Buying your first home in today’s market can feel tough. Between high home prices and mortgage rates, affordability is still a big challenge. And some buyers are making one simple trade-off that’s getting them in the door faster: square footage.

According to the National Association of Home Builders (NAHB), 35% of buyers are willing to purchase something smaller to make homeownership happen. And one place you can usually find a smaller footprint (and sometimes better affordability) is in townhomes.

Why Townhomes Are Gaining Popularity

Townhomes typically cost less than single-family homes due to their more limited size. And that’s a big plus for today’s budget-conscious buyer. As Realtor.com says:

“In today’s market, affordability remains a key priority for homebuyers, making townhomes an attractive option because they are often priced more reasonably than single-family homes. It makes them especially appealing to first-time homebuyers on a tighter budget . . .”

So, if you’re trying to buy but feeling stuck because of rising prices, shifting your focus to townhomes could be one way to get into homeownership without maxing out your budget.

Builders Are Responding to the Demand

Builders have seen buyers’ appetite shift to smaller homes, and they’re adjusting to meet the demand. As Joel Berner, Senior Economist at Realtor.com, explains:

“Builders are making a concerted effort to provide smaller, more affordable inventory to the market in a way that the existing-home market cannot. Townhomes are a significant portion of that effort.”

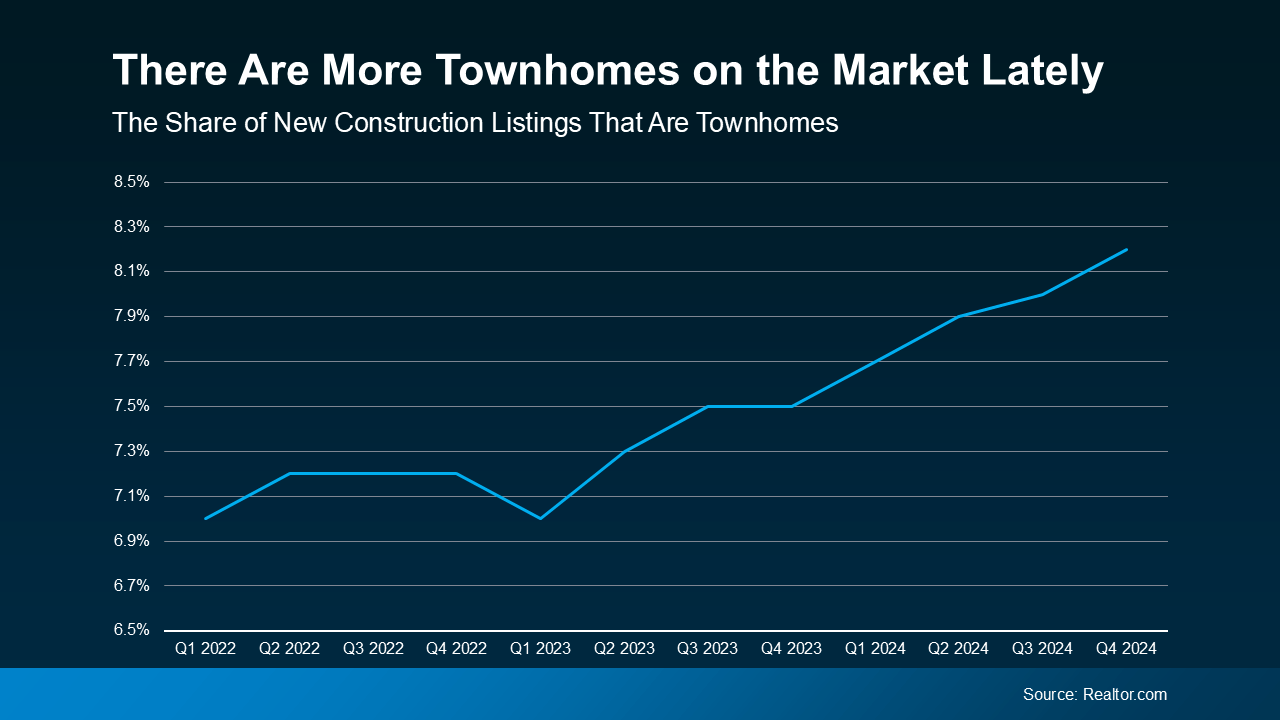

And the numbers back it up. According to data from Realtor.com, townhomes now make up a bigger share of new construction listings than they did just a couple of years ago (see graph below):

That means, if you’re interested in this type of house, you have more choices than you would have had over the last few years. And more options that are potentially more affordable are definitely a good thing. It should make your search for your first home a bit easier.

