(Updated 11/04/25)

Here’s something that might surprise you: single women are absolutely crushing it in the housing market right now. If you’ve been thinking about buying your own place but wondering if you can do it solo, the answer is a resounding yes. In fact, you’d be joining a growing movement of women who are making homeownership happen on their own terms.

Let’s talk about what’s really going on in the housing market and why more women than ever are deciding to take the leap into homeownership.

The Numbers Tell an Inspiring Story

If you’re wondering whether you’re alone in wanting to buy a home as a single woman, let me put your mind at ease. According to recent data from the National Association of Realtors, single women make up about 19% of all homebuyers. Compare that to single men, who account for only 10% of buyers, and you’ll see that women are nearly doubling their male counterparts when it comes to going solo on a home purchase.

But it gets even better. When you look at the actual ownership numbers across the country, single women own roughly 11.14 million homes, while single men own about 8.42 million. That’s a difference of nearly 2.72 million homes. Think about that for a second – that’s millions of women who decided they weren’t going to wait for a partner or perfect circumstances to invest in their future.

What’s Driving Women to Buy Homes Alone

So why are so many women jumping into homeownership on their own? The reasons are actually pretty varied, and they’re not just about money (though that’s definitely part of it).

Building Wealth for the Future

Let’s start with the financial side, because it’s a big one. When you buy a home, you’re not just getting a place to hang your hat – you’re making an investment that typically grows in value over time. Every mortgage payment you make is building equity, which is basically your stake in the property. It’s like a forced savings account that you can tap into later.

Ksenia Potapov, an economist at First American, puts it perfectly when she talks about how single women are increasingly pursuing homeownership and taking advantage of the wealth-building benefits that come with it. Real estate has historically been one of the most reliable ways to build long-term wealth, and women are figuring this out and taking action.

Independence and Security

But here’s the thing – it’s not all about the dollars and cents. For many women, buying a home is about something deeper. It’s about having your own space where you make all the decisions. Want to paint the walls purple? Go for it. Want to adopt three cats? Nobody’s going to stop you. There’s something incredibly empowering about knowing this space is yours.

The security aspect can’t be overlooked either. When you own your home, you’re not worried about a landlord selling the property or raising your rent by hundreds of dollars with only a month’s notice. You have stability, and in today’s uncertain world, that peace of mind is worth a lot.

