(Updated 9/26/25)

Stuck in the rent-or-buy debate? You’re definitely not alone. With mortgage rates still higher than we’d like and home prices that make your head spin, renting might seem like the safe play right now. But here’s what most people don’t realize: that “safe” choice could actually be costing you big time in the long run.

Homeowner Wealth vs. Renter Wealth

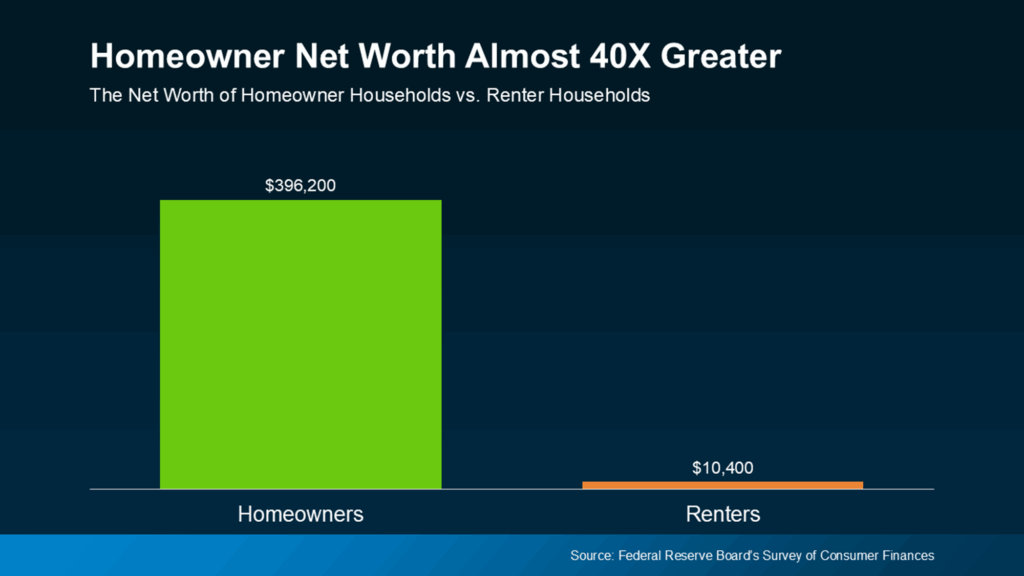

Let’s start with some numbers that might blow your mind. According to the Federal Reserve’s latest Survey of Consumer Finances, the average homeowner’s net worth is nearly 40 times higher than a renter’s.

We’re talking about a homeowner’s average net worth of around $396,200 compared to a renter’s $10,400. That’s not a typo – it’s a massive gap that keeps getting wider.

The wealth gap between homeowners and renters has grown significantly over recent years

But why is this gap so huge? The answer comes down to one powerful word: equity.

What’s Behind the Homeowner Wealth Explosion?

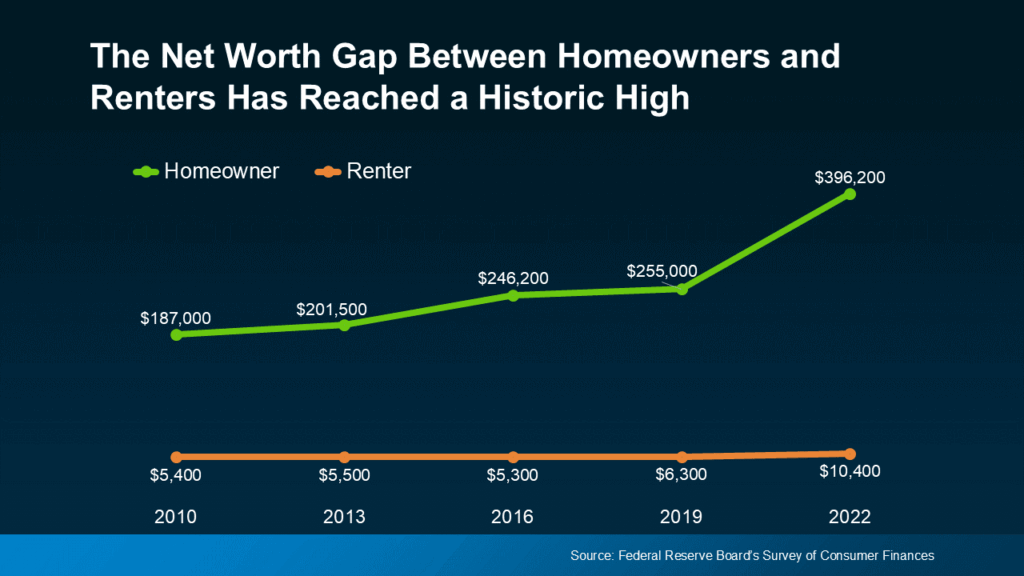

The Federal Reserve found that the 2019-2022 period saw “the largest three-year increase in median net worth over the history of the modern survey.” And guess what drove most of that growth? Home equity.

