(Updated 11/11/25)

If you’ve been house hunting lately, you know how frustrating it can be. You find a place you love, submit an offer, and then—someone else gets it. Maybe you’ve heard the rumors swirling around social media and news sites about big Wall Street firms swooping in with cash offers, buying up entire neighborhoods, and leaving regular folks like you and me with nothing. It’s easy to feel defeated before you even start, right?

But here’s some good news that might surprise you: the whole “Wall Street is buying everything” narrative? It’s mostly not true. Yes, there are investors in the housing market, but the reality is way different from what those viral headlines would have you believe. Let’s dig into what’s actually happening out there, because understanding the truth might just give you the confidence boost you need to jump back into your home search.

The Numbers Tell a Different Story

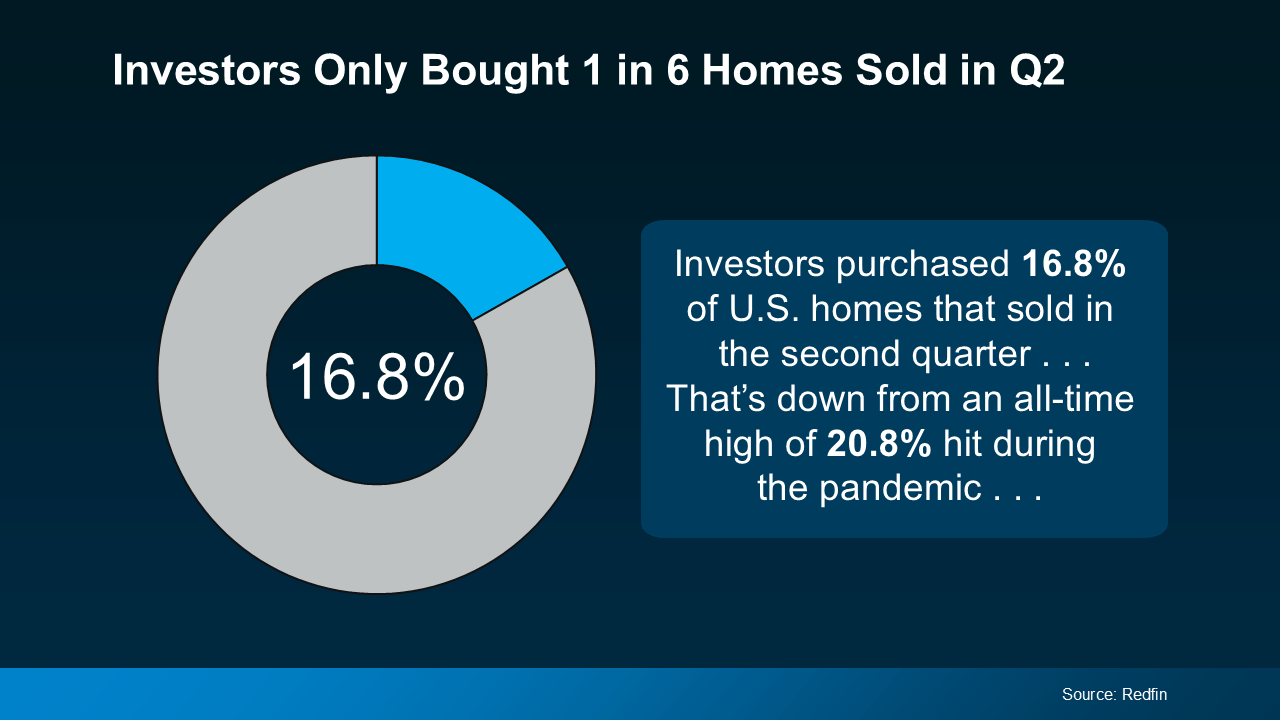

When you’re scrolling through your social media feed and you see another post claiming that hedge funds own half the housing market, it’s natural to feel discouraged. But data from reliable sources like Redfin paints a completely different picture. Investors of all types—from massive corporations to your neighbor who owns a rental property—purchase roughly one out of every six homes sold in America.

Think about that for a second. That means five out of every six homes are going to regular homebuyers. People just like you who are looking for a place to call their own, raise their families, or start their next chapter. The competition you’re facing isn’t coming from some faceless Wall Street giant—it’s probably coming from other families who are in the exact same boat as you.

