(Updated 10/17/25)

Let’s be real for a second – the idea of buying and selling a house at the same time sounds about as relaxing as juggling chainsaws while riding a unicycle. But here’s the thing: thousands of people pull this off successfully every year, and with the right game plan, you absolutely can too.

Whether you’re upgrading to accommodate a growing family, downsizing after the kids have flown the nest, or simply ready for a change of scenery, navigating both transactions simultaneously doesn’t have to be the nightmare you might be imagining. Sure, it requires some strategic thinking and careful coordination, but armed with the right information and a solid team in your corner, you can make this happen without losing your mind in the process.

In this guide, we’re going to walk through everything you need to know about buying and selling at the same time. We’ll explore your options, discuss the pros and cons of different approaches, and share practical strategies that’ll help you land on your feet. Think of this as your roadmap through what might otherwise feel like navigating a maze blindfolded.

This Situation Is Common

Before we dive into the nitty-gritty details, let’s talk about why so many homeowners find themselves in this position. The reality is that most people who own homes need to sell their current place to afford their next one. We’re not all sitting on piles of cash or able to comfortably swing two mortgage payments at once.

According to recent data, the average homeowner has built up a substantial amount of equity in their property – we’re talking over $300,000 in many cases. That’s not pocket change! For most folks, accessing that equity is essential for making their next move possible. It becomes the down payment on their dream home, helps cover closing costs, or provides the financial cushion needed to make the transition smooth.

The challenge, of course, is timing. Real estate transactions are complex beasts with lots of moving parts, multiple people involved, and timelines that don’t always cooperate with each other. One deal might be racing ahead while the other drags its feet. It’s enough to give anyone a headache.

But here’s some good news: understanding your options and planning ahead can dramatically reduce the stress and uncertainty involved in this process.

But the best way to determine what’s best for you and your specific situation? Talk to a trusted local agent.

But the best way to determine what’s best for you and your specific situation? Talk to a trusted local agent.

Look at Your Local Market

Before you make any major decisions, you need to understand what’s happening in your specific real estate market. And I mean really understand it – not just what you’ve heard on the news or from your neighbor who fancies themselves a real estate expert.

Markets can vary dramatically not just from state to state, but even from neighborhood to neighborhood within the same city. What’s happening in downtown could be completely different from what’s going on in the suburbs just twenty minutes away.

Buyer’s Markets

In a buyer’s market, homes are sitting around like wallflowers at a middle school dance – there are more properties available than people looking to buy them. For you as a seller, this means your house might take longer to move. Buyers have options, so they can afford to be picky and negotiate hard on price.

However, if you’re also buying in that same market, you’re in luck! You’ll have more properties to choose from and potentially more negotiating power when you find the one you want. Sellers in a buyer’s market might be more willing to accept contingent offers or work with you on timing because they’re motivated to close a deal.

The key strategy here is to be patient and realistic. You might need to price your current home competitively to attract buyers, but you’ll likely make up for it with better terms on your purchase.

Seller’s Markets

Flip the script, and you’ve got a seller’s market – more buyers than available homes. If you’ve spent any time house hunting in the last few years, you’ve probably experienced this firsthand. Multiple offers, bidding wars, homes selling before they even officially hit the market. It’s intense out there.

The good news? Your current home will likely sell quickly and possibly for more than you expected. The challenging news? Finding your next place and securing it might feel like competing in the Hunger Games of real estate.

In a seller’s market, you’ll want to be strategic. Consider asking buyers for a rent-back agreement, which gives you some breathing room to find your next place even after you’ve technically sold. Sellers are often willing to accommodate reasonable requests from buyers because they don’t want to lose a solid offer in a competitive environment.

When You’re Playing in Two Different Markets

Now, if you’re selling in one market and buying in another – say, relocating from a major city to a smaller town, or vice versa – things get even more interesting. You might be selling in a hot market where homes fly off the shelves, but buying in a slower market where you have more time and options. Or the opposite could be true.

This is where having knowledgeable real estate professionals in both locations becomes absolutely critical. They can help you understand the timing and strategy needed to coordinate both transactions successfully.

Build a Dream Team

Listen, I know it’s tempting to try to save money by going it alone or working with your cousin’s friend who just got their real estate license last month. But when you’re managing both a purchase and a sale simultaneously, this is not the time to cut corners on professional help.

