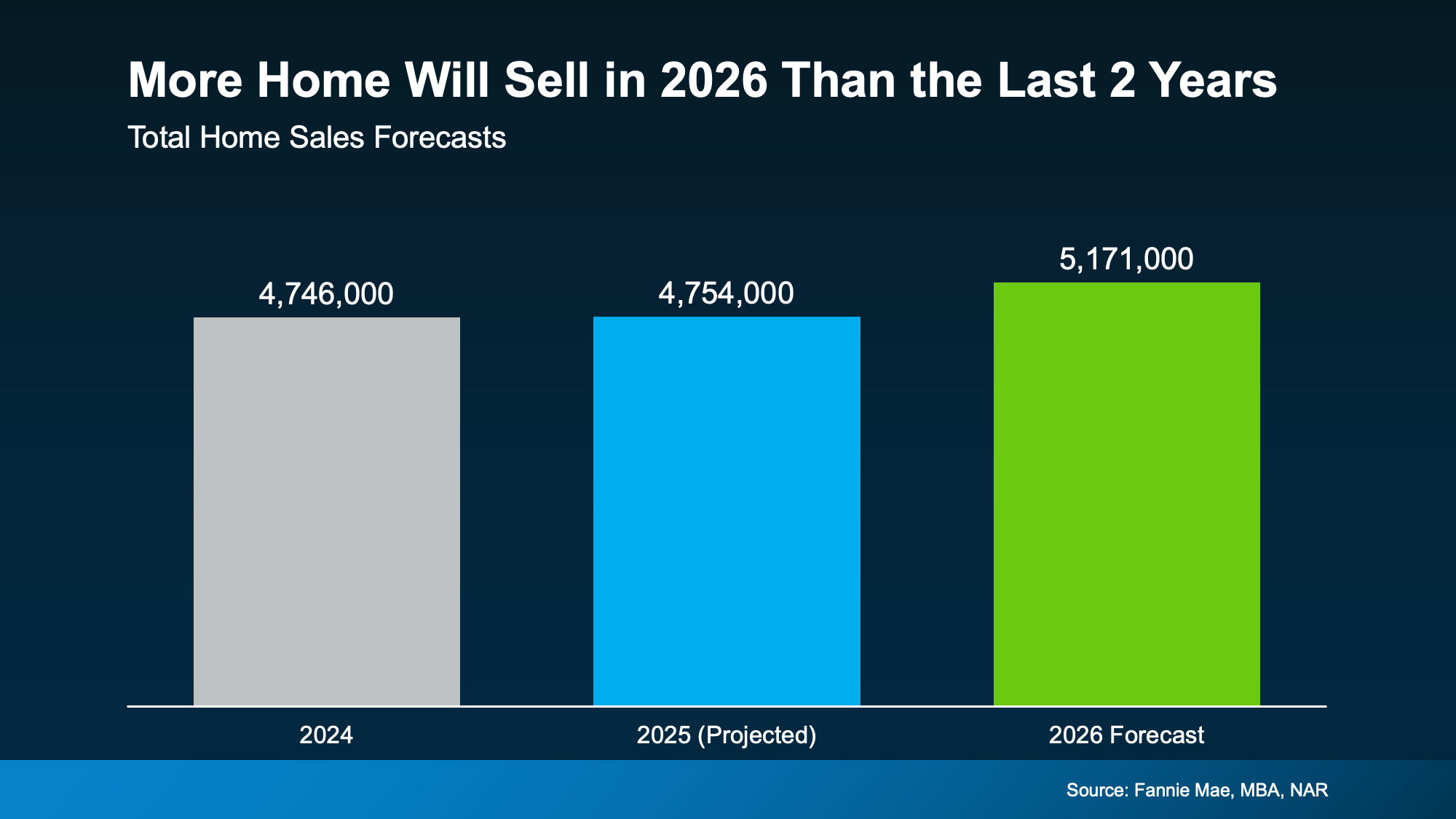

What This Means for Home Sales

When you put all these factors together—lower mortgage rates, more inventory, and moderate price growth—you get an affordability equation that’s finally improving. And that translates into more people being able to buy and sell homes.

