(Updated 10/14/25)

Let’s talk about something that’s probably been on your mind if you’ve been thinking about buying or selling a home lately: mortgage rates. They’re everywhere in the news, and honestly, it can feel a bit overwhelming trying to figure out what’s actually happening and what it means for you.

Here’s the thing – we’ve all been watching and waiting, hoping rates would drop back down to those incredible lows we saw a few years ago. But the reality is a bit more nuanced than that, and understanding where things actually stand can help you make smarter decisions about your housing plans.

Current Mortgage Rates

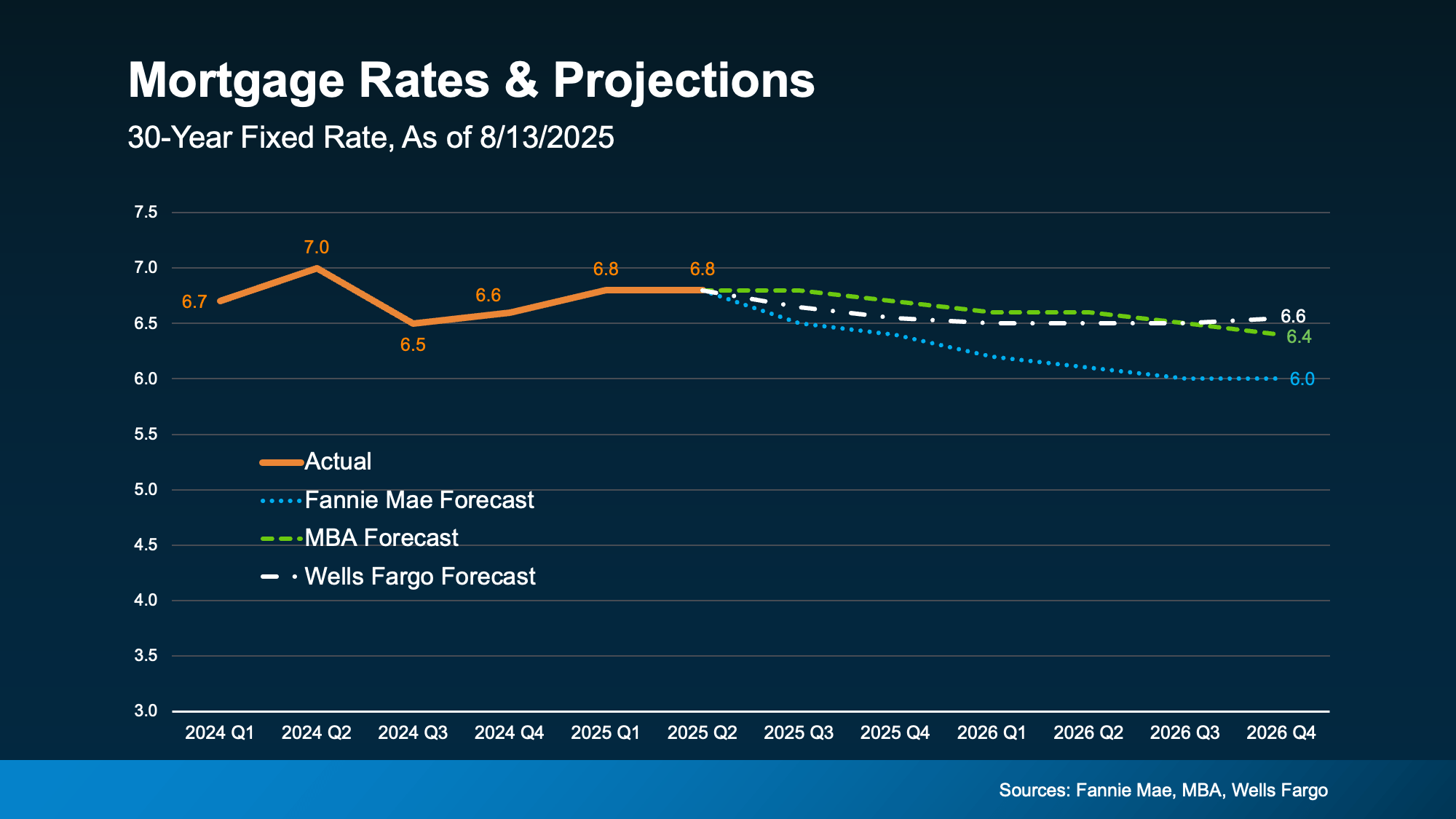

So where are we right now? After that surprisingly weak jobs report came out earlier this year, something interesting happened. The bond market responded almost immediately, and mortgage rates dipped to their lowest point of the year at around 6.55%. Now, you might be thinking, “That doesn’t sound particularly low,” and you’re not wrong. But here’s why it matters.

Every single buyer out there has been holding their breath, waiting for rates to come down. Even a small decrease like this one gives people hope that maybe, just maybe, we’re finally seeing the beginning of a downward trend. It’s like watching the first signs of spring after a long winter – you want to believe warmer days are ahead.

The challenge is figuring out what’s realistic to expect moving forward. According to the latest projections from industry experts, we’re not looking at any dramatic drops anytime soon. Most forecasters are predicting rates will hover somewhere in the mid-to-low 6% range through 2026. That’s not the news everyone wants to hear, but it’s important to set realistic expectations.

Small Shifts Are Still Meaningful

Even though we’re not seeing massive changes, those smaller movements in rates are still worth paying attention to. Every time new economic data comes out – whether it’s employment numbers, inflation reports, or updates from the Federal Reserve – there’s potential for mortgage rates to react.

Think of it like the stock market, but for home loans. The economy is constantly in motion, and mortgage rates move along with it. Some weeks we’ll see rates tick down a bit, other weeks they creep back up. It’s this constant dance that makes trying to perfectly time your home purchase nearly impossible.

The Magic Number

There’s one number that seems to be on every potential buyer’s radar: 6%. It’s not just some arbitrary figure people picked out of thin air, either. There’s real data backing up why this matters so much.

