If you’re thinking about buying a home this year, be sure to consider the long-term financial advantages of homeownership, like home equity.

On average, people who bought homes 32 years ago have seen their home’s value nearly triple over that time.

If you’re wondering if buying a home is a good idea, remember rising home values could grow your net worth with time. When you’re ready to start your homebuying journey, talk with a local real estate professional.

The increasing effects of natural disasters are leading to new obstacles in residential real estate. As a recent article from CoreLogicexplains:

“As the specter of climate change looms large, the world braces for unprecedented challenges. In the world of real estate, one of those challenges will be the effects of natural catastrophes on property portfolios, homeowners, and communities.”

That may be why, according to Zillow, more and more Americans now consider how climate risks and natural disasters can impact their homeownership plans (see below):

This study goes on to explain that climate risks affect where many people look for a home. That’s because homebuyers are interested in finding out if the house they want will be exposed to things like floods, extreme heat, and wildfires.

If you’re in the same situation and are thinking about what to do next, here’s some important information to consider as you start looking for a home.

Expert Advice for Homebuyers To Reduce Climate Risks

The first thing to do is understand how to go about buying a home while thinking about climate risks. With the right help and resources, you can simplify the process.

The Mortgage Reports provides these tips for buying your next home:

Evaluate climate risks: Before buying a home, it’s important to check if it’s in a flood-prone area using the FEMA website, review the seller’s property disclosure for any past damage, and get an inspection for issues like cracks and mold to make sure it’s a safe investment.

Consider future preventative maintenance costs: For areas that get tropical storms, you may need to purchase hurricane shutters and sandbags to protect the home. In wildfire-prone areas, you may want to clear plants five feet from the house, consider rooftop sprinklers, or possibly buy gutter guards to prevent fire hazards. Factor these future expenses in when touring homes that may need them.

Take steps to avoid losing your assets: Getting the right insurance for a home in a high-risk climate area is crucial. You should shop around and talk to multiple insurance agents to compare prices and options before deciding to bid on a home.

Above all else, your most valuable resource during this process is a trusted real estate expert. They’ll always focus on your goals while keeping your concerns top of mind. Even if they don’t have all the answers about how your home can handle natural disasters, they can connect you with the right experts and information.

Bottom Line

If you want to buy a home, but you’re also thinking about climate risks, you’re not alone. Your home is a big investment, and if anything can impact that, you want to know. Connect with a real estate professional so you have someone you can trust to guide you as you find your next home.

Are you considering buying your first home? If so, it can be helpful to know what led other people to make that decision. According to a recent survey of first-time homebuyers by PulteGroup:

“When asked why they purchased their first home recently, the answer was simple: because they wanted to. Either the desire to stop renting or recognition that homeownership is a smart financial investment was the main motivator for 72% of respondents.”

While that survey looked specifically at first-time homebuyers buying newly built homes, the same sentiment is true for just about anyone buying their first home. Here’s a bit more information to help you think about those two benefits of homeownership to see if they’re a key factor for you too.

When You Buy a Home, You Have More Stability than When You Rent

You might want to stop renting because rents keep going up. If you’re a renter, that means there’s a chance your payment will increase each time you sign a new rental agreement or renew your current one.

On the other hand, when you buy your home with a fixed-rate mortgage, your monthly housing payment is predictable over the length of that loan. This stability can give you a peace of mind that renting just can’t provide. Jeff Ostrowski, real estate journalist,breaks it down:

“With a fixed-rate mortgage, your monthly principal and interest payment is set for as long as you keep the loan. Sign a rental lease, however, and you could see your rent rise the following year, the year after that and so on.”

When You Buy a Home, You Grow Your Wealth as Home Values Climb

Beyond that, owning a home can also be a great long-term investment. While renting may be the more affordable option right now, it doesn’t provide an avenue for you to grow your wealth over time. Mark Fleming, Chief Economist at First American, explains that’s an important distinction to consider:

“Given current dynamics, more young households may choose to rent in the near term as the cost to own, excluding house price appreciation, has unequivocally increased. Yet, accounting for house price appreciation in that cost of homeownership, whether to rent or buy will depend on where, and if, a home is likely to cost more or less in the near future.”

Basically, renting doesn’t allow you to build equity. In contrast, homeownership can help you grow your net worth as your home’s value appreciates. That’s a significant perk you can’t get if you keep renting.

When you take that into account, it may make better financial sense to buy. Most experts project home prices will continue to appreciate over the next few years at a pace that’s more normal for the market. That means when you buy a home, not only are you investing in a place to live, but you’re also investing in your financial future.

Bottom Line

If you’re ready, it can be a smart move to buy your first home instead of renting. Connect with a real estate professional so you can stabilize your housing payment and start building wealth for your future.

During the fourthquarter of last year, some housing experts projected home prices were going to crash in 2023. The media ran with those forecasts and put out headlines calling for doom and gloom in the housing market. All of this negative news coverage made a lot of people have doubts about the strength of the residential real estate market.

If it made you question if you should delay your own plans to move, here’s what you really need to know.

Home Prices Never Crashed

Disregard what you saw in the headlines. The actual data shows home prices were remarkably resilient and performed far better than the media would have you believe (see graph below):

This graph uses reports from three trusted sources to clearly illustrate prices have already rebounded after experiencing only slight declines nationally. That’s a far cry from the crash so many articles called for.

The declines that did happen (shown in red), weren’t drastic but were short-lived. As Nicole Friedman, a reporter at the Wall Street Journal (WSJ), says:

“Home prices aren’t falling anymore. . . The surprisingly quick recovery suggests that the residential real-estate downturn is turning out to be shorter and shallower than many housing economists expected . . .”

Even though some media coverage made a big deal about home prices pulling back, the slight correction that happened is already in the rearview mirror. Basically, this data shows you home prices aren’t falling anymore – they’re actually going back up.

What’s Next for Home Prices?

The consensus from experts is that home price growth will continue in the years ahead and is returning to normal levels for the market. That means we’ll still see home prices appreciating, just at a slower pace than the last few years – and that’s a good thing.

Some news sources will see home price growth slowing and put out stories that make you think prices are falling again. The return of misleading headlines like those is already having an impact on how homebuyers are feeling again. You can see how this affects general opinion in theConsumer Confidence Surveyfrom Fannie Mae (see graph below):

While the percentage of Americans who think prices will fall has been slowly declining this year, the latest Consumer Confidence data indicates that’s ticked back up recently (shown in red). This change is surprising especially since the home price data shows prices are going up, not down. It tells you the impact the media still has on public opinion.

Don’t fall for the negative headlines and become part of this statistic. Remember, data from a number of sources shows home prices aren’t falling anymore.

Bottom Line

Even though the media may make things sound doom and gloom, the data shows home prices aren’t falling anymore. So, don’t let the headlines scare you or delay your plans. Lean on a real estate professional so you have a trusted resource to cut through the noise and tell you what’s really happening in your area.

If you’re thinking about buying a home soon, higher mortgage rates, rising home prices, and ongoing affordability concerns may make you wonder if it still makes sense to buy a home right now. While those market factors are important, there’s more to consider. You should think about the long-term benefits of homeownership too.