Finding the Right Real Estate Agent

A skilled, experienced real estate agent is worth their weight in gold when you’re juggling two transactions. And I’m not just talking about someone who can unlock doors and post photos on Zillow. You need someone who understands the intricacies of coordinating multiple deals, knows your market inside and out, and has the negotiation skills to get you the best possible outcomes on both sides.

What should you look for? Start by asking friends and family for recommendations, but don’t just go with the first name someone throws at you. Interview multiple agents. Ask about their experience with simultaneous transactions. How many have they handled? What strategies do they typically recommend? Can they provide references from past clients who were in similar situations?

Pay attention to how they communicate with you during the initial conversations. Are they responsive? Do they take time to understand your specific situation and concerns? Or are they just trying to rush you into signing a listing agreement?

If you’re buying and selling in the same general area, seriously consider using the same agent for both transactions. This streamlines communication enormously and ensures someone with a complete picture of your situation is coordinating all the moving pieces.

Legal Expertise

Depending on where you live, you might be required by law to have a real estate attorney involved in your transactions. But even if it’s not legally required in your state, bringing one on board is a smart move when you’re dealing with the complexity of simultaneous deals.

A good real estate attorney can review contracts, help you understand what you’re signing, negotiate terms that protect your interests, and handle any legal issues that pop up during the process. When you’re dealing with complicated contingencies and coordinating closing dates, having someone who speaks fluent legalese advocating for you is invaluable.

Your Mortgage Lender Is Part of the Team Too

Don’t sleep on the importance of having a responsive, experienced mortgage lender in your corner. They’re not just the people who approve your loan – they’re key players in making sure your purchase goes through smoothly and on time.

Start conversations with your lender early. Be upfront about your situation and timeline. Ask questions about pre-approval, what documentation they’ll need, and how long the process typically takes. The more they understand about your plans, the better they can support you.

Keep in mind that mortgage approval can take anywhere from 45 to 60 days in many cases, sometimes longer if there are complications. Knowing this timeline helps you plan your move more effectively.

Getting Your Finances Order

Real talk time: before you start looking at listings or putting your house on the market, you need to have a crystal-clear understanding of your financial situation. And I mean down-to-the-penny clear.

Calculating Your Home Equity

Your home equity is basically the difference between what your house is currently worth and what you still owe on your mortgage. If your home would sell for $400,000 and you have $150,000 left on your mortgage, you’ve got $250,000 in equity (minus selling costs, which we’ll get to).

This number is crucial because for most people, it represents the bulk of the money they’ll have available for their next purchase. But here’s the catch – you can’t actually access that equity until your sale closes. It’s like having money in a locked safe; you know it’s there, but you can’t spend it yet.

To figure out your likely equity, start by getting a realistic estimate of your home’s current market value. Your real estate agent can help with this by looking at comparable sales in your area. You might also want to consider getting a professional appraisal, though that’ll cost you a few hundred dollars.

Once you know what your home is likely worth, subtract your remaining mortgage balance and estimated selling costs. Selling costs typically include your agent’s commission (usually 5-6% of the sale price), closing costs, any repairs or improvements you need to make, and potentially other fees like transfer taxes.

Your Buying Power

On the flip side, you need to know what you can afford to spend on your next home. This involves more than just looking at your equity. You need to consider your income, existing debts, credit score, and what kind of mortgage you’ll qualify for.

Lenders use something called your debt-to-income ratio to determine how much they’re willing to lend you. This is basically all your monthly debt payments (including your new mortgage payment) divided by your gross monthly income. Most lenders want to see this ratio below 43%, though some programs allow higher ratios.

Here’s where things can get tricky: if you’re trying to buy before you sell, lenders will often count your existing mortgage payment in that debt-to-income calculation until your current home is sold. This can significantly limit how much you can borrow for your new place, or even prevent you from qualifying for a second mortgage at all.

Create a Buffer for the Unexpected

Murphy’s Law loves real estate transactions. If something can go wrong or cost more than expected, it probably will at the most inconvenient moment possible. That’s why having a financial cushion is so important.

Ideally, you want to have some savings set aside beyond what you’ll need for your down payment and closing costs. This buffer can cover unexpected repairs that come up during home inspections, moving expenses that end up being higher than you anticipated, or bridge the gap if you need temporary housing between homes.