After years of sluggish activity, experts are predicting an uptick in home sales for 2026. The estimates vary, but most forecasts suggest a modest increase of around 3% in existing home sales compared to the previous year. That might not sound like a massive jump, but remember that we’re coming off some of the slowest years for home sales in three decades. Any increase is significant progress.

This improved sales environment creates opportunities on both sides of the transaction. More sales mean more options for buyers and more potential purchasers for sellers. It’s a gradual return to a functioning market where people can make moves based on their life circumstances rather than feeling trapped by impossible affordability or market conditions.

A Return to Market Balance

The key word here is “balance.” After years of extreme seller’s market conditions followed by an abrupt shift, we’re moving toward the most balanced market we’ve seen in roughly a decade. In a balanced market, neither buyers nor sellers have an overwhelming advantage. Transactions happen at fair prices, negotiations are reasonable, and people generally feel satisfied with the outcomes.

This is healthy for everyone. Buyers don’t feel like they’re overpaying or being forced into bad decisions. Sellers receive fair value for their homes without unrealistic expectations. And the overall housing market functions more smoothly without the volatility and frustration that have characterized recent years.

The Income and Price Growth Dynamic

There’s another positive trend worth highlighting: for the first time in quite a while, household incomes are expected to rise faster than home prices. This is significant because it’s one of the core drivers of improving affordability.

Most projections suggest wages will increase by somewhere between 3.6% and 4% in 2026, while home prices grow by only 1% to 2.2%. This reverses a trend that’s been in place since before the pandemic, where home prices consistently outpaced income growth, making housing progressively less affordable.

When your income grows faster than home prices, your purchasing power improves even if prices don’t actually decline. You become able to afford more house relative to your earnings. Over time, this dynamic can significantly improve market accessibility, especially for first-time buyers who haven’t benefited from appreciation on a home they already own.

It’s worth noting that this income growth isn’t happening in a vacuum. It reflects broader economic conditions, labor market dynamics, and wage pressures across different industries. If the job market remains strong and employers continue competing for talent, these wage increases could persist or even accelerate.

The Reality Check on Pre-Pandemic Affordability

Now, let’s pump the brakes for a moment and inject some realism into this discussion. While things are improving, we’re not magically returning to the affordability levels of 2019 anytime soon. The math on that is pretty sobering.

To get back to 2019 affordability levels, we would need one of these scenarios: mortgage rates would have to plummet to around 2.65%, or household incomes would need to jump by 56%, or home prices would have to fall by 35%. None of these outcomes are remotely likely in the near term.

The reality is that we’re dealing with a fundamental shift in housing economics. The combination of elevated home prices and higher mortgage rates creates a challenging environment that won’t be fixed quickly or easily. If current trends continue without significant changes, it could take more than two decades to return to pre-pandemic affordability metrics.

This doesn’t mean the situation is hopeless—far from it. It just means we need to adjust our expectations and work with the market as it is, not as we wish it were. The improvements happening in 2026 are real and meaningful, even if they don’t represent a complete reset to previous conditions.

New Construction

The story for newly built homes is a bit different from existing home sales. Homebuilders are facing some unique challenges heading into 2026, particularly with excess inventory of finished homes.

Many builders are currently sitting on more unsold, completed homes than they’ve had in over a decade. This oversupply situation means new construction activity is likely to slow down in the near term, with some forecasts suggesting a 3% decline in single-family home construction.

For buyers interested in new homes, this could actually present opportunities. Builders with excess inventory may be more willing to negotiate on price, offer incentives like rate buydowns, or include upgrades they wouldn’t normally provide. If you’re flexible about location and design, you might find some good deals on newly built homes.

Regional Variations

I keep coming back to this point because it’s so important: national trends only tell you so much. The housing market in South Florida looks very different from the market in rural Indiana or downtown Seattle. Some states, like Florida, Texas, and California, have already seen home prices decline slightly from their peaks. Others are still experiencing solid appreciation.

Your local market conditions depend on factors like job growth, population trends, new construction activity, local regulations, and even weather patterns and natural disaster risks. Before making any major housing decisions, you really need to understand what’s happening in your specific area.