Think about this: if you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. Why is that? The reason is tied to how home values grow with time and how, by extension, that grows your own wealth. That may be why, in a recent Fannie Mae survey, 76% of respondents say they believe buying a home is a safe investment.

Here’s a look at how just the home price appreciation piece can really add up over the years.

Home Price Growth over Time

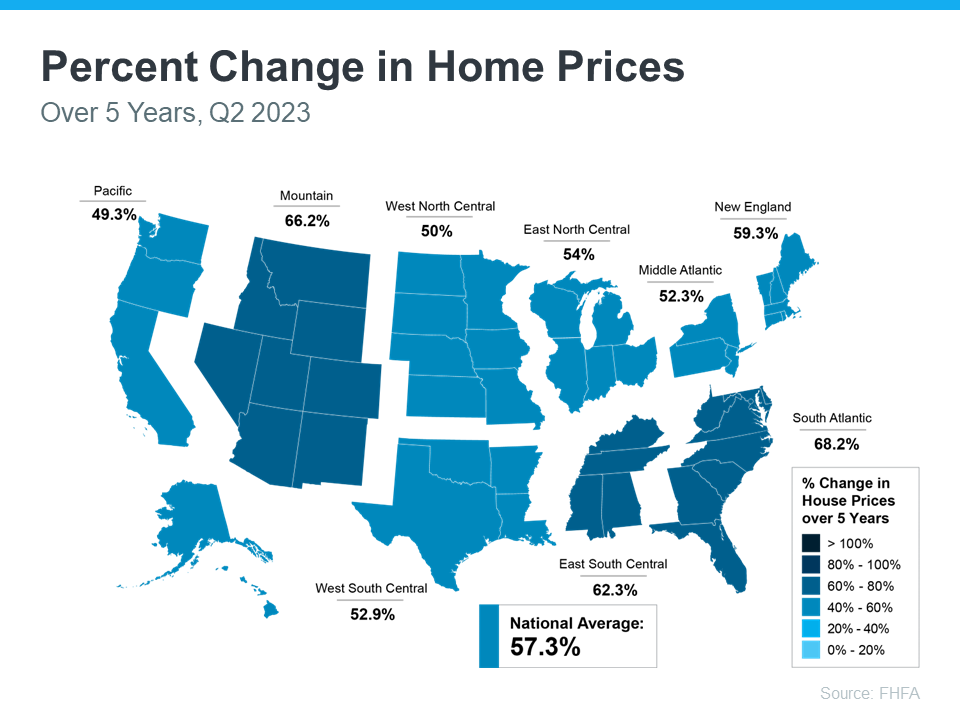

The map below uses data from the Federal Housing Finance Agency (FHFA) to show just how noteworthy price gains have been over the last five years. And, since home prices vary by area, the map is broken out regionally to help convey larger market trends:

If you look at the percent change in home prices, you can see home prices grew on average by just over 57% nationwide over a five-year period.

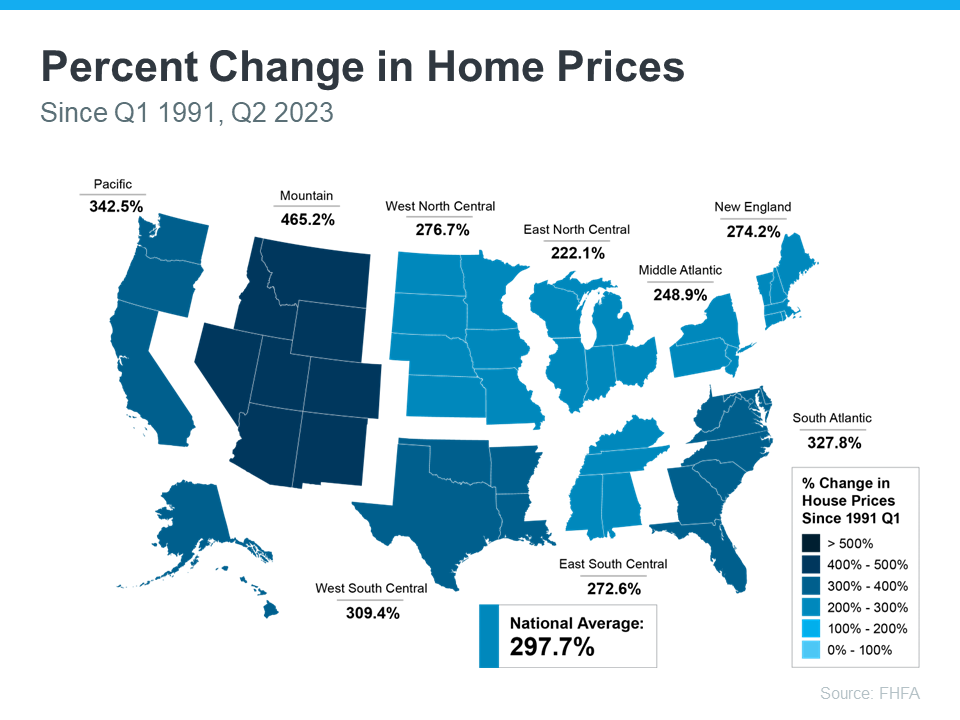

Some regions are slightly above or below that average, but overall, home prices gained solid ground in a short time. And if you expand that time frame even more, the benefit of homeownership and the drastic gains homeowners made over the years become even clearer (see map below):

The second map shows, nationwide, home prices appreciated by an average of over 297% over a roughly 30-year span.

This nationwide average tells you the typical homeowner who bought a house 30 years ago saw their home almost triple in value over that time. That’s a key factor in why so many homeowners who bought their homes years ago are still happy with their decision.

And while you may have heard talk throughout the year that home prices would crash, it hasn’t happened. In fact, experts project home prices will continue to rise for years to come.

Bottom Line

If you’re wondering if it still makes sense to buy a home today, it’s important to focus on the long-term advantages that come with homeownership. When you’re ready to start your homebuying journey, reach out to a local real estate professional.

Wondering why the supply of homes for sale is limited today? There are a few factors at play.

Lack of building over time, the mortgage rate lock-in effect, and people staying in their houses longer are three of the main reasons why supply is low.

But real estate agents know exactly where to look and what to do to make your dream a reality. Connect with an agent so you have an expert on your side to help you successfully navigate the market and find your next home.

If your listing expired and your house didn’t sell, you’re likely feeling a little frustrated. Not to mention, you’re also probably wondering what went wrong. Here are three questions to think about as you figure out what to do next.

Did You Limit Access to Your House?

One of the biggest mistakes you can make when selling your house is restricting the days and times when potential buyers can tour it. Being flexible with your schedule is important when you’re selling your house, even though it might feel a bit stressful to drop everything and leave when buyers want to see it. After all, minimal access means minimal exposure to buyers. ShowingTimeadvises:

“. . . do your best to be as flexible as possible when granting access to your house for showings.”

Sometimes, the most determined buyers might come from far away. Since they’re traveling to see your house, they may not be able to change their plans easily if you only offer limited times for showings. So, try to make your house available as much as you can to accommodate them. It’s simple. If no one’s able to look at it, how’s it going to sell?

Did You Make Your House Stand Out?

When selling your house, the old saying matters: you never get a second chance to make a first impression. Putting in the work to make the exterior of your home look nice is just as important as how you stage it inside. Freshen up your landscaping to improve your home’s curb appeal so you can make an impact upfront. As an article from U.S. Newssays:

“After all, if people drive by, but aren’t interested enough to walk through the front door, you’ll never sell your house.”