Both homeowner and renter wealth have grown, but homeowners have seen dramatically larger gains

Here’s how it works: Every month when you pay your mortgage, you’re building equity (the difference between what your home is worth and what you owe). Plus, when home values go up – which they typically do over time – your equity grows even faster.

As Ksenia Potapov from First American puts it: “Despite the risk of volatility in the housing market, homeownership remains an important driver of wealth accumulation and the largest source of total wealth among most households.”

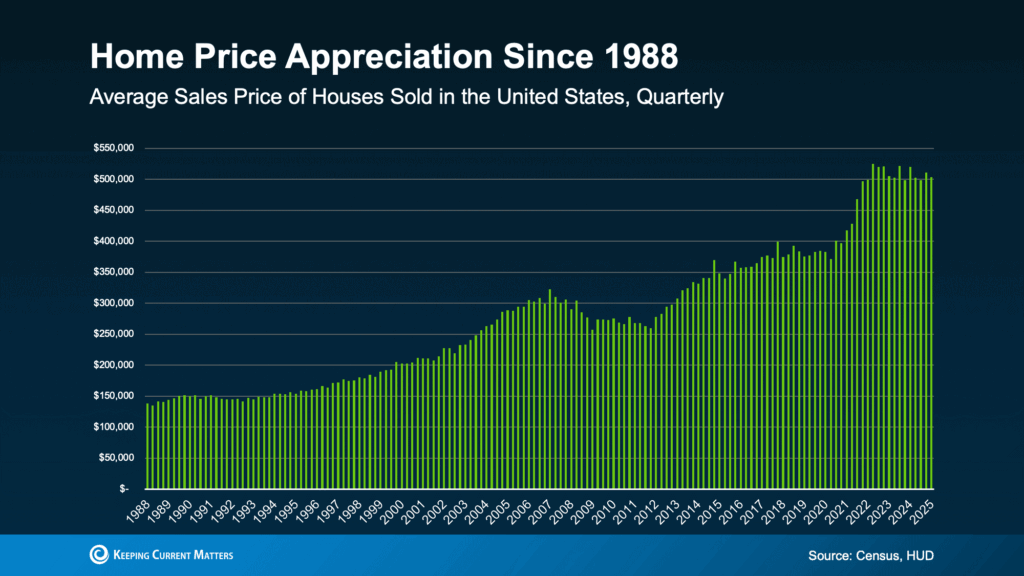

Reason #1: Home Values Almost Always Go Up Over Time

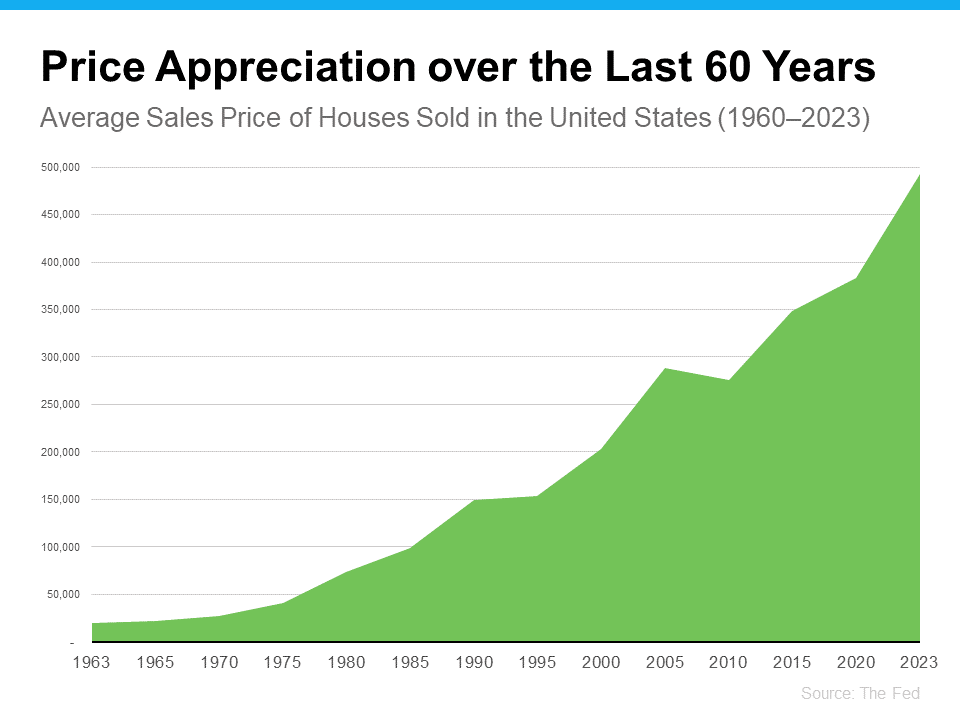

One of the biggest myths floating around is that home prices are unpredictable. But when you look at the long-term data, there’s actually a pretty clear pattern.

