You’re standing at a crossroads. News headlines scream about economic uncertainty, job market shifts, and housing market chaos. Your social media feeds overflow with conflicting advice about whether now is the right time to purchase a home. With all this noise swirling around, it’s completely understandable if you’re second-guessing whether homeownership makes sense for you right now.

But here’s something interesting that might change your perspective: thousands of people just like you decided to move forward with their home purchase this year. And when you ask them about it? Most will tell you it was absolutely the right decision, market conditions and all.

Let’s dig into why they made the leap, what’s really happening with home values, and how you can make the smartest decision for your unique situation.

Personal Reasons That Matter

Here’s a truth that might surprise you: most people who bought homes recently didn’t make spreadsheets comparing interest rates from the past decade or obsess over whether they caught the absolute bottom of the market. Instead, they focused on something far more important—what they needed for their lives right now.

Creating Space for What Matters

Think about the last time you walked into your current living space. Does it fit who you are today? For many recent buyers, the answer was a resounding no. Maybe you’ve been working from home in a cramped apartment, holding Zoom meetings from your bedroom while trying to maintain some semblance of work-life boundaries. Perhaps your family has grown, and you’re literally tripping over toys in a space that made sense five years ago but feels impossibly small now.

Recent data shows that the desire for a home that actually fits your lifestyle is driving more purchase decisions than market timing ever could. Some buyers are finally getting that home office they desperately need. Others are finding places with yards where their kids can play without constant supervision. Still others are discovering the joy of having a guest room for when family visits, rather than awkwardly shuffling sleeping arrangements every holiday season.

Proximity

There’s something magical about living close to the people you care about. Recent buyers consistently mention proximity to family and friends as one of their top motivators. And honestly, can you blame them?

Imagine this: Instead of planning visits to see your parents weeks in advance, you can drop by for Sunday dinner. When your best friend texts asking if you want to grab coffee, you don’t have to decline because they live forty-five minutes away. When you need a hand moving furniture or someone to watch the dog for an afternoon, help is nearby rather than requiring elaborate coordination across time zones.

This kind of connection fundamentally changes your daily experience. It transforms isolated moments into shared experiences. It means your kids actually know their grandparents, not as people they see twice a year, but as regular presences in their lives. That’s not something you can put a price tag on, and it’s certainly not something worth delaying for slightly better interest rates.

First-Time Buyers Taking the Plunge

For many people, this year represented the moment they finally transitioned from renting to owning. After years of watching rent checks disappear into someone else’s pocket, they decided to start building their own equity instead.

First-time buyers talk about the freedom of making a space truly theirs. You can finally paint that accent wall the exact shade of blue you’ve been dreaming about. Want to install shelving or hang heavy artwork? Go for it—no need to check with a landlord. Planning to adopt a dog? You don’t need permission from anyone but yourself.

There’s also something deeply satisfying about stability. No more wondering whether your lease will renew at an affordable rate. No more worrying about whether your landlord might sell the property and force you to move. You’ve planted roots, and they’re yours.

The Simplification Movement

Not everyone is upsizing. A significant number of recent buyers are actually moving to smaller, more manageable homes. This isn’t about settling for less—it’s about intentionally choosing more.

Empty nesters are trading large family homes for cozy condos or smaller houses that require less maintenance and sit closer to the activities and amenities they actually use. Busy professionals are choosing homes that don’t demand every weekend be dedicated to upkeep and repairs. People nearing retirement are positioning themselves in locations that will support their lifestyle for decades to come.

Downsizing often means freeing up both money and time for what truly matters. Less space to clean means more time for hobbies. Lower utility bills mean more budget for travel. A more manageable property means less stress and more enjoyment of daily life.

What’s Actually Happening with Home Prices

Let’s cut through the sensational headlines and talk about what housing market experts are actually projecting. Because spoiler alert: the crash everyone keeps predicting probably isn’t coming.