But don’t let that impact stop at the front door. By removing personal items and reducing clutter inside, you give buyers more freedom to picture themselves in the home. Additionally, a new coat of paint or cleaning the floors can go a long way to freshening up a room.

Did You Price Your House Compellingly?

Setting the right price is extremely important when you’re selling your house. Even though it might feel tempting to push the price higher to maximize your profit, overpricing can scare away buyers and make it hard to sell quickly. Business Insidernotes:

“. . . the biggest mistake sellers make is overpricing their home.”

If your house is priced higher than others like it, it could make buyers lose interest. Pay attention to the feedback people give your agent during open houses and showings. If lots of people are saying the same thing, it might be a good idea to think about lowering the price.

For all these insights and more, rely on a trusted real estate agent. A great agent will offer expert advice on relisting your house with effective strategies to get it sold.

Bottom Line

It’s natural to feel disappointed when your listing has expired and your house didn’t sell. Talk to a trusted real estate agent to figure out what happened and what to reconsider or change if you want to get your house back on the market.

You might remember the housing crash in 2008, even if you didn’t own a home at the time. If you’re worried there’s going to be a repeat of what happened back then, there’s good news – the housing market now is different from 2008.

One important reason is there aren’t enough homes for sale. That means there’s an undersupply, not an oversupply like the last time. For the market to crash, there would have to be too many houses for sale, but the data doesn’t show that happening.

Housing supply comes from three main sources:

Homeowners deciding to sell their houses

Newly built homes

Distressed properties (foreclosures or short sales)

Here’s a closer look at today’s housing inventory to understand why this isn’t like 2008.

Homeowners Deciding To Sell Their Houses

Although housing supply did grow compared to last year, it’s still low. The current months’ supply is below the norm. The graph below shows this more clearly. If you look at the latest data (shown in green), compared to 2008 (shown in red), there’s only about a third of that available inventory today.

So, what does this mean? There just aren’t enough homes available to make home values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that’s not happening right now.

Newly Built Homes

People are also talking a lot about what’s going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. The graph below shows the number of new houses built over the last 52 years:

The 14 years of underbuilding (shown in red) is a big part of the reason why inventory is so low today. Basically, builders haven’t been building enough homes for years now and that’s created a significant deficit in supply.

While the final blue bar on the graph shows that’s ramping up and is on pace to hit the long-term average again, it won’t suddenly create an oversupply. That’s because there’s too much of a gap to make up. Plus, builders are being intentional about not overbuilding homes like they did during the bubble.

Distressed Properties (Foreclosures and Short Sales)

The last place inventory can come from is distressed properties, including short sales and foreclosures. Back during the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford.

Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from the Federal Reserve to show how things have changed since the housing crash:

This graph illustrates, as lending standards got tighter and buyers were more qualified, the number of foreclosures started to go down. And in 2020 and 2021, the combination of a moratorium on foreclosures and the forbearance program helped prevent a repeat of the wave of foreclosures we saw back around 2008.

The forbearance program was a game changer, giving homeowners options for things like loan deferrals and modifications they didn’t have before. And data on the success of that program shows four out of every five homeowners coming out of forbearance are either paid in full or have worked out a repayment plan to avoid foreclosure. These are a few of the biggest reasons there won’t be a wave of foreclosures coming to the market.

What This Means for You

Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. According to Bankrate, that isn’t going to change anytime soon, especially considering buyer demand is still strong:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equationsimply won’t allow a price crash in the near future.”

Bottom Line

The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing inventory tells us there’s no crash on the horizon.