How much should you have in reserve? A good rule of thumb is to have at least three to six months of expenses saved up, plus extra for any costs specific to your move.

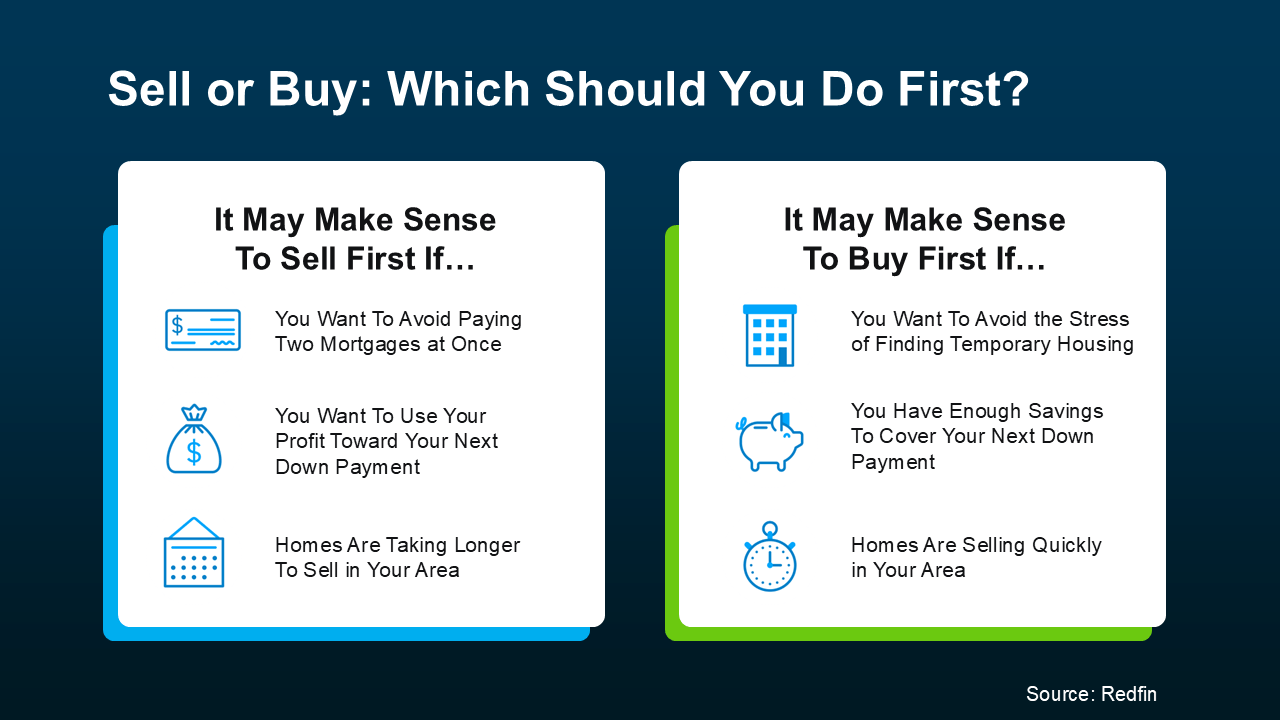

Option One: Selling First, Then Buying

For many people, selling their current home before committing to a new purchase makes the most sense. Let’s break down why this approach works and how to make it happen.

The Major Advantages

When you sell first, you eliminate a ton of financial uncertainty. You know exactly how much money you’re walking away with from the sale. No more wondering “what if we don’t get our asking price?” or “what if the appraisal comes in low?” You have real numbers to work with.

This also means you’re not juggling two mortgage payments, which can be a massive relief for your monthly cash flow. Paying for two homes simultaneously, even for just a few months, can drain your savings faster than you’d expect.

Another huge benefit: you’re a much stronger buyer when you don’t have a home to sell. Sellers love offers from buyers who don’t need to sell their current home first. You’re less risky to them, which means your offers are more likely to be accepted, even in competitive situations.

The Challenges You’ll Face

The biggest downside to selling first is pretty obvious – you need somewhere to live after your sale closes if you haven’t found your next home yet. This can mean moving twice, which nobody enjoys. Moving is consistently ranked as one of life’s most stressful events, and doing it twice in a short period amplifies that stress.