This is where a good real estate agent earns their commission. They can provide insights into neighborhood-level trends, upcoming developments that might affect property values, and the realistic timeline for buying or selling in your market. They know what similar homes have sold for recently, what buyers are currently looking for, and what it takes to make a deal happen.

The Rental Market

For those who are renting, the news is mixed. After a period of explosive rent growth a few years ago, things cooled off considerably in 2025. In fact, rents were essentially flat on a year-over-year basis for the first time in several years.

Unfortunately, that relief might be temporary. With homeownership still out of reach for many people due to high down payment requirements and monthly mortgage costs, rental demand is expected to remain strong. As fewer new apartment buildings are completed in the coming year, basic supply and demand dynamics could push rents back up.

Most forecasts suggest rent increases of around 2% to 3% by the end of 2026. That’s not catastrophic, but it’s still an increase that will eat into household budgets. For renters considering whether to buy, these modest but ongoing rent increases make the case for homeownership stronger, assuming you can manage the upfront costs and monthly payments.

Government Policy

You might be wondering about the new administration’s promised housing reforms. President Trump has indicated plans to pursue what he’s calling “the most aggressive housing reform plans” in U.S. history, but details remain pretty vague at this point.

What we know so far is that the focus will likely be on regulatory reforms—making it easier and faster to get construction projects approved, incentivizing states to reduce barriers to homebuilding, and potentially introducing new mortgage products like 50-year mortgages or portable mortgages that could transfer between properties.

The challenge with any government intervention in housing is that meaningful change takes time. Even if significant reforms are implemented quickly, their effects on housing affordability won’t be immediate. Building more homes—which is ultimately what’s needed to fundamentally improve affordability—is a multi-year process involving land acquisition, zoning approvals, construction, and more.

That said, regulatory streamlining could help over time. If it becomes easier and less expensive to build new homes, developers will build more of them, gradually increasing supply and easing price pressures. It’s not a quick fix, but it’s the kind of structural change that could make a real difference over the long term.

Should You Make Your Move in 2026?

So here’s the million-dollar question: should this be your year to buy or sell?

The truth is, there’s no universal answer that applies to everyone. But what we can say is that the conditions in 2026 are more favorable than they’ve been in several years. Affordability is improving, even if gradually. Market balance is returning, giving both buyers and sellers more breathing room.

If you’ve been putting off a move because the market felt impossible, it might be time to reconsider. Maybe you’ve been waiting for rates to drop—well, they have dropped, and while they might go a bit lower, waiting for them to return to 3% means you could be waiting a very long time. Maybe you’ve been worried about getting into a bidding war—with more inventory available, that’s less of a concern now.

For sellers, consider that rates in the 6% range might be the new normal, and if you’ve been accumulating equity in your current home, that can help offset the impact of a higher rate on your next property. The market is active enough that you have buyers, but not so overheated that you need to price aggressively high.

For first-time buyers, the improvements in affordability might finally make homeownership achievable. Yes, prices are still high by historical standards, but they’re not rising as rapidly, and your income is growing faster than home values for the first time in years. If you’ve been saving for a down payment, your target might finally be within reach.

Moving in the Right Direction

Nobody has a crystal ball, and economic forecasters readily admit they’re often wrong. But the broad consensus heading into 2026 is that the housing market is moving in a positive direction after years of frustration and challenges.

You’ll have more choices as a buyer. You’ll have more realistic expectations as a seller. Monthly costs relative to income are improving, even if slowly. The market is finding balance again.

Is it perfect? No. Are we back to 2019 affordability levels? Absolutely not. But is it better than it’s been in a while, with momentum continuing in the right direction? Yes, and that’s worth paying attention to.

If you’re thinking about buying or selling, the best move you can make is connecting with a knowledgeable local real estate agent. They can help you understand the specific opportunities and challenges in your market, navigate the transaction process, and make sure you’re making decisions based on current reality rather than outdated assumptions or social media hysteria.

The market is giving you an opportunity you haven’t had in quite some time. Whether you choose to take advantage of it is up to you, but at least now you know what you’re working with. And after years of uncertainty and difficulty, that clarity alone is a welcome change.