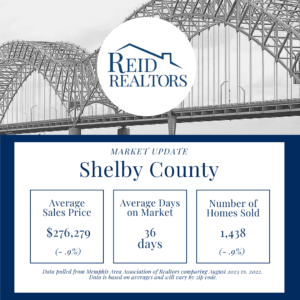

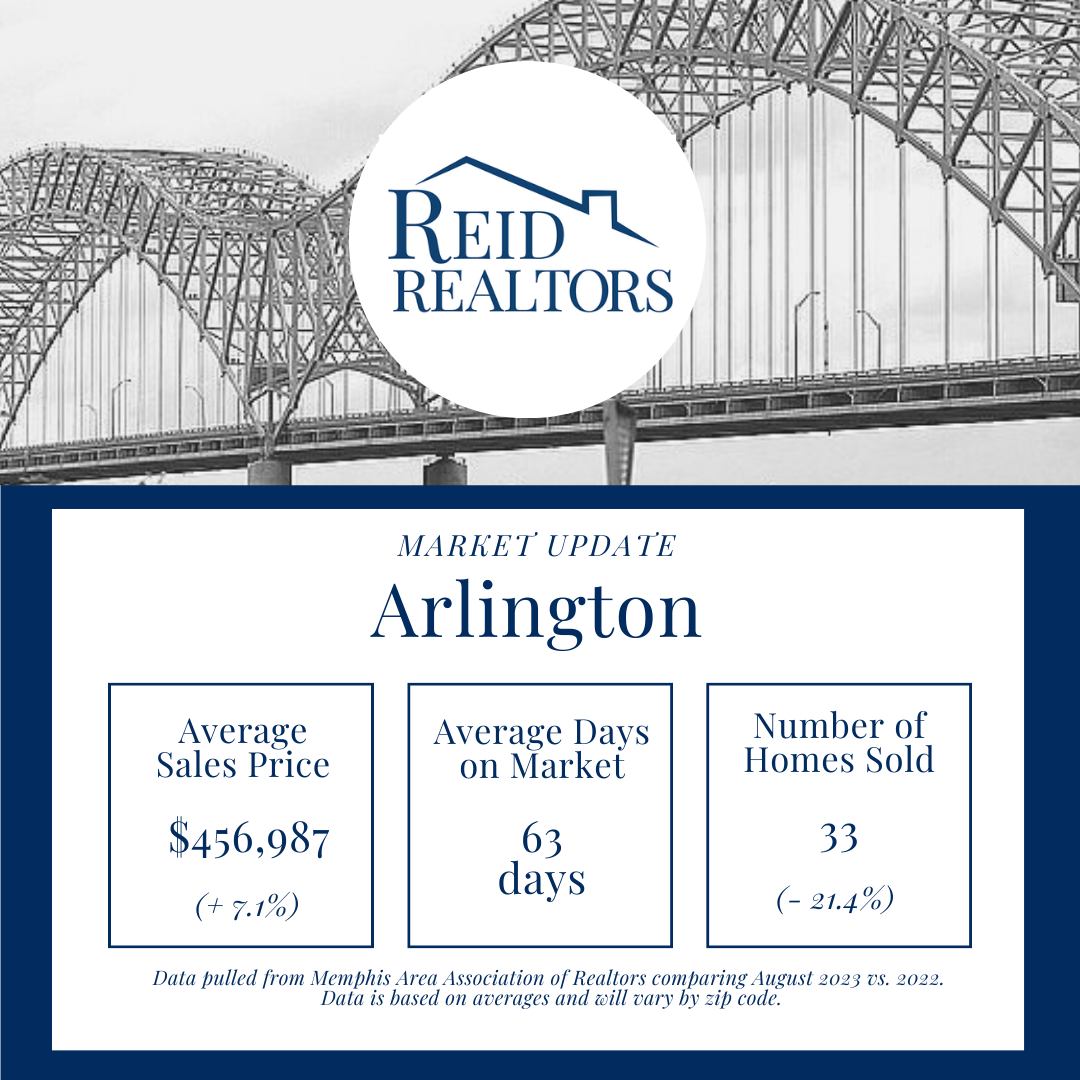

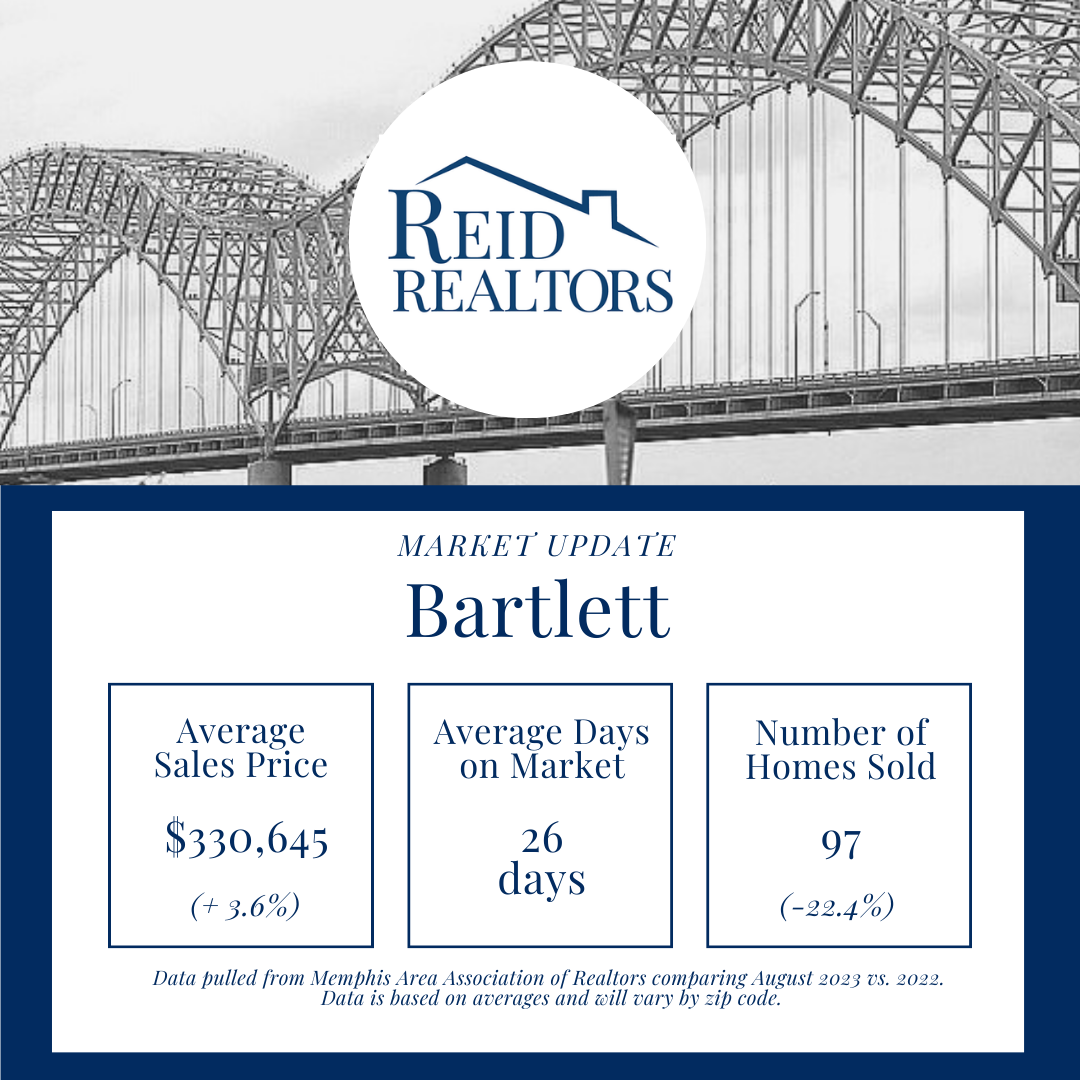

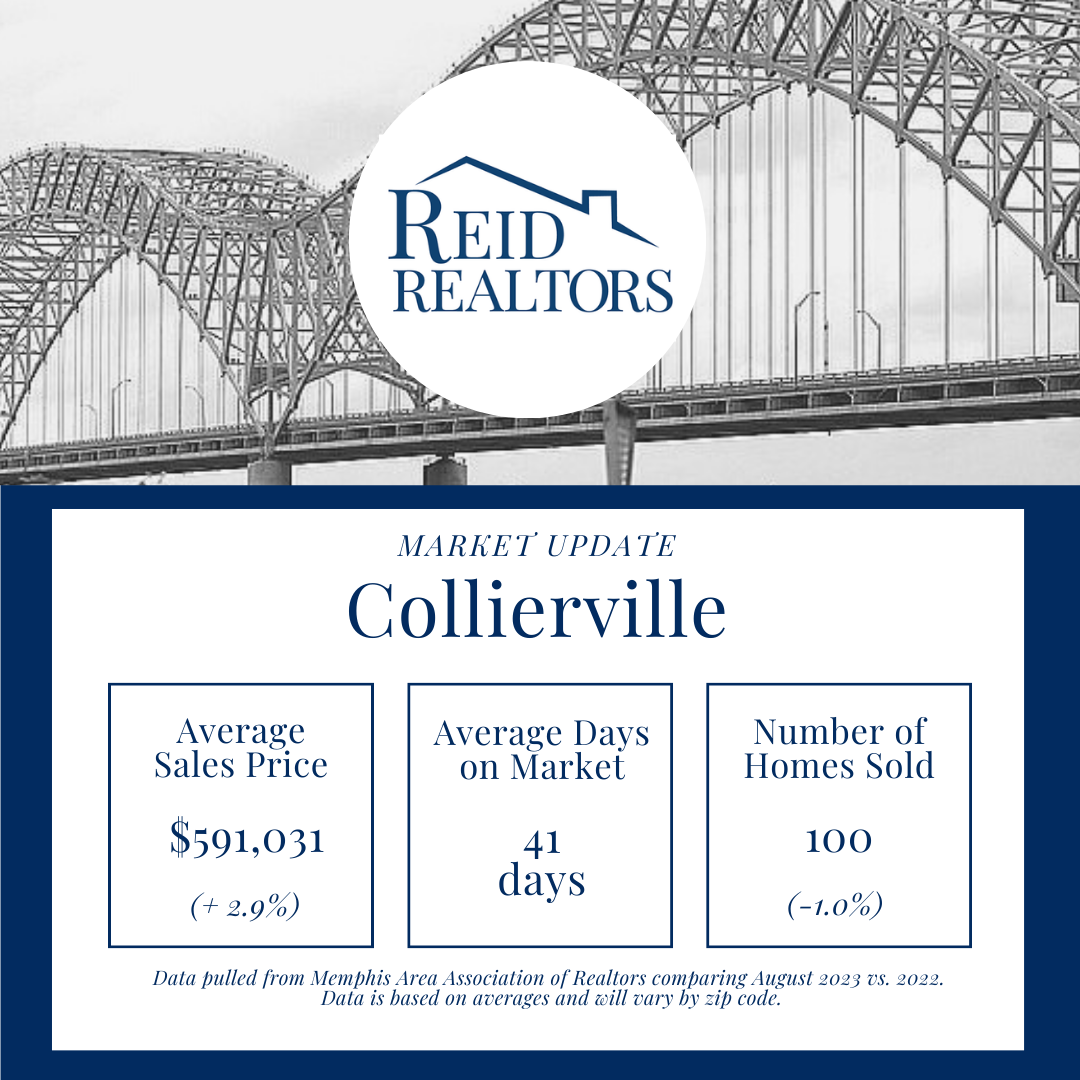

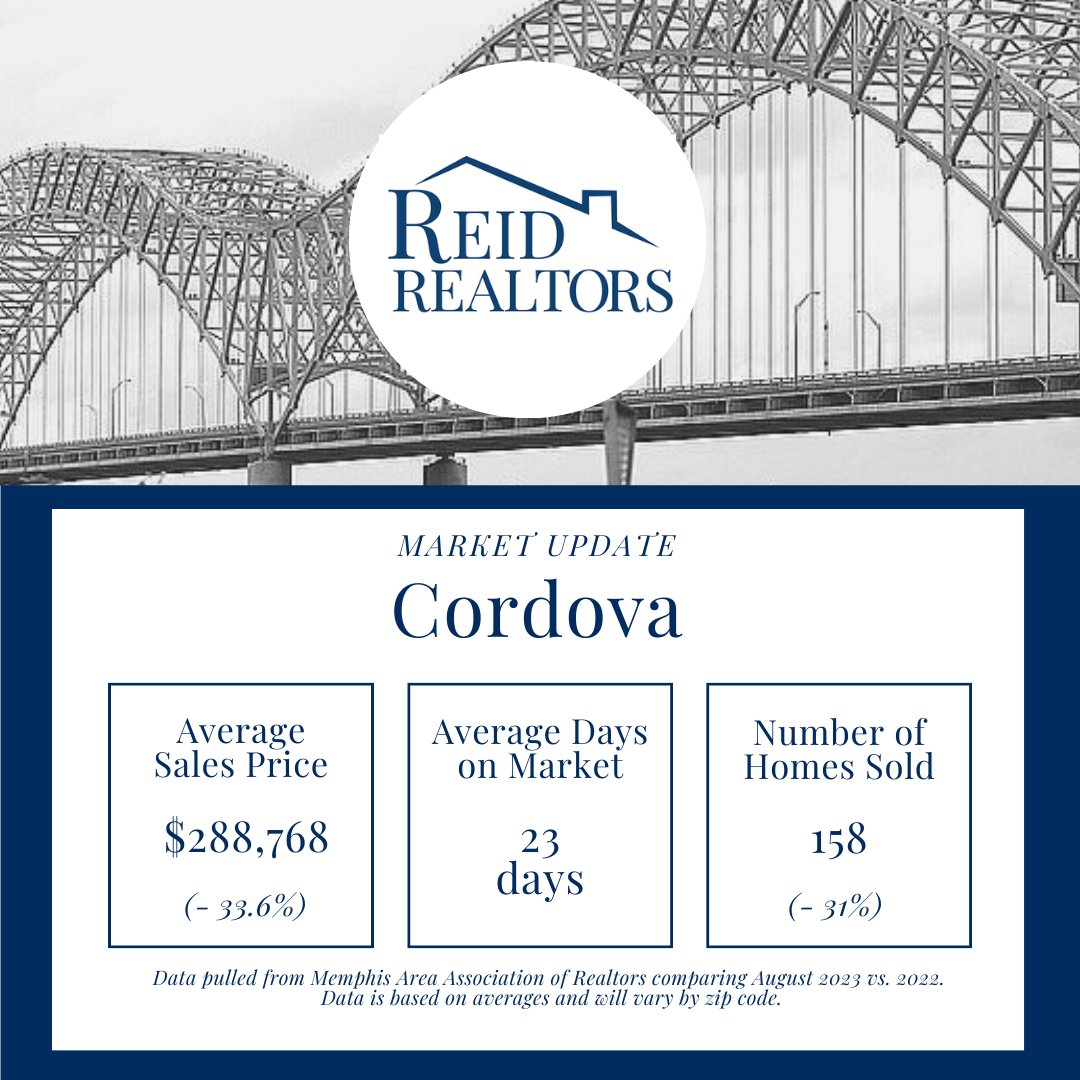

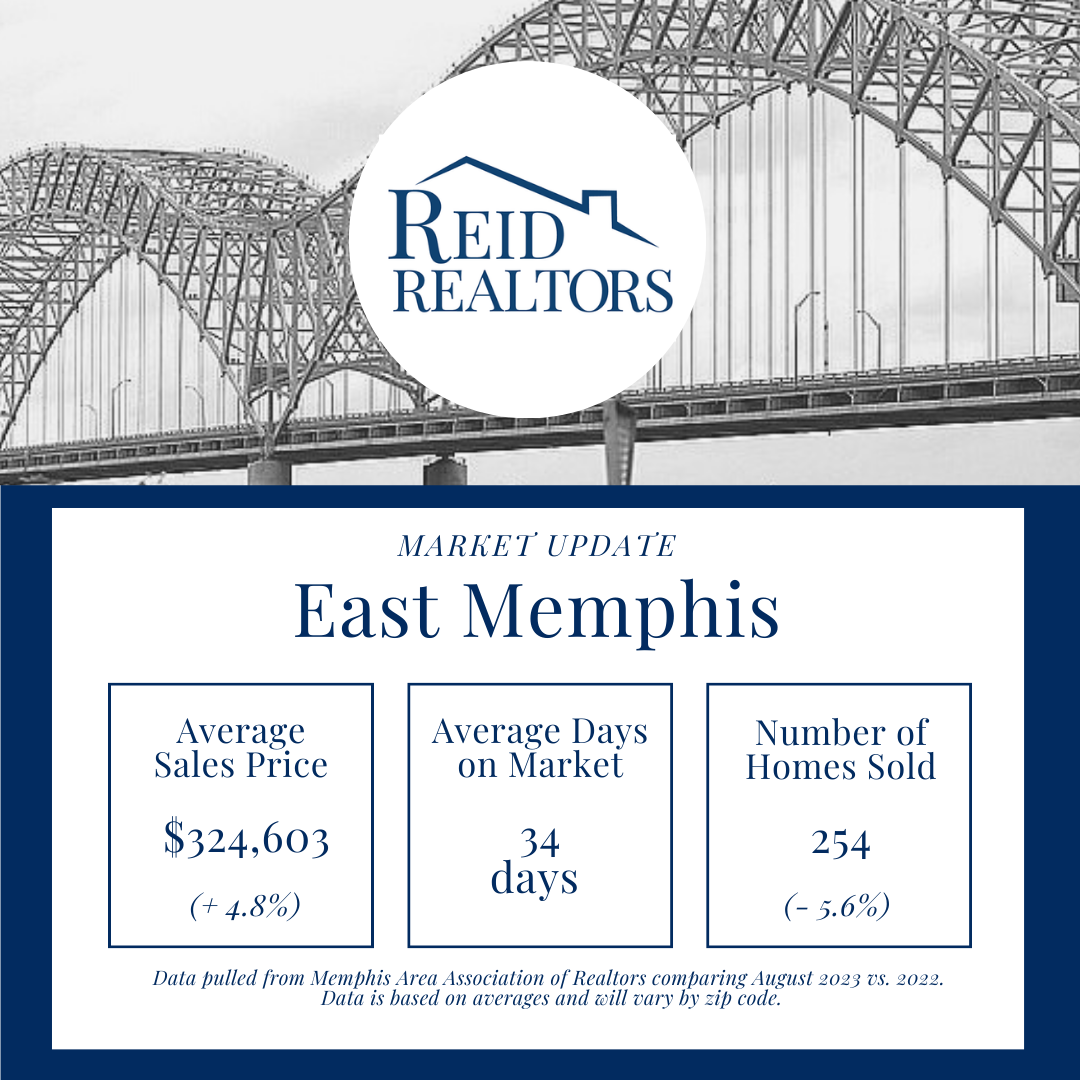

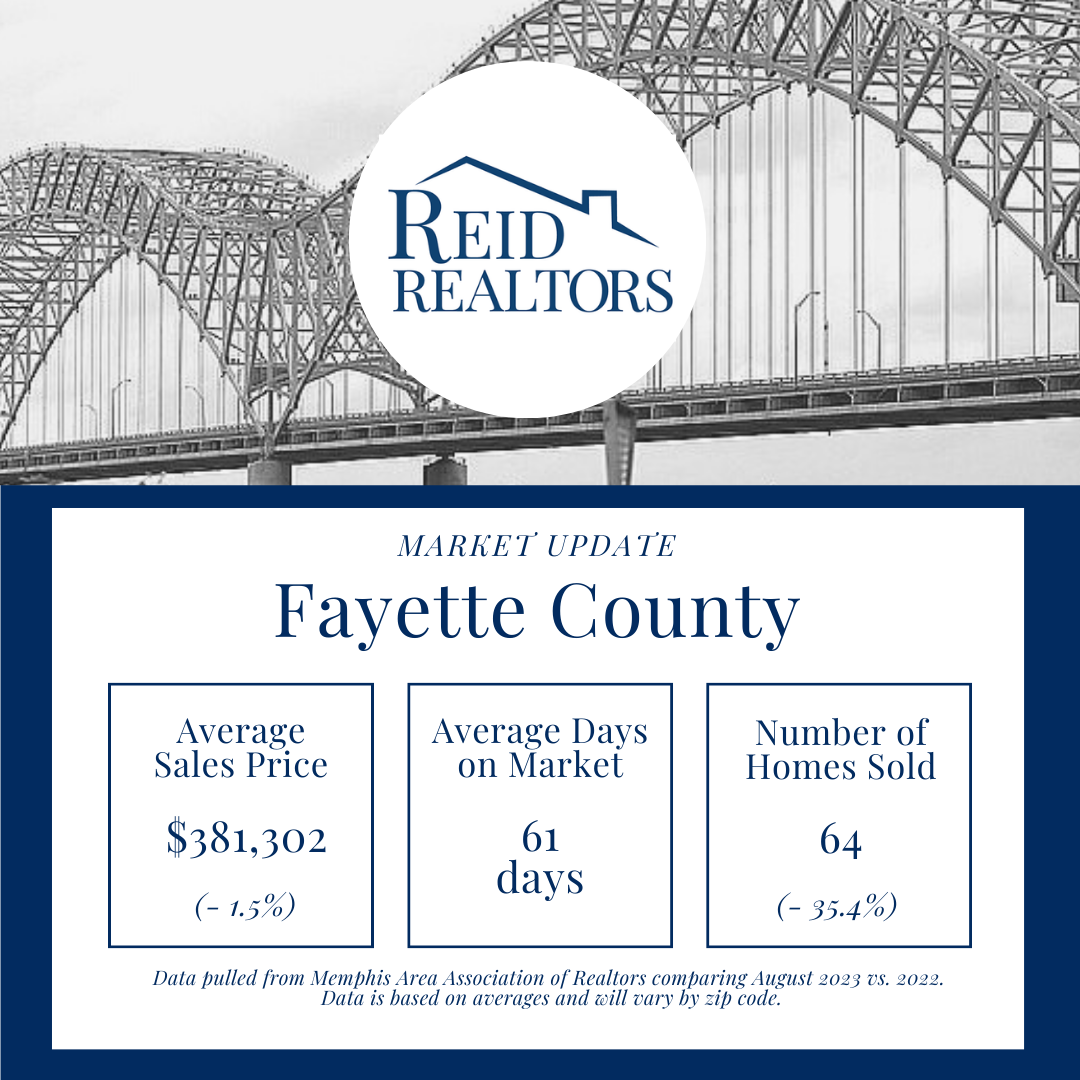

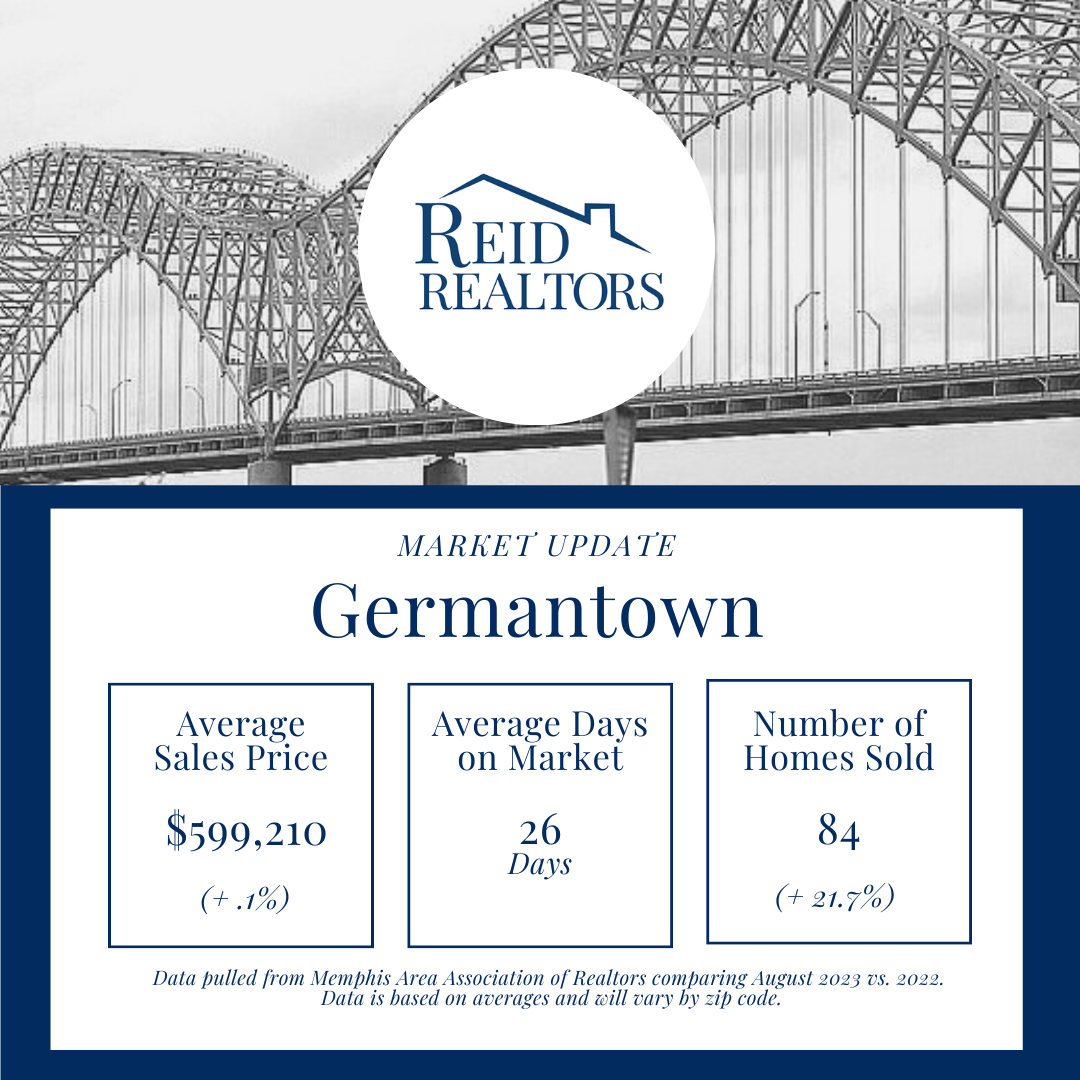

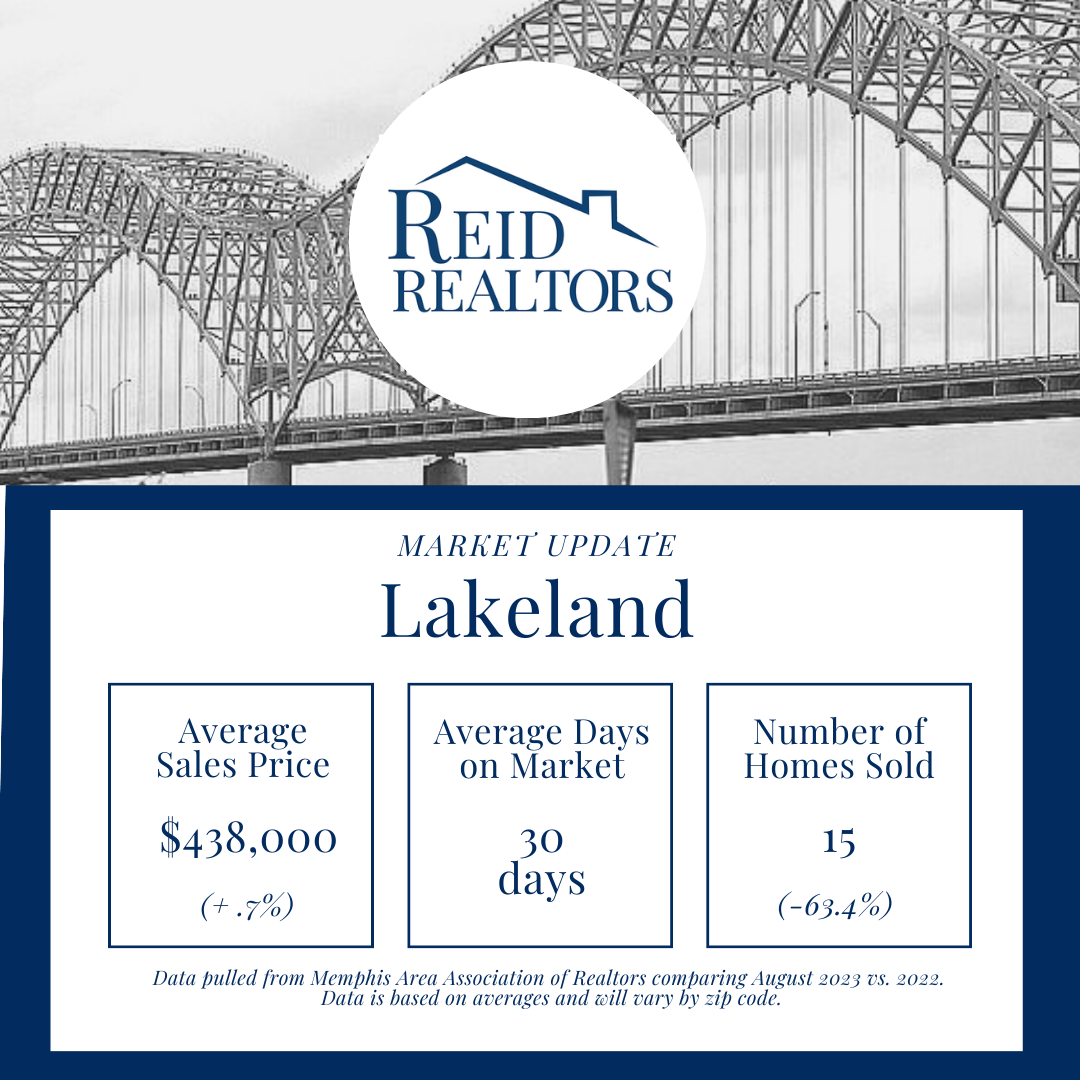

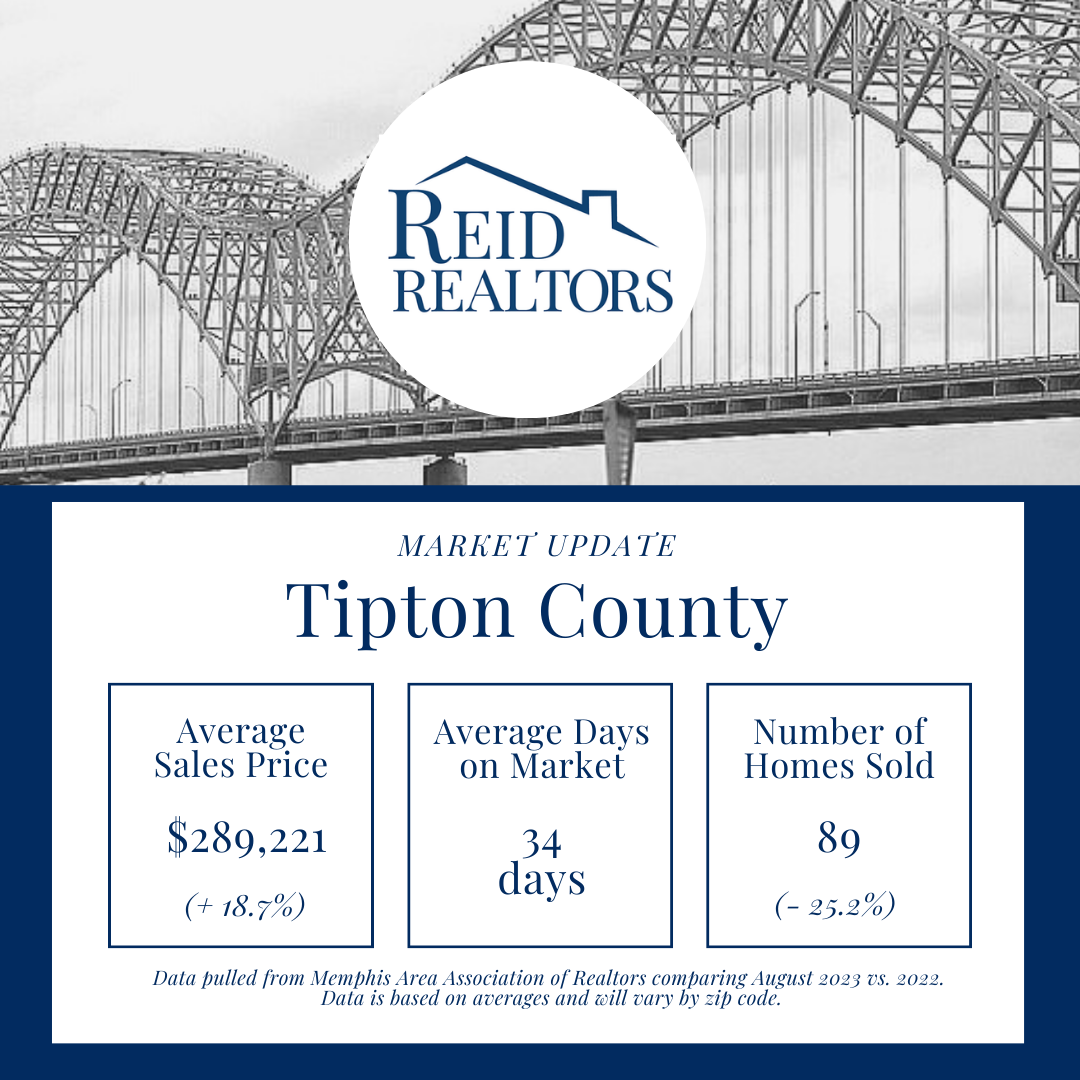

Your Real Estate Market UpdateFrom your Reid Realtors team

It’s that time again. We’re diving into what’s going on with our local market and what you should know.

Many have felt the change in the market from the pandemic years through where we are currently. If you haven’t experienced it yourself, you know someone who has. Interest rates still remain high and we are seeing fewer people move. Days on market are back to pre-pandemic days (homes are sitting longer) and overall we are adjusting our own expectations, continually learning and communicating these expectations and learnings with our clients.

While we understand that market fluctuations may cause some concern, we want to assure you that there is hope for Real Estate in Memphis and in August alone, we’ve seen an uptick compared to previous months.

Here are some key insights on why you should remain optimistic:

Despite minor fluctuations, the Memphis real estate market is still showing strength.

There are plenty of opportunities for both buyers and sellers.

We anticipate a stable market in the near future.