According to recent research from the National Association of Realtors, if mortgage rates hit that 6% mark, something significant would happen. Suddenly, about 5.5 million more households would be able to afford the median-priced home. That’s huge. And within just 12 to 18 months of rates hitting 6%, roughly 550,000 people would pull the trigger on buying a home.

That’s a massive amount of pent-up demand just sitting on the sidelines, waiting for the right moment to jump in. And looking at current projections, there’s a good chance we’ll see rates hit that threshold sometime next year. Which brings us to an important question you need to ask yourself.

Should You Wait for Lower Rates?

This is where things get really interesting, and honestly, where a lot of people are struggling with their decision right now. On one hand, waiting for lower rates makes perfect sense. Why wouldn’t you want a better deal? But there’s a significant tradeoff you need to consider.

If you’re waiting for rates to hit 6%, you need to realize something crucial: everyone else is waiting for that too. When rates finally do continue their downward trend and all those buyers who’ve been sitting on the sidelines decide to jump back in at the same time, you’re going to face some serious challenges.

More competition means you’ll be making offers against multiple other buyers. Fewer choices because homes will be snapped up faster. And here’s the kicker – higher home prices, because when demand surges, prices follow. It’s basic economics, and it’s exactly what we’ve seen happen in hot markets before.

Opportunity Right Now

Let me paint a picture of what’s happening in today’s market, because there are some real advantages that exist right this moment that might disappear if you wait too long.

First, inventory is up. There are more homes on the market than we’ve seen in quite a while. For buyers, this means actual choices. You’re not limited to just two or three properties in your price range and desired neighborhood. You can be selective, take your time, and find something that really fits what you’re looking for.

Second, price growth has slowed down considerably. We’re not seeing those crazy bidding wars where homes sell for 20% over asking price anymore. Pricing has become more realistic, more grounded in actual value rather than fear-driven panic buying.

Third, and this is big – you actually have negotiating power right now. Sellers are more willing to work with buyers, whether that means price reductions, covering closing costs, or making repairs. In a hot market when rates drop and everyone rushes back in, that negotiating power evaporates almost overnight.