There’s also the storage situation to consider. If you can’t move directly from one home to another, you’ll need somewhere to keep all your stuff. Storage units aren’t free, and depending on how long you need one, those costs can add up quickly.

Additionally, once you’ve sold your home, there can be psychological pressure to find your next place quickly. You don’t want to feel rushed into buying something that’s not quite right just because your lease on a temporary rental is ending.

Strategies to Bridge the Gap

Fortunately, there are several ways to smooth out the transition when you sell first:

Negotiate Your Closing Timeline: If you’ve found your next home and just need a little more time, see if you can push back your sale closing date or move up your purchase closing date to bring them closer together. Many sellers are flexible on timing, especially if it means closing a deal with a strong buyer.

Rent-Back Agreements: This is one of the most elegant solutions. Essentially, you sell your home but negotiate the right to rent it back from the buyers for a short period – usually anywhere from a week to a few months. You pay them rent during this time, which gives you the flexibility to close on your next home without needing temporary housing. Not all buyers will agree to this, but in many markets, it’s a common and reasonable request.

Short-Term Rentals: If a rent-back isn’t possible, look into short-term rentals in your area. This might be a furnished apartment, an Airbnb with a monthly discount, or even an extended-stay hotel. Yes, it’s an extra expense and inconvenience, but it gives you the freedom to take your time finding the right next home.

Crash with Friends or Family: If you have friends or family nearby with extra space, this can be a practical (and budget-friendly) option. Just make sure everyone’s on the same page about expectations and timeline before you show up with your suitcases.

Portable Storage Solutions: Companies that provide portable storage containers can be lifesavers during transitions. They deliver a container to your current home, you load it up, and they store it at their facility until you’re ready for them to deliver it to your new place. This beats having to load and unload a traditional storage unit multiple times.

Option Two: Buying First, Then Selling

On the flip side, some people prefer to secure their next home before putting their current house on the market. This approach has its own set of advantages and challenges.

Why People Choose This Route

The most compelling reason to buy first is certainty about where you’re going. You’ve found the perfect house, negotiated a deal, and know exactly where you’ll be living next. There’s no uncertainty, no backup plans needed, no temporary housing situation to figure out.

You also only have to move once, which saves both money and sanity. You can pack up, move out, and immediately move into your new place. No storage units, no living out of suitcases, no wondering where you packed the coffee maker.

Another advantage: you’re not under pressure to accept a low offer on your current home. If someone comes in with a lowball bid, you can afford to wait for a better offer because you’re not racing against a closing deadline on your purchase.

The Financial Realities

The biggest challenge with buying first is managing two mortgages simultaneously, even if just temporarily. Depending on your financial situation, this might not even be possible. Remember that debt-to-income ratio we talked about? Your existing mortgage counts against you when you’re applying for a new one.

Even if you do qualify for two mortgages, carrying both can be expensive. You’re paying two sets of mortgage payments, property taxes, insurance, utilities, and maintenance costs. If your current home doesn’t sell as quickly as you hoped, those costs can stretch your budget to the breaking point.

There’s also the risk that you’ll feel pressured to accept a lower offer on your current home than you’d like because you need to stop paying that second mortgage. This can cut into the profit you make on the sale.

Financing Options to Make It Work

If you’re set on buying first, here are some financial strategies that can help:

Sale Contingency Offers: When you make an offer on your next home, you can include a contingency that makes the purchase dependent on selling your current home. The seller agrees to give you time to sell before completing the transaction. However, in competitive markets, many sellers won’t accept contingent offers because they’re seen as riskier. This works best in buyer’s markets when sellers have fewer options.

Bridge Loans: These are short-term loans designed specifically for this situation. A bridge loan uses the equity in your current home to fund your down payment on the new house. Once your current home sells, you pay off the bridge loan. The catch? Bridge loans typically come with higher interest rates and fees than traditional mortgages, and you’ll need to qualify for them, which isn’t always easy.

Home Equity Line of Credit (HELOC): Similar to a bridge loan, a HELOC lets you borrow against the equity in your current home. The advantage is that you only pay interest on what you actually use, and HELOCs often have lower rates than bridge loans. The disadvantage is that you’ll need to start making payments immediately, and you’re adding more debt on top of your existing mortgage.

Using Savings or Investments: If you have substantial savings or investments, you might be able to use these for your down payment and then replenish them when your current home sells. Just be careful about tapping into retirement accounts, as you may face penalties and taxes for early withdrawals.