We’ll show you some numbers and discuss further thoughts below.

The Numbers

A preview of Shelby County aggregated from the month of August comparing August 2023 vs. August 2022. For information by suburb, click the link below to see your area specifically.

The above gives an overview of the Shelby County. These numbers vary from each area of the city so please click below to view your area.

Understanding Price Sensitivity

While sales are steady or down year over year for most cities in our area, we are starting to see a wider gap in communities with a lower average sales price. Interest rates are playing a major role in this and are having a negative impact on sales volume in these communities. Cities with a higher average sales price are seeing less of a decrease due to less price sensitivity. Regardless of where you fall, we’re committed to working with our clients in every circumstance and partnering with you to meet your goals. We are proud to serve a wide-range of clients from all walks of life across, multiple cities in the Greater Memphis Area.

Readjusting expectations

Our team strives to be authentic, clear and concise with our communication to our clients. One thing that we are having to readjust for ourselves and our clients (especially sellers) is expectations. Two main things we are striving to communicate in this current market to our sellers is 1) pricing your home correctly and 2) being patient after listing.

Overpricing your home in this market is one of the hardest obstacles to overcome if you price too aggressively on the front end. Our goal is to drive people in your door. Pricing too high is a red flag to many buyers that understand comparables in your area. Also, the longer your home sits, you can expect more price drops and more buyers coming in with low offers.

Patience is also key. There’s a fine line between reacting to what the market is telling you (with price) and dropping prices too quickly. Gone are the days that we expect a home to get under contract in a weekend (although in the right circumstances we are still seeing that too). It’s important to understand you need to be patient as there are less buyers in the market.

But you don’t have to do any of this alone. We’re doing this behind the scenes on a daily basis and are ready to guide you and help you navigate this current market.

Opportunities for First Time Home Buyers

While sellers are adjusting expectations, buyers are too. But in this case, they are leveraging their buying power to take more time before making an offer, ask for repairs and closing costs, and be more selective overall when choosing a home.

This presents a great opportunity for first time home buyers as they can slow down, save and find a home that’s right for them.

With rents just as high as mortgages (if not more), it’s smart to assess your situation to see if you can afford to buy a home. Many banks and mortgage companies offer different loans to accommodate first time home buyers. We’d be happy to connect you with reputable lenders to reach out to.