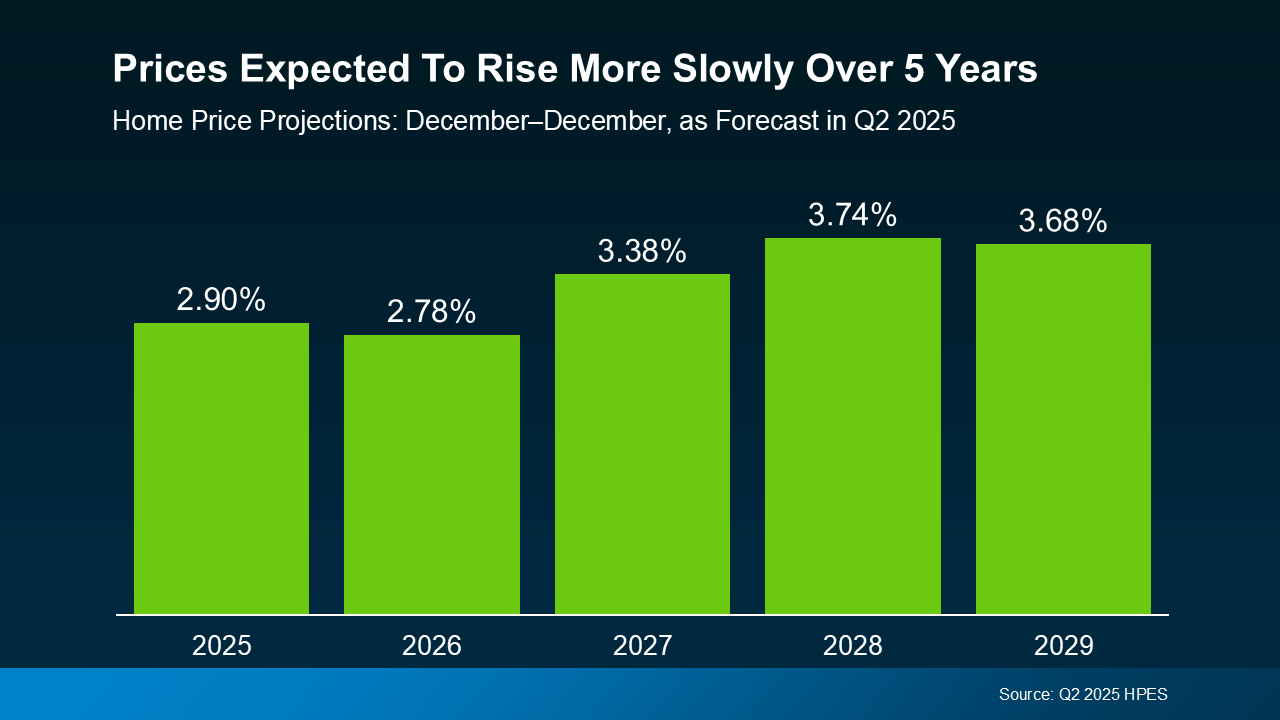

The Five-Year Outlook

Over one hundred leading housing market analysts recently shared their projections for where home values are headed through 2029. The consensus? Steady, sustainable growth—not a dramatic crash, but also not the wild appreciation we saw during the pandemic years.

On average, experts predict home values will increase by approximately 3.3% annually over the next five years. Now, before you dismiss that as modest, consider what it actually means. If you purchase a home today at the median national price, you’re looking at tens of thousands of dollars in equity building over the next half-decade. That’s not even accounting for the principle you’ll pay down through your mortgage payments.

