(Updated 10/24/25)

So you’ve found the perfect house and you’re ready to make your homeownership dreams come true. That’s exciting! But before you start picking out paint colors and measuring for furniture, there’s something important we need to talk about – and no, it’s not just your down payment.

While most future homeowners obsess over saving enough for that down payment (and rightfully so), there’s another significant expense that catches way too many buyers off guard: closing costs. Think of these as the “behind-the-scenes” expenses that make your home purchase official and legal. Let’s dive into everything you need to know about these costs so you can budget smartly and avoid any unwelcome surprises when you’re ready to get those keys.

What Closing Costs Really Mean

Here’s the thing about closing costs – they’re not some mysterious concept designed to confuse you. They’re simply all the various fees and expenses that pile up during the final stages of your home purchase. These are the charges that make your transaction official, ensure the property is legally yours, and protect everyone involved in the deal.

Picture closing day like the finale of a big production. You’ve got the real estate agents, lenders, attorneys, inspectors, insurance companies, and government offices all playing their parts. Each one provides a service that makes your home purchase possible, and each one needs to be compensated. That’s essentially what closing costs cover.

What makes these expenses a bit tricky is that they’re not a single, straightforward charge. Instead, they’re a collection of different fees bundled together. Some are paid directly to your lender, others go to third-party service providers, and some cover government requirements. The total amount you’ll pay depends on various factors, including where you’re buying, the purchase price of your home, and how you’re financing the purchase.

What Goes Into Closing Costs

Let’s get specific about what you’re actually paying for when those closing costs hit your bank account. Understanding each component can help you see where your money is going and why these expenses exist in the first place.

Fees Related to Your Mortgage Application

When you apply for a home loan, your lender has work to do. They need to process your application, which means someone has to review all your financial documents, verify your income, check your employment history, and assess whether you’re a good candidate for the loan amount you’re requesting.

The application fee covers this initial processing work. Not every lender charges this fee, but when they do, it’s typically due when you submit your application and usually isn’t refundable if your loan doesn’t get approved.

Then there’s the credit report fee. Your lender needs to pull your credit report to see your credit score and payment history. This helps them determine what interest rate to offer you. The better your credit score, the better your rate will typically be, which can save you thousands over the life of your loan.

Origination Charges

Here’s where things can get a bit pricey. The loan origination fee is what your lender charges for actually creating your mortgage. Think of it as their service charge for doing all the heavy lifting involved in funding your home purchase.

This fee typically ranges from half a percent to a full percent of your total loan amount. So if you’re borrowing three hundred thousand dollars, you could be looking at fifteen hundred to three thousand dollars just for this one fee. That’s a significant chunk of change, which is why it’s so important to factor this into your budget early on.

Some lenders also charge a separate underwriting fee if it’s not already included in the origination fee. Underwriting is the detailed risk assessment process where the lender analyzes your financial profile to determine if they should approve your loan.

Property-Specific Expenses

Your lender wants to know they’re making a sound investment, which means they need to know exactly what the property is worth. That’s where the appraisal comes in. A licensed appraiser will visit the property, assess its condition, compare it to similar recently sold homes in the area, and determine its fair market value.

Appraisal costs can vary based on the size and complexity of the property you’re buying. A standard single-family home in a typical neighborhood will cost less to appraise than a unique property or one in a rural area where comparable sales are harder to find.

While not always required by lenders, getting a professional home inspection is one of the smartest investments you can make. An inspector will thoroughly examine the property’s structure, systems, and components to identify any existing problems or potential issues. This could save you from buying a home with hidden problems that could cost tens of thousands to repair down the road.

Title Services and Insurance

Title-related costs are often some of the most confusing for first-time buyers, but they’re absolutely essential. Before you can officially own the property, someone needs to verify that the seller actually has the legal right to sell it to you. This involves researching public records to make sure there are no outstanding claims, liens, or disputes regarding the property.

Title insurance protects both you and your lender if any issues with the property’s ownership emerge after the sale. There are actually two types of title insurance policies involved in most transactions.

Lender’s title insurance protects the mortgage company’s investment if someone later claims they have a legal right to the property. This policy is typically required by lenders, and you’ll pay for it even though it protects them, not you.

Owner’s title insurance is your protection. While it’s optional, it’s highly recommended because it safeguards your ownership rights. In some regions, it’s customary for the seller to pay for the owner’s policy, but this varies by location and can be negotiated.

Insurance

Before you can close on your home, you’ll need to have homeowners insurance in place. Your lender requires this to protect their investment in case your home is damaged or destroyed. At closing, you’ll typically pay for your first year’s premium upfront.

The cost of homeowners insurance varies dramatically based on your location, the value and age of your home, the coverage limits you choose, and your deductible. Properties in areas prone to natural disasters, like hurricanes or wildfires, will have significantly higher premiums than homes in lower-risk areas.

