Spring is a season of renewal, and as a homeowner, it’s easy to get swept up in the day-to-day of life. But maintaining your home is an important part of protecting the long-term value of your investment.

So, whether you own a house already or you’re planning to become a homeowner this year, here are five essential spring home maintenance tasks you don’t want to overlook. Save this as your helpful resource to come back to year after year.

1. Clean Your Gutters

Winter weather can leave behind debris, like leaves and twigs, clogging your gutters. If water can’t flow freely, it can lead to roof leaks or foundation damage. Hiring a professional to take on the height of this job is probably best, but if you’re an ace on a sturdy ladder, this may be your thing. Either way, keeping them clean and clear is a must.

2. Wash Your Windows and Screens

Spring is the perfect time to let the sunlight in – but dirty windows can dull the view. Remove and wash your window screens, then use a window cleaner or a vinegar-water mix to make your glass sparkle. It’s a simple job that can instantly brighten your home while also keeping dirt and build-up from settling in permanently.

3. Service Your HVAC System

Spring also means it’s time to schedule a tune-up for your heating, ventilation, and air conditioning system. A professional can clean and inspect your system, ensuring it’s ready to keep you cool during the summer months while also fixing any damage that may have occurred over the winter. When the summer weather heats up, you don’t want to be calling for an emergency issue that could have been prevented with regular maintenance.

4. Rake and Clear Debris from Your Yard

After a long winter, your yard likely needs a little TLC. Rake up leaves, sticks, and other debris to give your lawn room to flourish. Not only does this make your yard look tidy, but it also helps promote healthy grass growth for the warmer months ahead.

5. Refresh Your Exterior Paint and Caulking

This season is a great time to touch up your home’s exterior paint and check the caulking around windows and doors. This helps prevent water damage and keeps your home looking fresh and inviting.

Bottom Line

Owning a home is a rewarding journey, but it comes with responsibilities. By staying on top of these spring maintenance tasks, you can protect your investment and enjoy your home to the fullest. A little effort now goes a long way when it comes to keeping your home safe, efficient, and beautiful for years to come.

Don’t let these essential tasks sit on the back burner. Your future self will thank you.

What’s on your to-do list this season? I’ll make sure you hit all the homeowner must-do’s and connect you to some local pros I trust who can help get the jobs done.

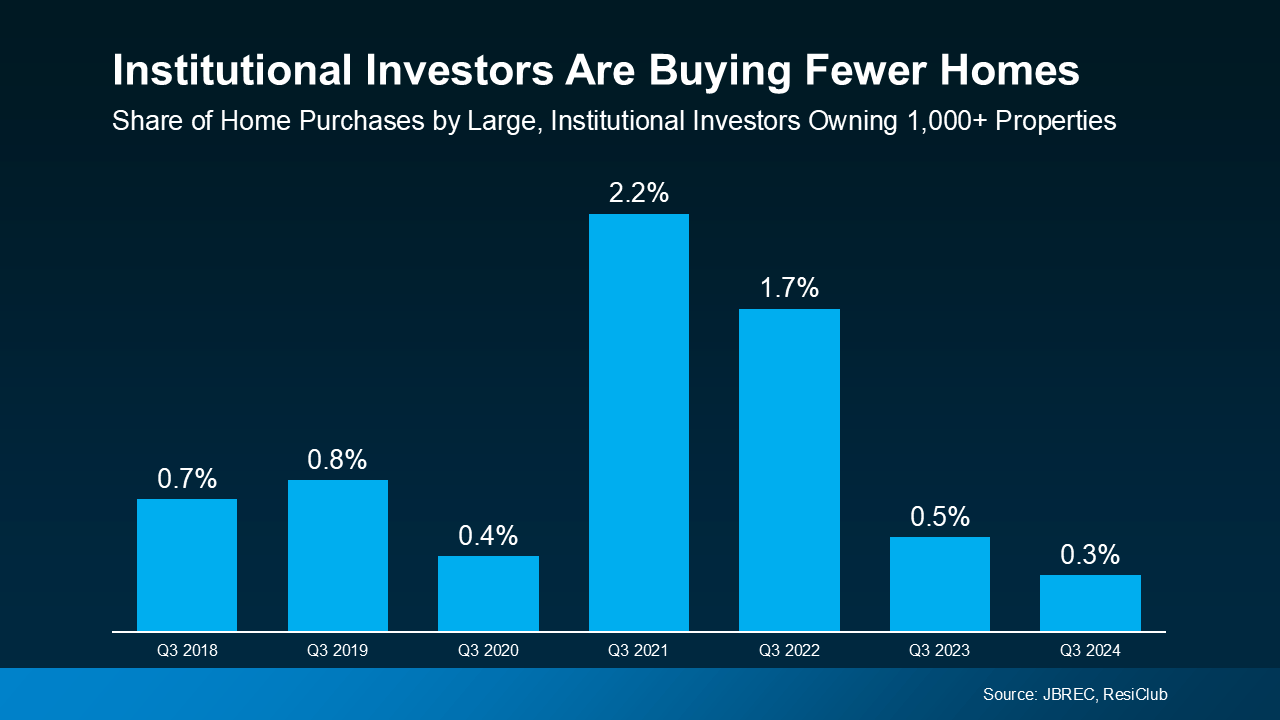

That’s a major shift, and it means far fewer investors are competing in the market now than just a few years ago.

That’s a major shift, and it means far fewer investors are competing in the market now than just a few years ago.