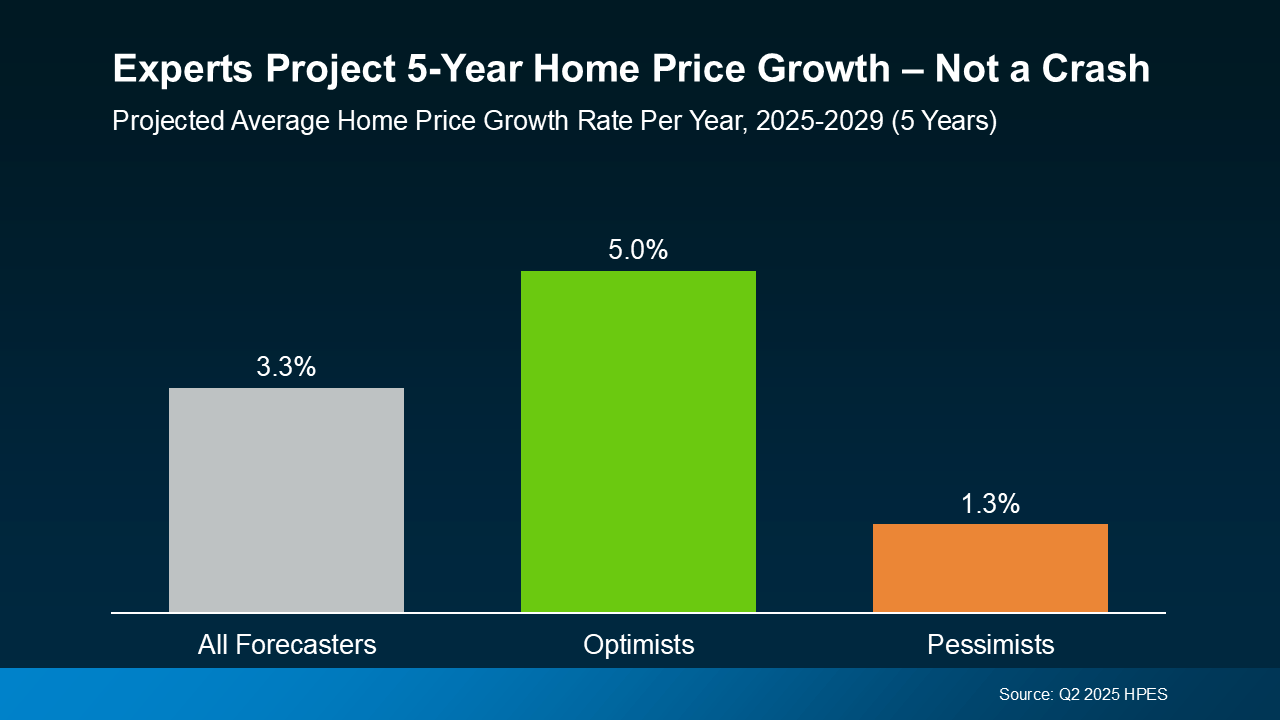

But here’s what’s really interesting: even the most conservative analysts in the survey still project growth. The pessimists (if you can call them that) forecast annual increases around 1.3%. Meanwhile, the optimists see growth closer to 5% per year. Notice something? Not a single expert group predicts a major nationwide decline.

Why This Growth Pattern Matters

The current trajectory represents something we haven’t seen in years: normalcy. The frenzied bidding wars and double-digit annual appreciation of recent years created an unsustainable situation. Homes became unaffordable for average families. People felt pressured to make rushed decisions or risk being priced out forever.

Now we’re seeing a return to healthier, more sustainable market dynamics. Some local markets might experience slight dips or flat growth in the short term, particularly where inventory has increased significantly. Other areas will continue appreciating faster than the national average because demand still outpaces supply.

This regional variation is actually a good thing. It means the market is functioning normally, responding to local economic conditions rather than being driven by pandemic-related panic and speculation.

The Factors Supporting Stability

Several fundamental factors are keeping the housing market stable and preventing the dramatic crash that some headlines predict.

Foreclosure rates remain remarkably low. During the housing crisis of 2008, foreclosures flooded the market with distressed properties that dragged down values across entire neighborhoods. Today’s lending standards are much stricter, and homeowners who purchased in recent years generally have solid financial footing.

Speaking of homeowners, equity levels are near historic highs. When you have substantial equity in your property, you have options if you encounter financial difficulties. You can sell without going through foreclosure. You can tap into a home equity line of credit to bridge temporary cash flow gaps. This cushion of equity provides stability to the broader market.

Finally, we’re not seeing the kind of oversupply that would crash prices. While inventory has increased from the extreme lows of recent years, we’re still not flooded with available homes in most markets. Basic supply and demand dynamics suggest that values should remain relatively stable when supply and demand are roughly balanced.

Regional Differences

Here’s something that often gets lost in national headlines: your local market might behave very differently from national trends. Real estate is inherently local, and understanding your specific area is crucial for making smart decisions.

Markets Showing Price Adjustments

Some cities, particularly in the Sun Belt, are experiencing price corrections after years of explosive growth. Places like Tampa, Phoenix, Dallas, and Miami saw enormous appreciation during the pandemic as people flooded in seeking better weather, lower costs of living, and remote work opportunities.