60 years of Federal Reserve data shows home prices have climbed steadily, with only rare exceptions

Using 60 years of Federal Reserve data, you can see that home prices have been on an upward climb for decades. Yes, there was that rough patch during the 2008 housing crash, but even that was more of a blip in the bigger picture.

This steady appreciation is exactly why homeownership beats renting for wealth building. As the Urban Institute notes: “Homeownership is critical for wealth building and financial stability.”

Reason #2: Rent Never Stops Going Up (But Your Mortgage Can Stay Fixed)

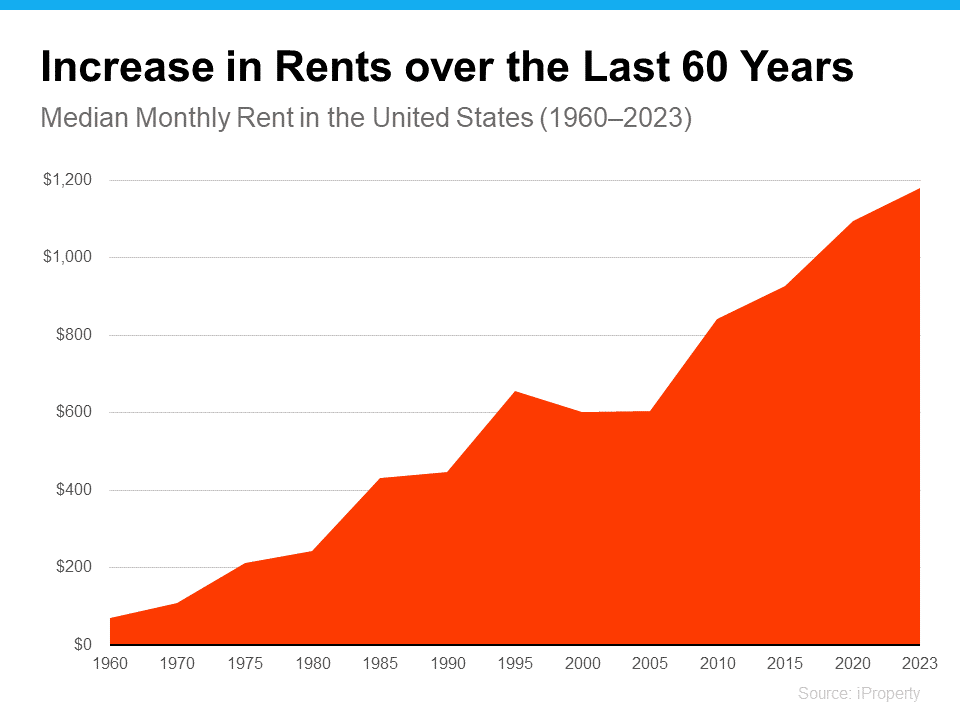

Here’s something that might hit close to home if you’re a renter: that sinking feeling when your lease renewal notice shows up with a higher monthly payment. It’s not your imagination – rent really does keep climbing year after year.

60 years of rent data shows the consistent upward trend that never seems to stop

This chart from iProperty Management shows rent has been rising pretty consistently for 60 years. And while recent years have seen some moderation, the overall trend is clear: rent goes up, and up, and up.

But here’s the beautiful thing about homeownership: when you get a fixed-rate mortgage, your principal and interest payment stays the same for the entire life of your loan. While your renting friends are dealing with annual rent increases, you’re sitting pretty with predictable housing costs.

Your housing payments are like an investment – the question is, do you want to invest in yourself or keep padding your landlord’s pockets?

When Buying Makes More Financial Sense Than Renting

You might be surprised to learn that in many situations, buying is actually more affordable than renting – especially if you need some space to spread out.

National data shows buying typically costs less than renting when you need two or more bedrooms

This comparison using national data from Realtor.com and the National Association of Realtors reveals something interesting: if you’re looking for two or more bedrooms, homeownership is typically more affordable than renting.

So if you’re planning to start a family, need a home office, or just want room for all your stuff without feeling cramped, buying might actually save you money from day one.

The Long-Term Wealth Building Power of Homeownership

Let’s zoom out and look at the bigger picture. While rent money disappears forever once you pay it, every mortgage payment builds your equity – and that equity becomes part of your net worth.

Decades of data show the long-term upward trend in home values

This long-term price appreciation, combined with paying down your mortgage balance, creates a powerful wealth-building machine. According to Zonda research, the top reason millennial homeowners bought their homes was to build their own equity instead of someone else’s.