Personal Reasons Matter Too

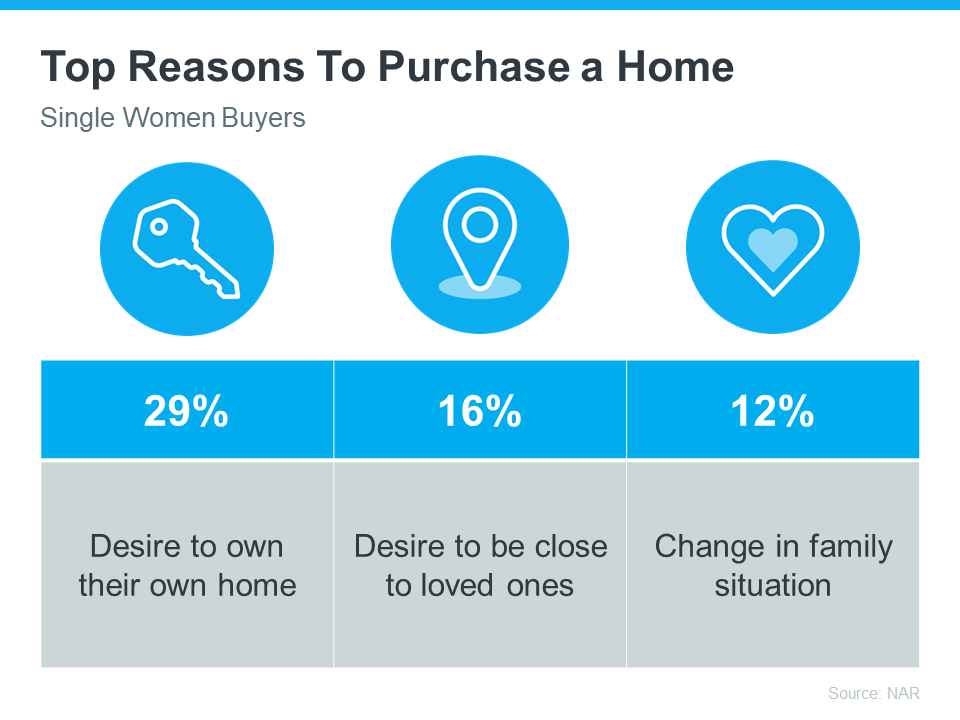

According to the National Association of Realtors research, single women cite all kinds of reasons for buying homes that have nothing to do with investment returns. Some are looking for a place where they feel truly comfortable and at home. Others want to be closer to family and friends, or they need more space for hobbies, a home office, or just room to breathe.

Some women are buying because they’re tired of dealing with landlords and want to have control over their living situation. Others see it as a major life milestone – something to be proud of accomplishing on their own. And honestly? All of these reasons are completely valid.

Where Women Are Making Homeownership Moves

The patterns of where single women are buying homes reveal some interesting trends. It’s not uniform across the country – some states have way more single women homeowners than others.

States Leading in Single Women Homeownership

New Mexico takes the top spot, with single women owning about 15.26% of all owner-occupied homes in the state. That’s a pretty impressive figure when you think about it. Mississippi comes in second at 15.07%, followed by West Virginia at 14.73%. These states show that women are actively pursuing homeownership and succeeding at it.

What’s interesting is that these percentages tell us that in these states, women are creating their own path to financial stability through real estate, regardless of relationship status. They’re not waiting around for someone else to make it happen.

The Few Exceptions

Now, it wouldn’t be fair to paint the picture that single women outnumber single men in homeownership everywhere. There are actually three states where single men own more homes: North Dakota, South Dakota, and Alaska. In North Dakota, for instance, single men own about 13.52% of homes compared to 10.75% for single women.

These exceptions are likely due to the unique economic and demographic characteristics of these states. They tend to have industries that traditionally employ more men, and the overall population dynamics are different from the rest of the country.

The Biggest Gaps

Delaware and Connecticut have the largest gaps between single women and single men homeowners. In Delaware, the difference is 5.23 percentage points, with single women owning 14.06% of homes compared to just 8.83% for single men. Connecticut isn’t far behind with a 5.06 percentage point gap.

These large disparities suggest that in some markets, women are particularly motivated or able to achieve homeownership independently. It would be fascinating to dig deeper into what makes these markets so conducive to single women homeowners.

Challenges Single Women Face

Okay, so we’ve talked about the good news. But let’s be real – buying a home as a single woman isn’t without its challenges. There are some genuine obstacles that women face in the housing market, and it’s important to acknowledge them.

The Pay Gap Is Real

Here’s an uncomfortable truth: women typically earn less than men for the same work. According to the U.S. Bureau of Labor Statistics, women’s median weekly earnings are about 83.6% of what men make. That’s not a small difference – it adds up to thousands of dollars every year.

When you’re saving for a down payment, that pay gap makes a huge difference. If you’re earning less, it naturally takes longer to accumulate enough money to put down on a home. This is one reason why the median age for single female first-time homebuyers is 40, compared to 34 for single men. That six-year difference represents six years of not building equity.

The Down Payment Dilemma

Speaking of down payments, they’re a major hurdle. When Bankrate surveyed aspiring homeowners, they found that 74% of women anticipated it would take at least a year to save up for a down payment. While this was actually slightly better than the 79% of men who said the same, the reality is that saving for a down payment on a single income is tough.

Some women also report feeling like they need to have everything perfectly in order before they can buy. They want a bigger down payment, a higher credit score, more savings in the bank. While being financially prepared is smart, waiting for perfect conditions means potentially missing out on years of equity building.