If you’re putting down less than twenty percent, you might also need to pay for private mortgage insurance, or PMI. This protects your lender if you default on your loan. For government-backed loans like FHA loans, there’s an upfront mortgage insurance premium that gets added to your closing costs.

Government and Legal Fees

When you buy a home, the transaction needs to be officially recorded with your local government. Recording fees cover the cost of updating public records to show that you’re now the legal owner of the property. These fees vary by location since different counties and municipalities set their own rates.

If you’re in a state that requires an attorney to be present at closing, you’ll need to budget for attorney fees as well. Even in states where it’s not required, having a real estate attorney review your documents and represent your interests can be worthwhile, especially for first-time buyers or complex transactions.

Additional Closing Expenses

There are several other miscellaneous fees that might show up on your closing statement. Survey fees pay for a professional to verify the exact boundaries of your property. This is particularly important if there are questions about property lines or if you’re buying land.

If your property is in a flood zone, you’ll encounter flood determination fees. These pay for a company to assess whether the property is at risk and to monitor if that risk level changes over time. If flood insurance is required, that’s an additional ongoing expense you’ll need to budget for beyond closing.

Tax monitoring fees cover the service of tracking your property taxes and ensuring they get paid on time. Some lenders handle this through an escrow account where they collect money from you each month and pay your taxes and insurance on your behalf.

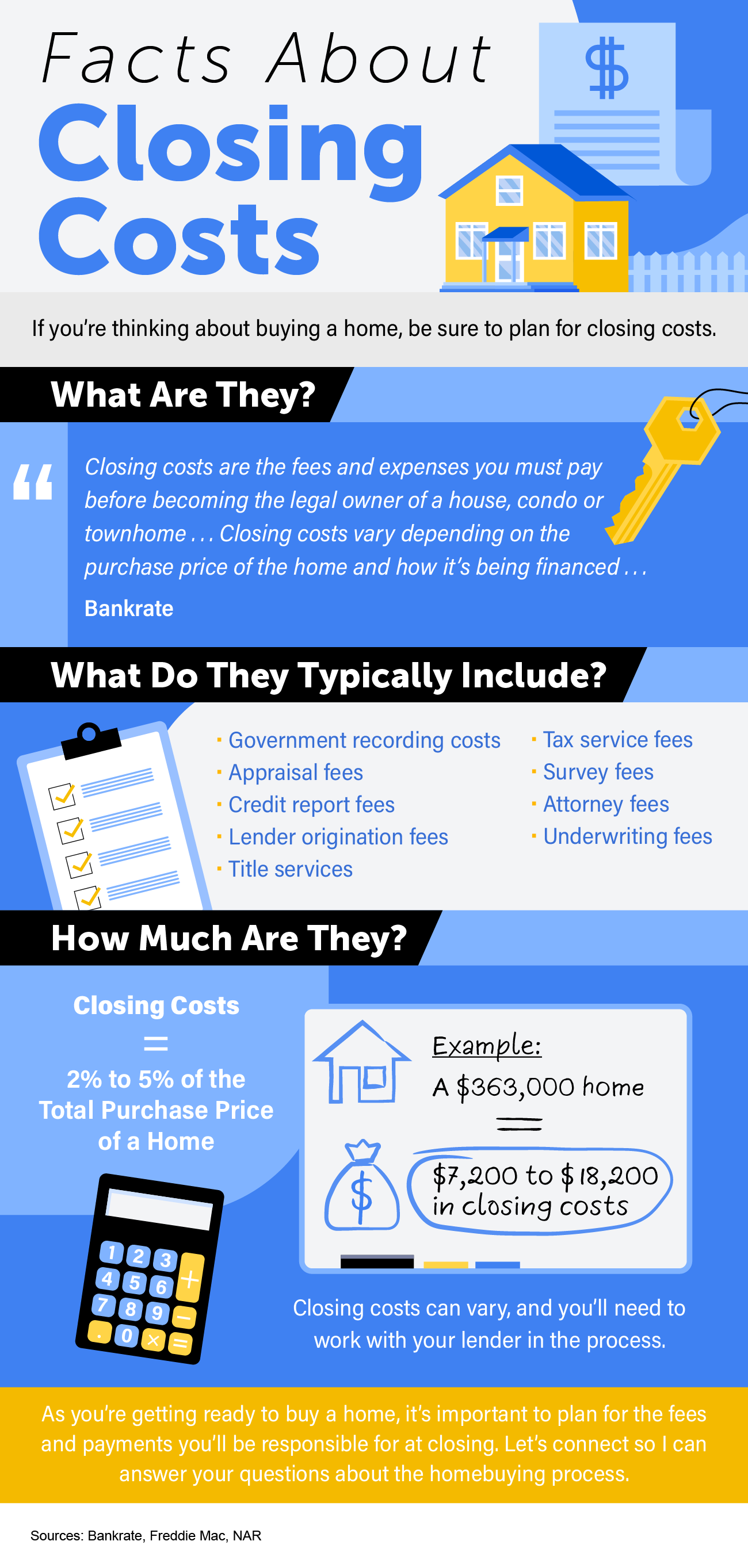

Calculating Expected Closing Costs

Now that you understand what closing costs include, let’s talk numbers. The general guideline is that closing costs typically fall between two and five percent of your home’s purchase price. That’s a pretty wide range, but several factors influence where your costs will land within that spectrum.