That surge in demand drove prices up rapidly—sometimes too rapidly. These markets are now adjusting as inventory increases and buyer enthusiasm moderates. If you’re looking in one of these areas, this adjustment might actually work in your favor, creating opportunities that didn’t exist a year or two ago.

However, “adjustment” doesn’t mean “crash.” Even in markets seeing the largest price declines, we’re typically talking about single-digit percentage drops, not the catastrophic collapses of 2008. And many buyers who purchased during the pandemic peak still have substantial equity because prices rose so dramatically.

Markets Maintaining Strength

Meanwhile, many markets in the Northeast and Midwest continue showing solid appreciation. Cities like Chicago, New York, and Boston are posting healthy year-over-year gains because they have tight inventory and steady demand driven by job markets and urban amenities.

These markets never experienced the same pandemic-driven frenzy, so they don’t need the same level of correction. They’re benefiting from fundamental factors like strong local economies, limited new construction, and consistent buyer demand.

What This Means for You

National statistics provide context, but your decision should be based on your local market. Are homes sitting on the market for months in your area, or do they still sell quickly? Are sellers reducing prices frequently, or are properties still commanding close to asking price? How does current inventory compare to historical norms for your region?

These hyperlocal factors matter far more than whether home prices rose or fell three percent nationally last quarter. A real estate professional familiar with your specific market can provide insights that general news articles simply cannot.

The Cost of Waiting

Let’s talk about something that doesn’t get discussed enough: what you’re giving up by waiting for “perfect” conditions that may never arrive.

Missing Life’s Moments

Every month you spend in a home that doesn’t fit your needs is a month you can’t get back. If you need more space for your growing family, your kids are getting older every day while you wait for interest rates to drop another quarter point. If you’re ready to simplify and downsize, you’re spending time and money maintaining a property that no longer serves your lifestyle.

Think about the memories you could be making in a home that truly fits. The dinner parties in that dream kitchen. The lazy Saturday mornings in your backyard. The home office where you can finally close the door and focus. These experiences have value that doesn’t show up on any financial calculator.

Equity Building

Here’s a simple truth: you start building equity the moment you close on a home. Every mortgage payment increases your ownership stake. Every year of appreciation adds to your net worth. When you wait, you’re not building either of these.

Let’s say you’re considering a home purchase but decide to wait a year because you think prices might drop five percent. Even if prices do decrease that much (which historical data suggests is unlikely in most markets), you’ve also missed out on a year of building equity and a year of appreciation in an upward-trending market.

Run the numbers on your specific situation, and you might be surprised to discover that the potential savings from waiting don’t offset what you lose by not building equity now.

Rent Isn’t Standing Still

While you’re waiting for the “perfect” time to buy, your rent probably isn’t staying flat. In many markets, rents continue increasing steadily. Every rent increase makes homeownership relatively more affordable and means you’re paying more for the temporary housing arrangement you’re already dissatisfied with.

Consider this: if your rent increases by $100 per month over the next year while you wait to buy, that’s $1,200 in additional housing costs that build exactly zero equity. Meanwhile, that same $100 applied to a mortgage payment would be increasing your ownership stake in a property.

Making the Decision

So how do you cut through all the noise and make a decision you’ll feel good about five or ten years from now?

Your Personal Situation

Start by looking inward rather than outward. What do you need from a home right now? Not what do market conditions suggest you should do, but what would genuinely improve your daily life and support your goals?

Consider your job stability. Are you in a career and location where you expect to stay for at least a few years? Real estate generally makes more sense as a medium to long-term investment rather than a short-term flip.

Look at your financial foundation. Do you have a solid emergency fund? Is your debt manageable? Can you comfortably afford the monthly payment without stretching your budget dangerously thin?

Think about your life plans. Are you likely to need to relocate for work? Are major life changes on the horizon that might affect your housing needs? Homeownership works best when you have some stability and predictability in your life situation.

Your Local Market

Once you’ve assessed your personal readiness, dive deep into your specific market. This is where working with a knowledgeable local real estate professional becomes invaluable.

What’s the current inventory situation in your price range and desired neighborhoods? Are you competing with dozens of other buyers, or do you have some negotiating leverage? How long are properties typically sitting on the market before selling?

Are there local economic factors that might affect values in the near term? Major employers moving in or out? Significant infrastructure projects? Changes to zoning or development patterns?