These are genuine opportunities that will disappear if rates fall and demand surges. You might be missing a key opening in the market by waiting for that perfect rate that may or may not materialize when you think it will.

The 3% Reality Check

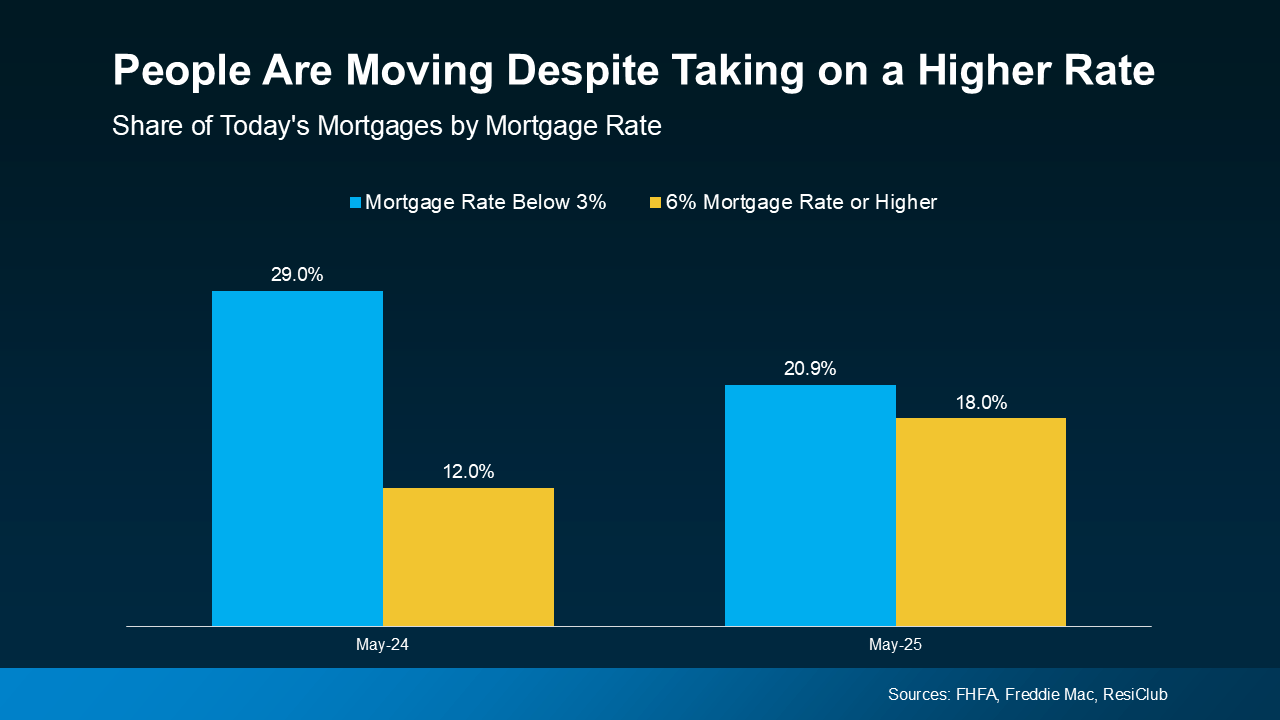

Let’s address the elephant in the room. A lot of homeowners are holding onto their current homes with those beautiful 3% mortgage rates from 2020 and 2021, and honestly, who can blame them? It’s incredibly hard to let go of a deal that good.

Those ultra-low rates are the main reason so many people have delayed moving in recent years. But here’s something worth considering: while your low rate might be ideal financially, it doesn’t make up for other real-life needs that matter just as much, if not more.

Maybe you’re cramped and need more space for a growing family. Maybe you’re dealing with a staircase your knees can’t handle anymore. Maybe you’re living a thousand miles away from family members you want or need to be closer to. These aren’t small issues – they’re quality of life concerns that impact your daily happiness.

The data shows that the share of homeowners with mortgage rates below 3% is steadily dropping as more people make the decision to move despite today’s higher rates. At the same time, the percentage of homeowners taking on rates above 6% is rising. People are making moves because life doesn’t wait for perfect financial conditions.