Extended Closing Dates: Sometimes simply negotiating a longer closing period on your new home can give you enough time to get your current house sold. If you’re confident your home will sell quickly, ask for a 60 or 90-day close instead of the standard 30-45 days.

Alternative Approaches

Beyond the traditional sell-first or buy-first scenarios, there are some alternative strategies worth considering:

The Rental Transition

Some people choose to convert their current home into a rental property rather than selling immediately. This can work if you don’t need the equity from your current home to buy the next one, and if you’re interested in becoming a landlord.

The rental income can help offset the cost of your new mortgage, and you might even cash flow positively depending on the numbers. Plus, you maintain the investment value of your property and can sell it later when the market is more favorable.

However, being a landlord isn’t for everyone. It comes with responsibilities, potential headaches, and the reality that you’ll still be on the hook for that mortgage whether or not you have reliable tenants.

Cash Buying Programs

Some companies specialize in buying homes for cash with quick closings. This can be attractive if you’re in a hurry or if your home needs significant repairs that you don’t want to deal with. The trade-off is that these companies typically offer below market value – sometimes significantly below – because they need to make a profit when they resell.

If you’re considering this route, get multiple offers and carefully weigh whether the convenience and speed are worth the lower price you’ll receive.

Trade-In Programs

A newer option in some markets is home trade-in programs offered by companies like Knock, Orchard, or Flyhomes. These companies will essentially buy your current home, allowing you to use that equity to purchase your next place. Once you’ve moved, they sell your old home.

This can be an elegant solution that eliminates timing stress, but these services charge fees for their convenience, and they may not be available in all markets.

Negotiate Like a Pro

Whether you’re buying first or selling first, strong negotiation skills can make a huge difference in your outcomes. Here are some key areas where negotiation matters:

Closing Dates Are Negotiable

Don’t assume that closing dates are set in stone. In fact, they’re one of the most commonly negotiated elements of a real estate transaction. If you need more time or want to move faster, speak up. Many buyers and sellers are willing to be flexible, especially if everything else about the deal is solid.

In some cases, you might even be able to negotiate for both of your closings to happen on the same day or within a few days of each other. This is the ideal scenario because it minimizes the time you’re between homes.

Contingencies Protect You

Contingencies are clauses in your contract that allow you to back out of a deal under specific circumstances without losing your earnest money deposit. The two most relevant for simultaneous transactions are:

Sale Contingency: Makes your purchase dependent on successfully selling your current home. This protects you if your sale falls through, but makes your offer less attractive to sellers.

Settlement or Closing Contingency: Similar to a sale contingency but specifically tied to the closing of your current home. This gives you an escape route if your sale doesn’t close on time.

While contingencies reduce your risk, they can also make your offer less competitive. This is where your agent’s expertise and knowledge of the local market becomes crucial in advising you on the right strategy.

Price Isn’t Everything

Yes, price matters – a lot. But in simultaneous transactions, terms and timing can sometimes be even more important. A slightly lower offer with perfect timing and no contingencies might actually be more valuable to you than a higher offer with complications.

Similarly, when you’re selling, an offer that’s a bit lower but from a buyer who can close on your timeline might be better than a higher offer with uncertainty around timing.

Preparing Your Current Home for Sale

When you’re ready to list your home, taking some time to prepare it properly can pay significant dividends in both how quickly it sells and what price you get.

Start with a Pre-Inspection

Consider paying for a pre-inspection before listing your home. This allows you to identify and address any issues before buyers find them. Fixing problems in advance prevents surprises during the negotiation phase and shows buyers that you’ve taken care of the home.

Even if you don’t fix everything the inspection turns up, at least you know what’s coming and can price accordingly or prepare for negotiation around those items.

The Power of Staging

You’ve probably heard the advice to declutter and depersonalize, and there’s a reason it’s repeated so often – it works. Buyers need to be able to envision themselves living in your space, and that’s hard to do when your family photos cover every surface and your unique decorating style dominates every room.

Professional staging can help your home show better and potentially sell for more. If professional staging isn’t in your budget, at least do some basic staging yourself: remove excess furniture to make rooms look larger, neutralize decor, deep clean everything, and make sure the home is bright and welcoming.