This isn’t to say the market isn’t competitive. It absolutely is, especially in desirable neighborhoods and growing cities. But knowing that most of your competition consists of other regular people rather than billion-dollar investment firms should help you feel less like you’re David going up against Goliath.

Who Are These Investors Anyway?

When we talk about investors in the housing market, most people immediately picture massive corporations with unlimited budgets and armies of real estate agents. That image has been reinforced by countless articles and social media posts. But the reality is much more down-to-earth and, frankly, more relatable.

According to research from CoreLogic, the vast majority of property investors are what we call “mom-and-pop” investors. These are everyday people who own fewer than ten properties. Maybe it’s your coworker who kept their starter home when they moved and now rents it out. Perhaps it’s a retired couple who bought a vacation home at the beach and lists it on rental sites when they’re not using it. It could even be someone in your own family who saw real estate as a smart way to build wealth for retirement.

These small investors aren’t the enemy. They’re not using sophisticated algorithms to identify undervalued properties or making all-cash offers sight unseen. They’re regular people who believe in homeownership and see rental properties as a way to generate income or build their financial future. In many ways, they’re proof that homeownership in America is still a viable path to building wealth.

Now, what about those mega-investors with thousands of properties? They do exist, but they represent only about one percent of the market. One percent! That’s a tiny slice of the pie. So while companies like Invitation Homes and American Homes 4 Rent do own substantial portfolios, their overall impact on your ability to buy a home is much smaller than you’ve probably been led to believe.

The Investor Trend Is Declining

Here’s another piece of good news that doesn’t get nearly enough attention. Investor activity in the housing market has been steadily decreasing over the past few years. We’re not just talking about a slight dip—we’re talking about a significant decline that shows no signs of reversing anytime soon.

CoreLogic’s data shows that investors made about eighty thousand home purchases in June of last year, compared to over one hundred thousand purchases the year before. If you go back to the peak in June of 2021, investors were buying nearly one hundred fifty thousand homes. That’s almost a fifty percent drop from the peak to now. The trend line is clearly pointing downward, and analysts expect this decline to continue through this year and beyond.

Why is this happening? Several factors are at play. Rising interest rates have made it more expensive for investors to finance purchases, especially smaller investors who rely on mortgages rather than all-cash offers. The narrowing profit margins in many markets mean that rental income doesn’t always justify the purchase price anymore. And increased competition from regular homebuyers—yes, you!—means investors can’t always win bidding wars like they used to.

This cooling of investor activity is creating more opportunities for primary homebuyers. Those homes that might have gone to an investor a few years ago are increasingly available for families looking to buy. The playing field is leveling out, slowly but surely.