That means, if you’re interested in this type of house, you have more choices than you would have had over the last few years. And more options that are potentially more affordable are definitely a good thing. It should make your search for your first home a bit easier.

Is a Townhome Right for You?

If you’ve been focused only on more traditional homes with their own yards, an agent can help you explore whether a townhome could work for you. Who knows, you may find out you love the lifestyle. A lot of people do. As an article from the National Association of Realtors (NAR) explains:

“Townhomes tend to cost less than single-family detached homes and can be appealing to young professionals who may desire medium-density, walkable neighborhoods.”

That’s because they’re lower maintenance, they can provide a sense of community with other residents, and they have their own unique amenities. Not to mention, they give you the chance to start building wealth through homeownership without the upkeep that comes with having your own detached, single-family home. And that can be great for first-time buyers who are a bit worried about the maintenance anyway.

But they also come with some other considerations, like dealing with noise through shared walls. If you’re a renter right now, maybe you’re used to that already. But these are the types of things you’ll want to think about. And that’s where an agent’s expertise comes in. They’ll help you weigh the pros and cons, so you understand how a townhome fits into your lifestyle and long-term goals before making your decision.

Bottom Line

If you’re struggling to find a home within your budget, it may be time to expand your search and consider options you haven’t before, like townhomes. Sometimes, compromising a little bit on space is worth it to get your foot in the door.

What matters most to you — space, location, or budget? Connect with an agent to figure out where you can flex to make homeownership happen.

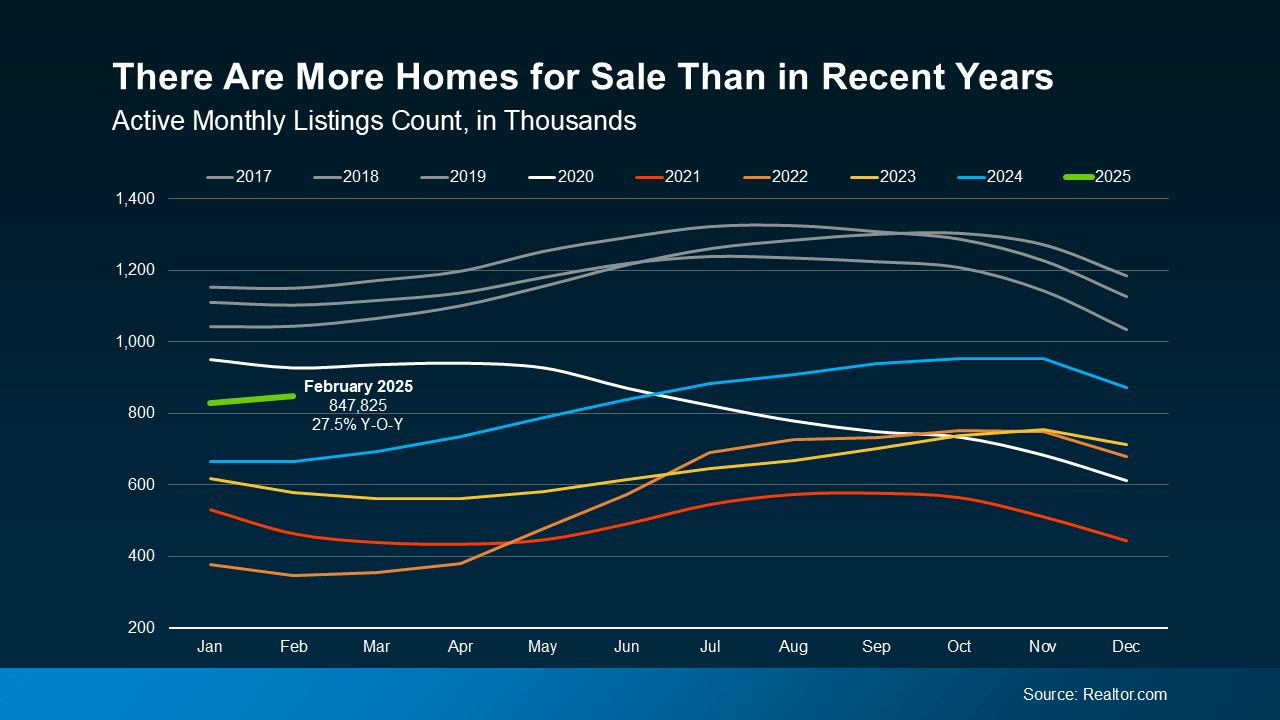

Buyers: This means you have more choices, and you can be more selective.

Buyers: This means you have more choices, and you can be more selective. Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.

Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.