Understanding these local dynamics helps you make informed decisions rather than gambling based on national headlines that may not reflect your reality at all.

Run Your Personal Numbers

Take the time to crunch the numbers for your specific situation. Online calculators can help, but consider sitting down with a mortgage professional and a financial advisor to really understand the implications.

How does your anticipated monthly housing payment (including insurance, taxes, and maintenance reserves) compare to your current rent? What’s your break-even timeline if you had to sell? How would a modest increase or decrease in property values affect your financial position?

Don’t forget to factor in the tax implications. For many buyers, the mortgage interest deduction and the long-term capital gains treatment of home sales provide significant financial benefits that rent doesn’t offer.

Consider the Intangible Benefits

Not everything that matters can be quantified. Yes, you need to make sure homeownership makes financial sense. But there’s also real value in the stability, autonomy, and sense of belonging that comes with owning your home.

Think about what it would mean to never worry about lease renewals or unexpected moves. Consider the satisfaction of building something that’s truly yours. Imagine the security of knowing you’re protected from rent increases and can stay as long as you choose.

These factors are harder to measure, but they’re very real components of your overall quality of life.

Moving Forward

If you’ve determined that homeownership aligns with your goals, your finances, and your life situation, the next step is taking action without getting paralyzed by analysis.

Work with Trusted Professionals

Surround yourself with experts who can guide you through the process. A experienced real estate agent brings market knowledge and negotiation skills that can save you thousands of dollars and countless headaches. A mortgage professional helps you understand your financing options and structure your loan optimally. A home inspector protects you from buying a property with hidden issues.

These professionals exist to make your transaction smoother and more successful. Use their expertise rather than trying to figure everything out on your own.

Stay Focused on Your Why

Throughout the homebuying process, you’ll encounter moments of doubt. Markets will fluctuate. Interest rates might shift. You’ll see properties that don’t quite work or negotiations that fall through. This is all normal.

In these moments, return to your original motivation. Why did you decide homeownership was right for you? What were the needs and goals driving your decision? Keeping your “why” front and center helps you navigate the inevitable ups and downs without losing sight of what matters.

Don’t Try to Time the Market Perfectly

Here’s a truth that applies to both real estate and investing: nobody consistently times the market perfectly. The people who build wealth do so by making sound decisions based on solid fundamentals and then sticking with them long enough for compound growth to work its magic.

The best time to buy a home is when you’re financially ready, you’ve found a property that meets your needs, and homeownership aligns with your life goals. It’s not when mortgage rates hit their absolute lowest point or when you’ve correctly predicted the exact bottom of the local market cycle.

Look Beyond the Headlines

In a world of 24-hour news cycles and social media hot takes, it’s easy to feel overwhelmed by conflicting information about the housing market. Remember that most headlines are designed to generate clicks, not to provide nuanced guidance for your specific situation.

The reality is more complex and more boring than dramatic headlines suggest. Most markets are experiencing modest, sustainable growth. Some areas are adjusting after rapid pandemic-era appreciation. Others are showing steady strength based on local fundamentals.

What matters is not whether the national market went up or down last quarter. What matters is whether homeownership serves your needs, fits your finances, and supports the life you want to build.

Your Home, Your Timeline, Your Decision

At the end of the day, this is your decision to make. Not what the headlines suggest you should do. Not what worked for your neighbor or your coworker. What works for you, based on your unique situation, goals, and needs.

The buyers who purchased homes this year didn’t wait for perfect conditions because perfect conditions rarely exist. They evaluated their situations honestly, ran the numbers, consulted with professionals, and moved forward when it made sense for them.

Many of them will tell you they’re sleeping better now. They’re enjoying homes that finally fit their lives. They’re building equity with every payment. They’re creating memories in spaces that feel like home.

That could be you. Not because market conditions are perfect, but because you made a well-informed decision based on sound fundamentals and your personal circumstances.

If you’re ready to explore what homeownership might look like for you, start by having honest conversations with real estate and financial professionals who can help you evaluate your specific situation. They can help you understand your local market, assess your readiness, and determine whether now is your right time—regardless of what the headlines say.

Because here’s the ultimate truth: the people who buy homes aren’t trying to time the market perfectly. They’re trying to build lives that work for them. And that’s something worth moving forward on, market conditions and all.