Investor Categories

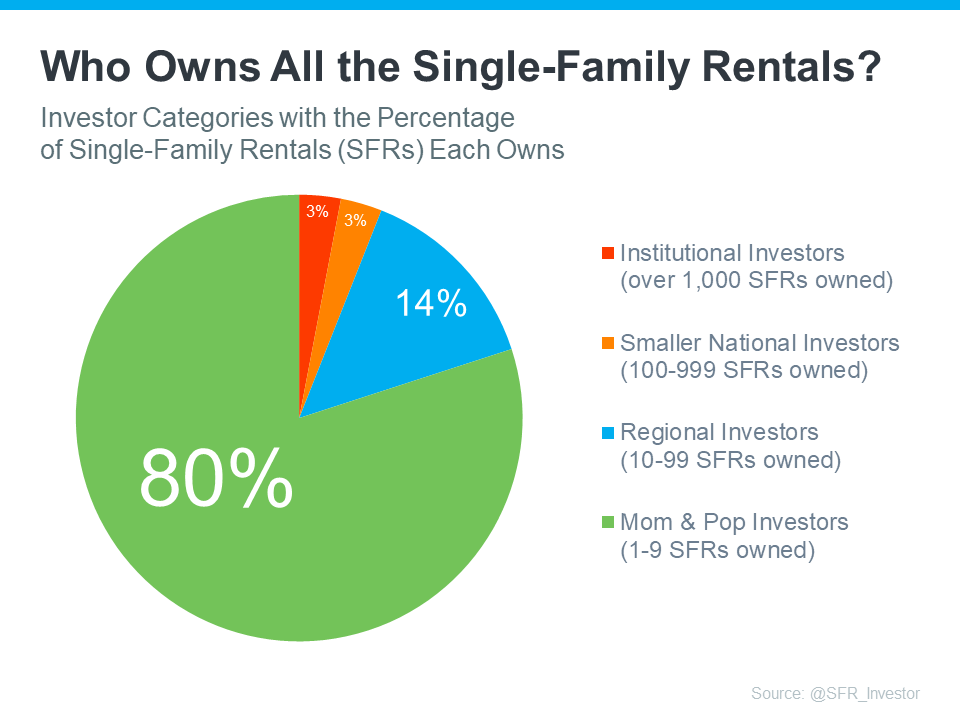

To really understand the investor landscape, it helps to break down the different types of investors and what percentage of rental properties each group owns. When you see the actual numbers, the picture becomes even clearer.

At the bottom tier, we have mom-and-pop investors who own between one and nine single-family rentals. This group owns the overwhelming majority of rental homes in America. These are the small-time landlords who might have inherited a property, decided to keep their first home when they upgraded, or intentionally purchased one or two rental properties as part of their investment strategy.

Moving up, there are regional investors who own between ten and ninety-nine properties. This group often consists of small property management companies or individuals who’ve made real estate investing their primary business. They’re more professional than mom-and-pop investors but still operate on a relatively small scale compared to what most people imagine when they think of corporate landlords.

Then we have smaller national investors with portfolios of one hundred to nine hundred ninety-nine homes. These companies operate across multiple markets but still represent a fairly small portion of the overall rental market.

Finally, at the top, we have institutional investors—the ones that get all the attention—who own more than one thousand properties. Despite all the headlines and social media fury directed at this group, they own the smallest percentage of rental homes. We’re talking about single-digit percentages at most, even though they receive ninety percent of the blame for housing market challenges.

Viral Myths

Remember when a claim went viral saying Wall Street investors bought forty-four percent of all homes in 2023? That story spread like wildfire across social media, got shared by news outlets, and even prompted some lawmakers to introduce legislation. There was just one problem: it was completely false.

The actual data from organizations like Freddie Mac and John Burns Real Estate shows that institutional homebuyers—those who purchased one hundred or more homes in a twelve-month period—never even reached two and a half percent market share at their peak. Not forty-four percent. Not even four percent. At the peak, it was less than five percent, and current figures show it’s now roughly half that amount.

So where did that forty-four percent claim come from? It appears to have originated from a misunderstanding or misrepresentation of data in an article that then got amplified through the social media echo chamber. Once something goes viral, it’s incredibly hard to correct, even when the actual numbers are readily available and clearly show something entirely different.

The confusion often stems from lumping all investors together. When you include every single investor from the person with one rental property to massive corporations with thousands, the overall investor share of home purchases does reach around thirty percent in some markets. But the vast, vast majority of that thirty percent consists of small investors, not Wall Street firms.

What About Blackstone and BlackRock?

These two names come up constantly in discussions about corporate homeownership, often used interchangeably even though they’re different companies. Let’s clear up some of the confusion and look at what these firms are actually doing.

Blackstone—not BlackRock—is one of the largest private equity firms in the world and does own a substantial number of residential properties through various investment vehicles. They own hundreds of thousands of residential units, making them one of the largest corporate landlords globally. That’s real, and it’s legitimate to discuss the implications of such concentrated ownership.

However, even with their massive portfolio, Blackstone’s holdings represent a tiny fraction of the total housing market in America. When you consider that there are roughly eighty-two million single-family homes in the United States, and sixty-eight million of those are owner-occupied, Blackstone’s few hundred thousand units represent less than three percent of even just the rental market.

The impact also varies dramatically by location. In some cities like Atlanta, corporate landlords including Blackstone-related entities own a much larger share of rental properties—sometimes over twenty percent in certain neighborhoods. This concentrated ownership in specific markets can absolutely create real problems for residents in those areas, including rapidly rising rents and decreased housing stability.

But nationally? The narrative that Blackstone or any other single firm is buying up everything and pricing out regular homebuyers simply doesn’t match the data. It makes for compelling headlines and gets lots of shares on social media, but it’s not an accurate representation of what’s happening across the country.