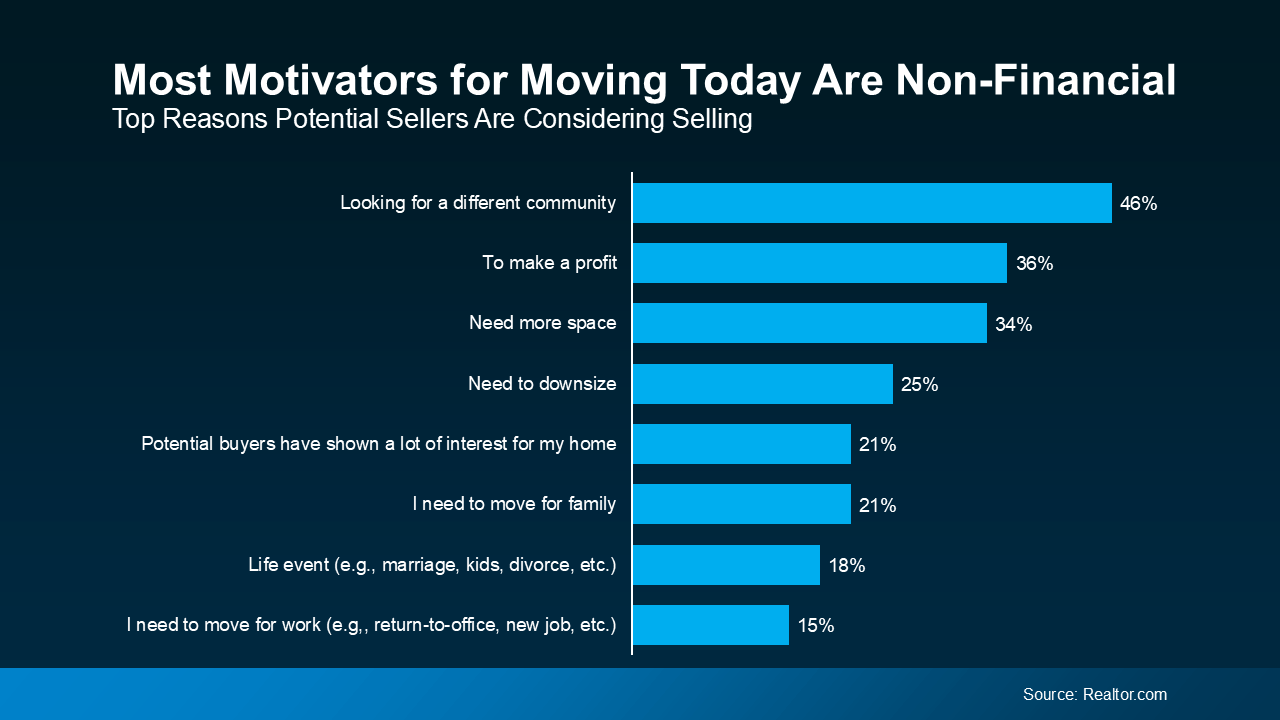

Why People Move Despite Higher Rates

Recent surveys reveal something fascinating: 79% of homeowners who are considering selling today are doing it out of necessity, not choice. And most of these necessary reasons are non-financial in nature. They’re about life changes that can’t be put on hold indefinitely.

Maybe you need more space because there’s a baby on the way, or your aging parents need to move in so you can take care of them more easily. Perhaps your kids are out of the house now and you’re craving something simpler – fewer rooms to clean, less to maintain, lower utility bills.

Sometimes it’s about being closer to family. Whether you want to help with grandchildren or need to care for aging parents, the pull of being near loved ones can outweigh any financial calculations. Other times it’s relationship changes – divorce, separation, or moving in together after marriage or starting a new partnership.

And then there’s work. If you’ve landed your dream job or your partner’s company is relocating, sometimes you simply have to move regardless of what mortgage rates are doing.

Rate Forecasts

While experts do expect mortgage rates to ease somewhat, the keyword here is “slowly.” The latest projections show only modest declines over the coming months and year – definitely not the 3% rates some people are hoping will magically return.