Price It Right from the Start

Pricing strategy is both an art and a science. Your agent will help you analyze comparable sales in your neighborhood to determine a competitive price point. In some hot markets, pricing slightly below market value can actually work in your favor by attracting multiple offers and potentially driving the final price up.

Overpricing, on the other hand, can backfire. Homes that sit on the market too long become stale, and buyers start wondering what’s wrong with them. You might end up selling for less than if you’d priced it correctly initially.

Managing the Logistics

The logistics of moving from one home to another while coordinating two complex transactions can feel overwhelming. Here’s how to stay on top of it all:

Create a Master Timeline

Work with your agent to create a comprehensive timeline that includes all the key dates for both transactions: inspection deadlines, financing contingency removal dates, closing dates, and your actual move date. Having everything laid out visually helps you see where potential conflicts might arise and plan accordingly.

Communicate Constantly

Stay in regular contact with everyone involved in your transactions – your agent, lender, attorney, the other parties’ agents, and anyone else in the mix. Don’t wait for them to reach out to you; be proactive about checking in and making sure everything is on track.

If problems arise, address them immediately rather than hoping they’ll resolve themselves. The earlier you catch issues, the easier they typically are to fix.

Plan Your Move Strategically

If you’re moving directly from one home to another, consider starting to pack non-essential items weeks in advance. Seasonal clothes, books, decorative items, and other things you don’t use daily can be boxed up early, making your actual moving day less chaotic.

For essential items you’ll need right up until moving day and immediately in your new home, pack a separate “first day” box or suitcase. This might include toiletries, a change of clothes, important documents, basic kitchen items, and anything else you can’t live without for 24 hours.

Have Backup Plans Ready

Even with perfect planning, unexpected issues can arise. Your buyer might need to delay closing by a week. Your seller might need to move up the closing date. Inspections might reveal problems that need addressing. Stay flexible and have backup plans ready for common scenarios.

The Emotional Side

Let’s acknowledge something that doesn’t get talked about enough: buying and selling at the same time is emotionally intense, even when everything goes smoothly. You’re leaving a home that likely holds years of memories while simultaneously trying to get excited about your next chapter. You’re spending large amounts of money while also hoping to receive large amounts of money. The stress is real.

Give yourself permission to feel overwhelmed sometimes. This is a big deal, and it’s okay if you’re not in perfect zen mode throughout the entire process. Take breaks from house hunting or listing prep when you need them. Lean on your support system – friends, family, or even a therapist if the stress is getting to be too much.

Remember that this is temporary. You will get through it, and you’ll end up in your new home wondering why you were so stressed. But while you’re in the thick of it, be kind to yourself.

Making Your Decision

So which approach should you choose – selling first or buying first? Honestly, there’s no one-size-fits-all answer. The right choice depends on your specific circumstances:

Your financial situation is probably the biggest factor. If you absolutely need the equity from your current home to make your next purchase, selling first is likely your only realistic option. If you have substantial savings or can qualify for two mortgages, buying first becomes more feasible.

Your local market conditions matter too. In a hot seller’s market where homes fly off the shelves, selling first might make more sense because you can be confident your home will move quickly. In a buyer’s market where homes sit longer, you might want to secure your next place first.

Your personal risk tolerance is also relevant. Some people handle uncertainty better than others. If the idea of not knowing where you’ll live after your sale closes gives you panic attacks, buying first might be worth the extra financial complexity.

Wrapping It All Up

Buying and selling a home simultaneously is undoubtedly complex, but it’s far from impossible. Thousands of people successfully navigate this process every year, and with proper planning, professional guidance, and realistic expectations, you can too.

The keys to success are: understanding your local market, building a strong team of professionals to guide you, getting your finances in order before you start, carefully weighing the pros and cons of selling first versus buying first, staying flexible when unexpected issues arise, and communicating constantly with everyone involved.

Most importantly, remember that while the process might be stressful, you’re working toward an exciting goal – your next home. Keep that vision in mind when things get tough, trust the professionals you’ve hired to guide you, and know that before long, you’ll be settling into your new place and this whole complicated dance will be nothing but a memory.

The journey from one home to the next doesn’t have to be a nightmare. With the right preparation and approach, it can actually be a rewarding experience that sets you up for success in your next chapter. So take a deep breath, make a plan, and take that first step. You’ve got this.