The Real Competition

So if it’s not Wall Street firms, who are you actually competing against when you’re trying to buy a home? The answer might surprise you—or maybe it’ll confirm what you’ve suspected all along.

You’re competing against other people who want the same thing you do. Young families looking for their first home with enough space for kids. Millennials who’ve been saving for years and are finally ready to stop renting. Gen Xers who are upgrading to accommodate aging parents or grown children moving back home. Baby boomers who are downsizing from larger family homes or relocating to be closer to grandchildren.

The challenge in today’s market isn’t that Wall Street is buying everything. The challenge is that there simply aren’t enough homes available for the number of people who want to buy. Years of underbuilding following the 2008 financial crisis created a supply deficit that we’re still working through today. Add to that the fact that many existing homeowners are reluctant to sell because they have historically low mortgage rates they don’t want to give up, and you have a recipe for intense competition among regular buyers.

This is actually somewhat encouraging news, believe it or not. When your competition consists of other families and individuals, you’re all playing by the same basic rules. You’re all dealing with mortgage pre-approvals, home inspections, and financing contingencies. You’re all balancing budgets and making tough decisions about how much to offer. Nobody has an unfair advantage that makes it impossible for you to compete.

Mortgage Data

Here’s another way to understand what’s really happening in the housing market. Wall Street firms typically buy homes with cash because they have the capital to do so and it makes their offers more attractive to sellers. Individual homebuyers, on the other hand, usually need mortgages.

When we look at mortgage application data, we see something interesting. Despite all the noise about institutional investors, mortgage purchase applications continue to show year-over-year improvement. Every time mortgage rates dip closer to six percent, there’s a surge of eager buyers jumping into the market. This activity is driven by primary residence buyers—people who plan to live in the homes they’re purchasing, not rent them out.

The latest data on pending contracts also shows positive trends. These are early indicators of home sales that will close in the next month or two, and they consistently point to healthy demand from individual homebuyers. If Wall Street were really dominating the market, we wouldn’t see this kind of sustained mortgage demand. The growth is coming from regular people like you who are working with lenders, getting pre-approved, and making offers on homes.

This mortgage data essentially proves that the primary driver of housing market activity is individual homebuyers, not cash-wielding investment firms. The American dream of homeownership is still very much alive and being pursued by millions of people across the country.

Regional Variations

While the national picture shows that institutional investors are a small part of the overall market, it’s important to acknowledge that some cities and regions have been more heavily impacted than others. Atlanta is often cited as an example, with some studies showing that corporate landlords own a significant percentage of rental homes in certain neighborhoods.

In some Atlanta neighborhoods, corporate ownership of single-family rental homes can reach extremely high levels. This concentrated ownership can create real challenges for residents, including rapid rent increases, less responsive property management, and a general sense that neighborhoods are changing in ways that don’t benefit longtime residents.

Phoenix, Las Vegas, and parts of Florida have also seen higher-than-average institutional investor activity. These markets tend to have characteristics that attract large investors: strong rental demand, relatively affordable home prices, and favorable landlord-tenant laws.

But even in these hotspot markets, the overall percentage of homes owned by large institutional investors remains in the single digits or low double digits when looking at the entire metropolitan area. The impact is often felt more intensely in specific neighborhoods or suburbs rather than uniformly across the region.

If you’re house hunting in one of these areas with higher institutional ownership, it’s worth working with a local real estate agent who understands the nuances of your specific market. They can help you identify neighborhoods where you’re less likely to be competing with investors and more likely to be making offers against other families.

The Legislative Response

The perception that Wall Street is buying up all the homes has prompted lawmakers at both the federal and state levels to introduce various bills aimed at limiting corporate ownership of single-family homes. Some proposals would cap the number of homes any single company can own. Others would impose heavy taxes on institutional investors to discourage them from entering the market. A few would even require large investors to sell off portions of their portfolios to individual buyers.

While these legislative efforts show that politicians are responding to constituent concerns about housing affordability, very few of these bills have advanced beyond the proposal stage. In most cases, they haven’t even reached a floor vote in their respective legislatures.