Waiting for a big drop in rates might just mean spending more time feeling stuck in a space that no longer fits your life. And for many people, that waiting game has already dragged on far too long. Data shows that nearly two out of three potential sellers have been thinking about moving for over a year.

If that’s you, it’s worth asking yourself: how much longer are you willing to press pause on your life? Maybe the house you’re in right now fit your life five years ago. But that “for now” house you bought back in 2020? It might not be delivering what you actually need in 2025.

Those 3% Rates Aren’t Coming Back

I know this might be tough to hear, but it’s important to understand: those 3% rates were never meant to last. They weren’t the new normal – they were a short-term response to a very specific moment in time.

Back in 2020 and 2021, those incredibly low rates gave buyers serious advantages in terms of affordability and buying power. But they were the result of emergency economic policies implemented during the height of a global pandemic. Now that the economy has shifted into a different phase, we’re seeing rates settle into a new range.

While experts currently project some easing in the months ahead, virtually all industry leaders agree on one thing: rates are not going back to 3%. Those days are behind us. Instead, forecasts suggest mortgage rates will likely settle somewhere in the mid-6% range, pending any major economic upheavals.

As one economist puts it, while rates may end the year near the mid-6% level barring any unforeseen shocks, the path to get there might be bumpy along the way.

What You Can Control

Trying to time the market perfectly based on rate predictions is basically impossible. You can’t control what happens with the overall economy or where mortgage rates go on any given day. But here’s the good news: there are several things you absolutely can control that will significantly impact the rate you qualify for.

Your credit score is huge. This single number can really affect what mortgage rate a lender offers you. Even a relatively small improvement in your score can translate to a meaningful difference in your monthly payment. Lenders typically reward higher credit scores with lower interest rates and better loan terms.

If you’re not sure where your credit score currently stands or how to improve it, talking with a loan officer should be your first step. They can review your credit report with you and point out specific actions that will boost your score.

Your loan type matters too. There are several different categories of mortgages out there – conventional loans, FHA loans, USDA loans, VA loans, and others. Each comes with unique requirements for qualified buyers, and rates can vary significantly depending on which type you choose.

Lenders decide which products to offer, so talking with multiple lenders can help you understand all the options available to you. What works best depends on your specific financial situation, down payment amount, and long-term plans.

Then there’s your loan term. Most lenders typically offer 15, 20, or 30-year conventional loans. Your loan term affects not just your interest rate, but also your monthly payment and the total amount of interest you’ll pay over the life of the loan. A shorter term usually means a lower rate but higher monthly payments, while a longer term spreads payments out but costs more in total interest.

Financing Options to Consider

Since rates aren’t expected to decline as dramatically as many people originally hoped, it’s worth exploring alternative financing strategies that could help you get into a home sooner rather than later.

Mortgage buydowns allow you to pay an upfront fee to temporarily lower your mortgage rate for a set period. This can be especially helpful if you want or need a lower monthly payment early on. Interestingly, 27% of real estate agents report that first-time homebuyers are increasingly requesting that sellers contribute to buydowns as part of the deal.

Adjustable-rate mortgages, or ARMs, typically start with a lower rate than traditional 30-year fixed mortgages. This makes them attractive, especially if you expect rates to drop in coming years or if you plan to refinance down the road.

Now, if you remember the housing crash from 2008, you might be thinking ARMs are risky. Here’s the important distinction: today’s ARM products are fundamentally different from the problematic ones issued in the mid-2000s. Back then, lenders often approved ARMs based on whether borrowers could afford just the initial lower rate, and sometimes they didn’t even verify income properly.

Today, adjustable-rate borrowers must qualify based on their ability to cover a higher monthly payment, not just that initial teaser rate. Banks now verify income, assets, and employment much more carefully, which significantly reduces the risks compared to the past.

Assumable mortgages represent another option worth exploring. This allows you to essentially take over the seller’s existing loan, including their lower mortgage rate. With more than 11 million homes potentially qualifying for this option, it’s definitely worth investigating if you’re looking for ways to secure a better rate.