Interest Rates Hit Single-Income Buyers Harder

The recent rise in interest rates has made homeownership more challenging for everyone, but it hits single-income buyers particularly hard. When you’re the only one paying the mortgage, higher interest rates mean significantly higher monthly payments. Real estate agents working specifically with single women report that many potential buyers are holding off because the numbers just don’t work with current rates.

The Home Value Gap

Here’s something that doesn’t get talked about enough: research from Yale and Zillow shows that homes owned by women tend to be worth less than those owned by men. This isn’t because women are buying inferior properties – it’s a complex issue involving negotiation, the timing of purchases, and how homes are maintained and improved over time.

Women often end up buying properties at slightly higher prices and selling them for slightly lower prices compared to men. Over time, this impacts the total amount of equity wealth that women can accumulate through homeownership. It’s not a huge difference in any single transaction, but it adds up.

Making Your Homeownership Dreams a Reality

If you’re a single woman thinking about buying a home, here’s what you need to know to make it happen successfully.

Start with a Great Real Estate Agent

This is probably the single most important piece of advice: find a real estate agent you trust and who understands your situation. You want someone who gets that you’re buying on a single income and who will advocate for you throughout the process.

Be upfront about your goals and why homeownership matters to you. Maybe you’re looking at it primarily as an investment, or maybe you’re more focused on finding a community where you can put down roots. Whatever your priorities are, make sure your agent knows them. They should be keeping what’s critical for you front and center as they show you properties and help you negotiate.

A good agent will also help you understand the local market. Is it currently favoring buyers or sellers? How much inventory is available? What are homes actually selling for versus what they’re listed for? This information is crucial for making smart offers and negotiating effectively.

Do Your Homework on Financing

Before you even start looking at homes, get pre-approved for a mortgage. This tells you exactly how much you can afford and shows sellers that you’re a serious buyer. Shop around with multiple lenders to make sure you’re getting the best rate and terms.

Look into programs specifically designed to help first-time homebuyers. There are options like Home Ready and Home Possible that offer more flexible down payment requirements. Some programs will help with closing costs too, which can save you thousands of dollars upfront.

Don’t assume you need a 20% down payment to buy a home. While it’s nice to have if you can manage it, many programs allow you to put down as little as 3-5%. Yes, you’ll pay private mortgage insurance if you put down less than 20%, but that might be worth it to get into a home sooner and start building equity.

Master the Art of Negotiation

Here’s something women sometimes struggle with: being tough negotiators. Studies show that women tend to be more emotionally attached to the homes they’re considering, which can make it harder to walk away from a bad deal.

It’s important to remember that buying a home is both an emotional decision and a financial one. Yes, you want to love where you live, but you also need to make sure you’re making a smart investment. Know your limits going in, and don’t be afraid to walk away if the numbers don’t work or if the seller isn’t willing to meet you halfway.

Real estate agents who work primarily with single women emphasize the importance of disconnecting from the emotional tie when it’s time to negotiate. You can love a house and still be a savvy negotiator. In fact, the better you negotiate, the more equity you’ll have in your home from day one.

Understand the Market Timing

Timing isn’t everything, but it matters. If you’re buying in a hot seller’s market where there are multiple offers on every property, you might need to be more aggressive with your offer. But you also need to be careful not to overpay just because everyone else is bidding up prices.

In a buyer’s market where there’s more inventory and fewer competing buyers, you have more leverage to negotiate on price, ask for repairs, or request that the seller cover some of your closing costs. Understanding where your local market stands right now can help you make strategic decisions.

Don’t Go It Alone

While you might be buying the house by yourself, that doesn’t mean you have to navigate the process alone. In addition to your real estate agent, consider bringing in other professionals like a home inspector and maybe even a real estate attorney if the transaction is complex.

Join online communities or local groups for single women homebuyers. The advice and support you’ll get from others who’ve been through the process is invaluable. They can recommend lenders, inspectors, contractors, and share their own lessons learned.

Home Equity and Building Wealth

Once you’re a homeowner, it’s important to think strategically about building equity and using your home as a wealth-building tool.