There are several reasons for this. First, the actual data on institutional ownership makes it hard to justify aggressive legislative action when these companies own such a small percentage of homes. Second, the single-family rental industry has argued that they provide valuable housing options for people who can’t or don’t want to buy, and that limiting their operations could actually reduce housing options rather than expand them. Third, many economists and housing experts argue that the real problem is insufficient housing supply, and that focusing on investors distracts from the more fundamental issue of building more homes.

Regardless of where you stand on these legislative proposals, their mere existence highlights how much attention the issue of corporate homeownership has received, even if the actual scope of the problem doesn’t match the public perception.

What This Means for Your Home Search

Okay, so we’ve established that Wall Street isn’t actually buying up all the homes. How does this information help you in your actual home search? Here are some practical takeaways.

First, don’t let the myth of overwhelming investor competition discourage you from even trying. The odds are much more in your favor than you probably thought. Five out of six homes are going to regular buyers, which means you absolutely have a realistic chance of finding and buying a home.

Second, focus your energy on the things that actually matter in a competitive market. Get pre-approved for a mortgage so you can move quickly when you find the right home. Work with an experienced real estate agent who knows your local market and can help you craft competitive offers. Be prepared to act fast, but also be patient—the right home at the right price will come along.

Third, remember that your main competition is other families and individuals who have the same constraints you do. They need mortgage approval, they have budget limits, and they’re dealing with the same tight inventory you are. You’re not up against entities with unlimited resources and insider advantages.

Finally, stay informed about what’s actually happening in your local market. National trends are interesting, but real estate is ultimately local. What’s true for the country as a whole might not reflect what’s happening in your specific city or neighborhood. Your real estate agent can provide insights into investor activity in your target areas and help you strategize accordingly.

Housing Affordability

While it’s important to debunk the myth that Wall Street is buying everything, it’s equally important to acknowledge that housing affordability is a real and serious issue facing millions of Americans. Home prices have risen dramatically over the past decade, wages haven’t kept pace, and many people are finding it harder to achieve homeownership than their parents did.

But blaming institutional investors for this problem misses the mark. The fundamental issue is that we haven’t built enough housing to meet demand. Zoning restrictions, construction costs, labor shortages, and lengthy approval processes have all contributed to an undersupply of homes across the country.

When demand exceeds supply, prices rise. It’s basic economics. Institutional investors are a symptom of the housing affordability problem, not the primary cause. They buy homes because it’s profitable to do so in markets where rents are high relative to purchase prices—but the underlying reason rents are high is because there aren’t enough homes for everyone who needs one.

Solving the housing affordability crisis will require building more homes of all types, streamlining approval processes, investing in infrastructure to support new development, and potentially rethinking some of our zoning laws that restrict housing density. These are complex, long-term challenges that don’t lend themselves to viral social media posts, but they’re the real issues we need to address.

Moving Forward

The narrative that Wall Street is buying up all the homes makes for compelling content on social media and generates lots of clicks for news sites. It taps into legitimate anxieties about housing affordability and economic inequality. But it’s simply not supported by the data.

Most investors are small mom-and-pop landlords, not massive corporations. Overall investor activity is declining, not increasing. And the vast majority of homes are still being purchased by individual homebuyers who plan to live in them. Yes, housing is expensive and the market is competitive, but you’re competing against other people, not against an army of Wall Street firms with unlimited budgets.

Understanding the reality of the situation should be empowering. You’re not fighting an impossible battle. You’re navigating a challenging market, sure, but one where regular people like you are successfully buying homes every single day. Those five out of six homes going to non-investors? Each one represents someone who pushed through the challenges, stayed focused, and achieved their goal of homeownership.

If you’re in the market for a home, don’t let myths and misconceptions derail your search before you even begin. Connect with a knowledgeable real estate agent who can give you accurate information about your local market. Get your finances in order and obtain a mortgage pre-approval. Start looking at homes and making offers. Yes, you might face some rejection along the way—that’s normal in any competitive market. But you absolutely can succeed.

The dream of homeownership in America isn’t dead, and it hasn’t been stolen by Wall Street. It’s alive and well, being pursued and achieved by hundreds of thousands of regular people every year. There’s no reason you can’t be one of them. Take this more accurate understanding of the market, use it to fuel your confidence, and go find the home that’s right for you. It’s out there waiting, and now you know that the competition for it is much more manageable than you thought.