Your location plays a huge role. States with higher property taxes, for example, will have higher closing costs. Areas that require attorney representation at closing will add legal fees to your total. The price of your home obviously matters too – five percent of a six hundred thousand dollar home is quite different from five percent of a three hundred thousand dollar property.

Let’s walk through a practical example. Say you’re purchasing a home for four hundred thousand dollars. Using that two to five percent guideline, your closing costs could range anywhere from eight thousand dollars on the low end to twenty thousand dollars on the high end. That’s a significant amount of money that needs to be available in addition to your down payment.

If you’re buying a more affordable home priced at two hundred and fifty thousand dollars, your closing costs might range from five thousand to twelve thousand five hundred dollars. On the other hand, if you’re purchasing a more expensive property at seven hundred thousand dollars, you could be looking at fourteen thousand to thirty-five thousand dollars in closing costs.

These are estimates, of course. Your actual costs will depend on your specific situation, but these calculations give you a ballpark figure to work with when planning your budget.

Strategies for Reducing Closing Costs

The good news is that closing costs aren’t entirely set in stone. There are several legitimate strategies you can use to potentially reduce what you’ll pay at closing. Let’s explore some of the most effective approaches.

Negotiating with the Seller

In today’s real estate market, buyers often have more negotiating power than they might realize, especially if homes in the area are taking longer to sell. Sellers who are motivated to close the deal may be willing to help with your closing costs.

You can ask the seller to pay for specific expenses like the home inspection or provide you with a credit toward your closing costs. This is called a seller concession. The amount they’re willing to contribute often depends on market conditions, how long their home has been listed, and how motivated they are to sell.

This negotiation typically happens during the offer stage. Your real estate agent can help you craft an offer that includes a request for seller-paid closing costs without making your offer less attractive overall. Sometimes it makes sense to offer a slightly higher purchase price in exchange for the seller covering a portion of your closing costs, especially if you’re stretching to come up with cash at closing.

Shopping Around for Services

Not all closing costs are negotiable, but some are. You have the right to shop around for certain services like homeowners insurance, title services, and even some lender fees. Taking the time to compare options can lead to significant savings.

Homeowners insurance is an area where shopping around really pays off. Different insurance companies offer varying rates for similar coverage. Getting quotes from at least three different insurers can help you find the best combination of price and coverage. Don’t just go with the cheapest option, though – make sure you understand what’s covered and what’s excluded.

Some buyers don’t realize they can shop for title services. Your lender might suggest a title company, but you’re not obligated to use them. Getting quotes from different title companies could save you several hundred dollars, though in some areas, title fees are more standardized.

Assistance Programs

If closing costs are a significant financial hurdle, you might qualify for assistance programs that can help. These programs exist at the federal, state, and local levels, and they’re designed to help buyers overcome the upfront cost barriers to homeownership.

Many first-time buyer programs include assistance with closing costs, not just down payments. Some programs offer grants that don’t need to be repaid, while others provide low-interest loans. Eligibility requirements vary, but they often consider factors like your income level, the location where you’re buying, and whether you’re a first-time buyer.

Certain professions may also qualify for special programs. Teachers, healthcare workers, law enforcement officers, and veterans often have access to programs that can help with closing costs. Your real estate agent should be familiar with local programs and can point you in the right direction.

The Department of Housing and Urban Development maintains resources to help you find homebuying assistance programs in your area. Many state housing finance agencies also offer programs worth exploring. It’s worth spending some time researching what’s available – the money you save could make the difference between being able to afford your dream home or having to keep looking.

Timing Your Closing Strategically

Here’s a lesser-known strategy: the timing of your closing can affect your costs. You’ll need to prepay interest on your mortgage from the closing date until your first payment is due. If you close early in the month, you’ll prepay more interest than if you close near the end of the month.

For example, if you close on the fifth of the month, you’ll prepay interest for roughly twenty-five days. If you close on the twenty-eighth, you’re only prepaying for a few days. While this doesn’t change your total interest over the life of the loan, it does affect how much cash you need at closing.