If you’re thinking of making a move, one of the biggest questions you have right now is probably: what’s happening with home prices? Despite what you may be hearing in the news, nationally, home prices aren’t falling. It’s just that price growth is beginning to normalize. Here’s the context you need to really understand that trend.

In the housing market, there are predictable ebbs and flows that happen each year. It’s called seasonality. Spring is the peak homebuying season when the market is most active. That activity is typically still strong in the summer but begins to wane as the cooler months approach. Home prices follow along with seasonality because prices appreciate most when something is in high demand.

That’s why there’s a reliable long-term home price trend. The graph below uses data from Case-Shiller to show typical monthly home price movement from 1973 through 2022 (not adjusted, so you can see the seasonality):

As the data shows, at the beginning of the year, home prices grow, but not as much as they do in the spring and summer markets. That’s because the market is less active in January and February since fewer people move in the cooler months. As the market transitions into the peak homebuying season in the spring, activity ramps up, and home prices go up a lot more in response. Then, as fall and winter approach, activity eases again. Price growth slows, but still typically appreciates.

After several unusual ‘unicorn’ years, today’s higher mortgage rates helped usher in the first signs of the return of seasonality. As Selma Hepp, Chief Economist at CoreLogic,explains:

“High mortgage rates have slowed additional price surges, with monthly increases returning to regular seasonal averages. In other words, home prices are still growing but are in line with historic seasonal expectations.”

Why This Is So Important to Understand

In the coming months, you’re going to see the media talk more about home prices. In their coverage, you’ll likely see industry terms like these:

Appreciation: when prices increase.

Deceleration of appreciation: when prices continue to appreciate, but at a slower or more moderate pace.

Depreciation: when prices decrease.

Don’t let the terminology confuse you or let any misleading headlines cause any unnecessary fear. The rapid pace of home price growth the market saw in recent years was unsustainable. It had to slow down at some point and that’s what we’re starting to see – deceleration of appreciation, not depreciation.

Remember, it’s normal to see home price growth slow down as the year goes on. And that definitely doesn’t mean home prices are falling. They’re just rising at a more moderate pace.

Bottom Line

While the headlines are generating fear and confusion on what’s happening with home prices, the truth is simple. Home price appreciation is returning to normal seasonality. If you have questions about what’s happening with prices in your local area, connect with a real estate professional.