How Equity Works

Every time you make a mortgage payment, a portion of that payment goes toward paying down the principal balance of your loan. That’s equity building right there. Additionally, as home values appreciate over time (which they generally do), you’re gaining equity without doing anything at all.

After a few years of ownership, you’ll likely have built up substantial equity. This equity can be tapped through a home equity loan or line of credit if you need funds for renovations, debt consolidation, or other major expenses. Just be thoughtful about borrowing against your home – it’s putting your property at risk if you can’t repay.

Making Smart Improvements

Some home improvements add more value than others. If you’re thinking about renovations, focus on updates that will give you the best return on investment. Kitchen and bathroom updates typically pay off well, as do fresh paint, good landscaping, and fixing any major maintenance issues.

You don’t need to do expensive renovations to maintain or increase your home’s value. Sometimes the best improvements are the unsexy ones – a new roof when needed, updating old electrical or plumbing, making sure the HVAC system works efficiently. These keep your home in good condition and prevent small problems from becoming big, expensive ones.

The Long Game

Remember that building wealth through homeownership is usually a long-term play. While some people get lucky and see rapid appreciation, for most homeowners, the real benefits come from staying in the home for several years, letting equity build up, and taking advantage of the forced savings that comes with paying a mortgage instead of rent.

The longer you own your home, the more you benefit from appreciation and the less you owe on your mortgage. If you can avoid selling in the first few years after buying (when transaction costs eat up a lot of your equity), you’ll be in a much better position financially.

The Legal Protections You Should Know About

It’s important to understand that you have legal protections as a homebuyer and mortgage applicant.

You Cannot Be Discriminated Against

Federal law prohibits lenders from denying you a loan based on your sex, sexual orientation, gender identity, or marital status. The Equal Credit Opportunity Act makes this crystal clear. If a lender tries to treat you differently because you’re a single woman, that’s illegal.

Unfortunately, discrimination still happens sometimes. Research has shown that female borrowers are denied mortgages at slightly higher rates than male borrowers, and women applying for home equity loans are denied twice as often as men (6% versus 3%). If you believe you’ve been discriminated against, you can file a complaint with the Consumer Financial Protection Bureau or the Department of Housing and Urban Development.

Understanding Your Rights

You have the right to apply for credit in your own name, regardless of marital status. You have the right to have all your income counted, including part-time work, investments, and child support or alimony. Lenders must consider your complete financial picture fairly.

You also have the right to know why you were denied credit if your application is rejected. Lenders are required to provide specific reasons in writing. This transparency helps you understand what you might need to improve before applying again.

Historical Context Matters

It’s worth understanding that women haven’t always had these protections. Before the Equal Credit Opportunity Act was passed in 1974, women routinely faced discrimination in lending. Banks could require a woman to have a male co-signer, could refuse to count her income, or could simply deny her application based on gender.

While we’ve made progress, studies show there’s still work to be done. Women – particularly women of color – are still more likely to be steered toward subprime loans even when they qualify for better terms. Being aware of this history helps you stay vigilant and advocate for yourself.

Special Considerations for Different Life Stages

Depending on where you are in life, there might be specific factors to consider.

Young Professionals Just Starting Out

If you’re in your 20s or early 30s and thinking about buying, the biggest challenge is usually the down payment. You might not have had as much time to save, but you also have the advantage of starting to build equity early. Even if you can only afford a smaller starter home or a condo, getting on that property ladder now means you’ll have more options down the road.

Consider whether you might relocate for work in the next few years. If there’s a good chance you’ll need to move, renting might make more sense short-term. But if you’re fairly settled in your location, buying could be a smart move.

Mid-Career Buyers

If you’re in your 40s or 50s and buying for the first time, you might have more saved for a down payment and a stronger income, but you also have fewer years until retirement to pay off the mortgage. Think about what loan term makes sense for you – a 15-year mortgage will have higher payments but less total interest, while a 30-year mortgage is more affordable month-to-month.