Getting Estimates Before Closing

One of the most important protections for homebuyers is the Loan Estimate, a standardized form that your lender must provide within three business days of receiving your loan application. This document breaks down your estimated closing costs in detail, giving you a clear picture of what to expect.

The Loan Estimate isn’t just a casual estimate – it’s a legal document that your lender has to honor within certain limits. Most fees can’t increase by more than ten percent from what’s shown on your Loan Estimate. Some fees, like those for services where the lender requires you to use a specific provider, can’t increase at all.

A few days before closing, you’ll receive your Closing Disclosure, which shows your final closing costs. Compare this carefully to your Loan Estimate. If you notice any unexpected changes or fees that seem off, don’t hesitate to question them. You have the right to ask for explanations and challenge charges that don’t seem accurate.

Working with Real Estate Professionals

This might sound like obvious advice, but partnering with experienced real estate professionals can make a massive difference in your closing cost experience. A knowledgeable real estate agent doesn’t just help you find a home – they can guide you through every aspect of the transaction, including understanding and potentially reducing your closing costs.

Your agent should be able to connect you with reputable lenders who offer competitive rates and fees. They can recommend title companies, attorneys, inspectors, and insurance agents they’ve worked with successfully. Having these trusted resources makes the process smoother and can help you avoid unnecessarily high fees.

A good loan officer will also take the time to explain your closing costs in detail, answer your questions, and help you understand which costs are fixed and which might be negotiable. They should be upfront about all fees and shouldn’t surprise you with unexpected charges at the last minute.

Don’t be shy about asking questions. If something on your closing cost estimate doesn’t make sense or seems too high, speak up. Your real estate team is there to advocate for you and help you make informed decisions.

Avoiding Common Mistakes

Even with the best preparation, some buyers still make mistakes that can cost them money. Being aware of these common pitfalls can help you avoid them.

One of the biggest mistakes is waiting until the last minute to review your closing documents. You should receive your Closing Disclosure at least three business days before closing. Use this time to carefully review every line item. If you wait until you’re sitting at the closing table, you might miss errors or have no time to question charges.

Another mistake is not budgeting enough cash for closing. Remember, you’ll need your down payment plus your closing costs, and you should have some additional reserves for moving costs and immediate home expenses. Running out of available cash at closing can derail your entire transaction.

Some buyers focus so much on getting the lowest interest rate that they don’t pay attention to the associated fees. Sometimes a slightly higher interest rate with lower upfront costs is actually the better deal, especially if you don’t plan to stay in the home for a long time. Your loan officer can help you compare different scenarios to see what makes the most sense for your situation.

The Big Picture

At the end of the day, closing costs are simply a reality of the homebuying process. While they might seem like an annoying extra expense on top of your down payment, they serve important purposes. They ensure the property is legally transferred to you, protect everyone’s interests, and set you up for successful homeownership.

The key is to plan ahead. Start factoring closing costs into your savings plan from the very beginning of your home search. Understanding that you’ll need two to five percent of the purchase price on top of your down payment helps you set realistic timelines and price ranges for your home search.

Remember that being prepared is empowering. When you know what to expect, you can budget appropriately, ask the right questions, and potentially negotiate better terms. You’ll walk into closing day feeling confident rather than stressed about unexpected expenses.

Taking the Next Steps

If you’re ready to start your homebuying journey, make closing costs part of your planning conversation from day one. Talk with your real estate agent about typical closing costs in your area. Discuss with potential lenders what fees they charge and how your loan structure affects your closing costs.

Get pre-approved for your mortgage early in the process. This not only shows sellers you’re a serious buyer, but it also gives you a detailed breakdown of your expected costs through the Loan Estimate. You can use this information to fine-tune your budget and make sure you’re looking at homes you can truly afford when all costs are considered.

Don’t forget to explore assistance programs that might be available to you. Even if you think you won’t qualify, it’s worth investigating. Many programs have broader eligibility than people realize, and the potential savings could be substantial.

Most importantly, work with professionals you trust. Your real estate agent, loan officer, and other members of your homebuying team should be responsive, transparent, and willing to explain things in terms you understand. If something feels off or you’re not getting clear answers to your questions, it’s okay to seek second opinions or find different professionals to work with.

Buying a home is one of the biggest financial decisions you’ll ever make, and closing costs are an important part of that equation. By understanding what they are, how much to expect, and strategies for managing them, you’re setting yourself up for a smoother, less stressful path to homeownership. And trust me, when you’re finally holding those keys to your new home, you’ll be glad you took the time to prepare properly for every aspect of the purchase, including those sometimes-surprising closing costs.

Your dream of homeownership is within reach. With the right preparation and the right team supporting you, you’ll navigate closing costs and every other aspect of the homebuying process successfully. Here’s to finding your perfect home and closing the deal with confidence!