Volatility

Have you noticed mortgage rates bouncing around lately? One day they drop a little, the next day they climb back up. It can feel genuinely confusing and frustrating when you’re trying to figure out whether now is a good time to buy.

Looking at recent data, we can see that after a relatively stable period in March, rates went on something of a roller coaster ride through April. This kind of up-and-down volatility is actually expected when significant economic changes are happening.

This volatility is precisely why trying to time the market perfectly isn’t your best strategy. You simply can’t control what happens with mortgage rates on a day-to-day basis. But you’re far from powerless in this situation. Even with all the economic uncertainty, you can take concrete actions that put you in the strongest possible position.

What Influences Rate Movements

Understanding what drives mortgage rate changes can help you make sense of all the ups and downs. Several key factors influence where rates go, and they’re all interconnected in complex ways.

Inflation plays a massive role. If inflation cools down, rates could dip further. On the flip side, if inflation rises or remains stubbornly high, rates may stay elevated longer than anyone wants. The Federal Reserve watches inflation data like a hawk and adjusts their policies accordingly.

The unemployment rate also significantly impacts decisions by the Fed. While the Federal Reserve doesn’t directly set mortgage rates, their actions reflect what’s happening in the broader economy, which definitely impacts where rates go.

Government policies matter too. With any new administration or changes in fiscal and monetary policy, financial markets respond, and those responses filter down to affect mortgage rates. It’s all connected in this intricate web of economic factors.

The Coming Months

After considerable volatility and uncertainty, the most recent forecasts suggest rates should start stabilizing over the next year. Experts expect them to ease slightly compared to current levels, but again, we’re talking about modest improvements rather than dramatic drops.

As one chief economist recently noted, while mortgage rates remain elevated, they are expected to stabilize. That’s actually good news in its own way – stability means you can plan more confidently without worrying about massive swings.

It’s important to understand that forecasting mortgage rate timing and pace is one of the most challenging predictions to make in the entire housing market. These forecasts depend on multiple key factors all lining up properly. While rates are expected to come down slightly, they’re going to remain a moving target with ongoing ups and downs driven by economic factors.

Don’t try to time the market based on forecasts alone. Instead, focus on what you can actually control right now. Work on improving your credit score. Put away any extra cash toward your down payment. Automate your savings so you’re consistently building up funds. All of these actions help you reach your homeownership goals regardless of what rates do.

Stay Informed

If you’re planning to move and want to stay informed about where mortgage rates are heading, your best bet is connecting with trusted professionals who can guide you through all of this complexity.

A knowledgeable local real estate agent understands what’s happening in your specific market. They can explain whether it makes sense to make your move now, before competition potentially intensifies if and when rates drop further.

A trusted lender can review your specific financial situation, explain which loan products make sense for you, and help you understand creative options that could make homeownership more affordable right now rather than waiting indefinitely for perfect conditions that may never arrive.

Remember, rates in the mid-6% range aren’t historically high when you look at the bigger picture. Yes, they’re higher than those pandemic-era emergency rates, but they’re not unprecedented or unmanageable. Plenty of people are successfully buying homes right now at these rates.

The question isn’t really whether rates are ideal – they probably never will be. The question is whether waiting for marginally better rates is worth potentially missing out on the perfect home, facing increased competition, or continuing to put your life on hold.

Sometimes the best financial decision isn’t the one that looks perfect on paper. Sometimes it’s the one that lets you move forward with your life, in a home that actually meets your needs, in a neighborhood where you want to be, at a time when you have negotiating power and actual choices.

What matters most isn’t necessarily getting the absolute lowest rate possible. What matters is finding the right home at the right time for your life circumstances, with financing terms you can comfortably manage for the long term. And for many people, that time might be right now, even if rates aren’t exactly where we wish they were.

The housing market will always have some uncertainty. There will always be reasons to wait, always something on the horizon that might potentially improve conditions slightly. But life doesn’t wait, and your needs don’t pause just because economic conditions aren’t perfect.

Talk with professionals who can give you personalized advice based on your actual situation rather than hypothetical scenarios. They can help you build a game plan that works for you, taking into account not just where rates are today, but where you are in life and what you actually need from a home.