Smart move, millennials.

The stark difference in net worth between homeowners and renters tells the whole story

Forbes puts it perfectly: “While renting might seem like the less stressful option… owning a home is still a cornerstone of the American dream and a proven strategy for building long-term wealth.”

The Cost of Staying in the Rental Trap

A recent Bank of America survey found that 70% of aspiring homeowners worry about what long-term renting means for their future. And honestly? They should be worried.

Census data shows how rent increases have outpaced many other expenses over the decades

Here’s the thing about rent: it’s not just money going out the door every month. Those increases make it harder and harder to save up for a down payment. Meanwhile, the homes you’re hoping to buy someday? They’re getting more expensive too.

In that same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances. That’s a lot of people losing sleep over something that homeownership could solve.

It’s Not Just About Money – It’s About Living Life on Your Terms

Sure, we’ve been talking a lot about dollars and cents, but homeownership offers benefits you can’t put a price tag on. As the experts at 1000WATT point out: “Homeownership isn’t primarily financial anymore… Across all demographics, emotional and lifestyle factors consistently outrank wealth-building as motivators.”

Freedom to Make It Yours

Want to paint your bedroom walls deep blue? Go for it. Ready to hang that gallery wall you’ve been planning? No permission needed. When you own your home, you have the freedom to create a space that actually reflects who you are.

Pro tip: If you’re buying in a community with a homeowner’s association (HOA), just check what approvals you might need for exterior changes.

Privacy and Peace of Mind

There’s something special about knowing this place is truly yours. No surprise inspections from landlords, no worrying about lease renewals, just the peaceful feeling of being home.

Room to Grow

Whether you’re planning to start a family, launch a side business from home, or finally set up that home gym, owning gives you the space to live life exactly how you want.

Putting Down Real Roots

When you own, you’re not just passing through – you’re part of the community. That often means stronger neighborhood connections and a deeper sense of belonging.

The Pride of Achievement

There’s nothing quite like getting those keys and walking through your own front door for the first time. It’s more than pride – it’s that quiet satisfaction of knowing “I did this.”

Is Now Really the Right Time?

Look, we’re not going to sugarcoat this. The housing market today isn’t exactly easy for first-time buyers. It takes patience, strategy, and sometimes some creative problem-solving.

But as Realtor.com says: “Buying a home is a major commitment, but it’s also incredibly rewarding.”

Here’s what you need to consider: You should only buy a home when you’re ready and able to do it, and if the timing is right for you. But if you can make the numbers work, the long-term benefits are hard to ignore.

Dr. Jessica Lautz from the National Association of Realtors puts it this way: “If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Making the Decision: Rent vs. Buy

Joel Berner, Senior Economist at Realtor.com, sums up the trade-off perfectly:

“Households working on their budget will find it much easier to continue to rent than to go through the expenses of homeownership. However, they need to consider the equity and generational wealth they can build up by owning a home that they can’t by renting it. In the long run, buying a home may be a better investment even if the short-run costs seem prohibitive.”

The key question isn’t just “Can I afford the monthly payment?” It’s “Can I afford to keep paying someone else’s mortgage instead of my own?”

Getting Out of the Rental Cycle

Key factors to consider when making your rent vs. buy decision

If homeownership feels out of reach right now, you’re definitely not alone. But the first step toward building real wealth through homeownership is creating a solid plan.

Here’s what Bankrate recommends: “Deciding between renting and buying a home isn’t just about cost – the decision also involves long-term financial strategies and personal circumstances. If you’re on the fence about which is right for you, it may be helpful to speak with a local real estate agent who knows your market well.”

Your Financial Future Depends on This Decision

Renting might feel safer today, and in some areas, it might even cost less month-to-month. But over time, it could end up costing you way more – without building anything for your future.

Meanwhile, homeownership with a fixed-rate mortgage can:

- Lock in your monthly housing costs for decades

- Build equity with every payment

- Grow your net worth as home values appreciate

- Give you the freedom to live life on your terms

- Provide stability in an uncertain world

The numbers don’t lie: homeowners have nearly 40 times the net worth of renters. That’s not a coincidence – it’s the power of building equity instead of building someone else’s wealth.

Ready to Stop Paying Someone Else’s Mortgage?

Whether you’re ready to buy now or need to create a plan for the future, the most important step is getting expert guidance. A local real estate agent can help you understand your market, explore your options, and figure out the best strategy for your situation.

They can also connect you with lenders who offer programs that might make homeownership more accessible than you think.

What would it mean for you to finally have a place to call your own?

The rental trap is real, but it doesn’t have to be permanent. With the right plan and expert help, that dream of homeownership – and all the financial benefits that come with it – might be closer than you think.

Ready to explore your options? Connect with a trusted local real estate agent today and start building your wealth instead of your landlord’s.