At this stage, you might also be thinking about not just your current needs but what you’ll need as you age. Is the house going to work for you long-term? Is it near family or friends who can provide support as you get older?

Pre-Retirement and Retirement Buyers

Buying a home close to or during retirement is absolutely possible, though you’ll want to think carefully about the financial implications. Make sure the monthly payments fit comfortably in your retirement budget. Consider whether you want to take on a mortgage in retirement or if you’d prefer to buy something less expensive that you can pay for outright.

Think about accessibility and maintenance too. A house with lots of stairs or a huge yard might sound great now, but will it be manageable in 10 or 20 years? Some women in this age group choose to downsize into a smaller, more manageable property.

Resources and Support for Women Homebuyers

You don’t have to figure all this out on your own. There are tons of resources available specifically to help women become homeowners.

Government and Non-Profit Programs

The U.S. Department of Housing and Urban Development offers housing counselors who can walk you through the homebuying process. These counselors are free or low-cost and can help you understand your options, improve your credit, and find down payment assistance programs.

The National Homebuyers Fund offers down payment assistance grants in many states. Instead of having to come up with the full down payment yourself, you might be able to get a grant to cover part or all of it. This can make homeownership accessible years sooner than it would be otherwise.

Educational Resources

The Consumer Financial Protection Bureau has excellent guides on mortgages and home equity loans that explain everything in plain English. The Federal Trade Commission also has consumer advice specific to home buying that can help you avoid scams and understand your rights.

Many local housing authorities offer first-time homebuyer classes. These are usually free or very cheap and cover everything from understanding mortgages to negotiating offers to maintaining your home. The education you get in these classes is invaluable.

Online Communities and Local Groups

Look for online groups or local meetups for single women homebuyers in your area. These communities can provide emotional support, practical advice, and referrals to great real estate agents, lenders, and contractors. Sometimes just knowing other women who’ve successfully bought homes on their own gives you the confidence boost you need.

Some real estate brokerages focus specifically on educating and helping single women buy homes. They understand the unique challenges you might face and can provide targeted support throughout the process.

The Bottom Line on Single Women and Homeownership

Here’s what it all comes down to: yes, being a single woman in the housing market comes with some challenges. The pay gap is real, saving for a down payment takes time, and current interest rates aren’t helping anyone. But millions of women are doing it successfully, and there’s no reason you can’t be one of them.

Homeownership is one of the most powerful ways to build wealth over time. Every payment you make on a mortgage is an investment in your future, unlike rent which simply disappears. The independence and security that comes with owning your own place is hard to put a price on.

The trend is moving in the right direction. More young women are buying homes earlier, which means they’ll build more equity over their lifetimes. The resources and protections available to women homebuyers are better than they’ve ever been. And culturally, the idea that you need to be married or have a partner to buy a home is becoming outdated.

If you’re on the fence about whether to take the plunge into homeownership, talk to a trusted real estate agent about what’s possible in your situation. Get pre-approved for a mortgage to see where you stand financially. Run the numbers to understand what homeownership would cost you monthly compared to what you’re paying in rent.

You might find that homeownership is more achievable than you thought. Or you might realize you need another year or two to build up your savings and improve your credit. Either way, you’ll have a clear picture of where you stand and what steps you need to take.

The housing market can feel intimidating, especially when you’re going it alone. But remember – nearly 20% of all homebuyers are single women just like you. You’re not alone in this journey, even if you’re buying solo. With the right support, resources, and determination, homeownership is absolutely within your reach.

The key is to be strategic, educate yourself, advocate for yourself throughout the process, and remember that this is an investment in your future. Whether you’re motivated by financial goals, the desire for independence, or just wanting a place that truly feels like home, those are all valid reasons to pursue homeownership.

Take that first step. Talk to a real estate agent. Get pre-approved. Start looking at what’s available in your area. You might be surprised at how close you already are to making your homeownership dreams a reality. And when you finally get the keys to your own place, you’ll join the millions of women who’ve discovered that buying a home on their own was one of the best decisions they ever made.