If you’ve owned your home for a few years, there’s a good chance you’re sitting on more money than you think. Not cash in a savings account, but equity, the share of your home you actually own free and clear.

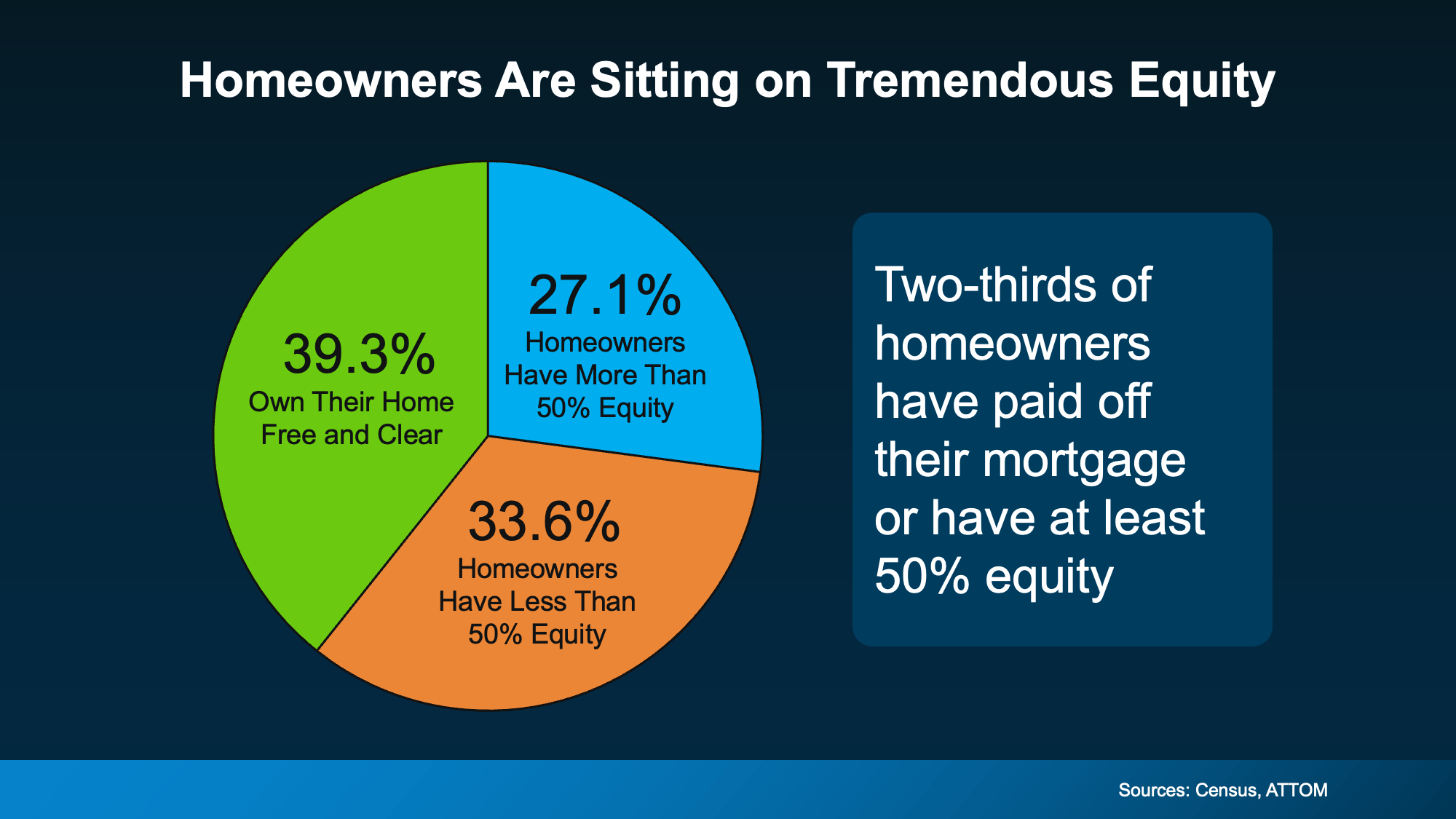

Two-thirds of American homeowners have significant equity right now, according to Census and ATTOM data. About 39% own their homes outright, and another 27% have at least 50% equity built up. The typical homeowner has close to $300,000 in equity, per Cotality. That’s real money, even if it doesn’t feel like it because you can’t see it in your bank balance.

But here’s where things get tricky. Having equity and knowing how to use home equity wisely are two very different things. Tapping into it at the wrong time or for the wrong reasons can cost you thousands, or worse, put your home at risk. So let’s walk through your actual options, what they cost, and when each one makes sense.

What home equity is and how to calculate yours

Home equity is simple math. Take what your home is worth today and subtract what you still owe on your mortgage. The difference is your equity.

Say you bought a home for $350,000 with a $280,000 mortgage. You’ve paid the balance down to $220,000 over the years, and your home has appreciated to $400,000. Your equity is $180,000.

Two things build equity over time. First, every mortgage payment chips away at your loan balance. Second, if your local market pushes home values up, your equity grows without you doing anything at all. Most homeowners benefit from both simultaneously.

One catch worth knowing: the equity number you calculate at home is an estimate. Lenders require a formal appraisal before they’ll let you borrow against it. Your neighbor’s sale price gives you a ballpark, but the appraiser’s number is the one that counts.

Four ways to access your home equity

You can’t just withdraw equity like money from an ATM. You have to borrow against it, and each borrowing method works differently. Here’s what you’re actually choosing between.

Cash-out refinance

A cash-out refinance replaces your current mortgage with a new, larger one. You use part of the new loan to pay off the old mortgage and pocket the rest as cash.

This sounds clean on paper, but the details matter. Your new loan comes with a new interest rate, new terms, and potentially a longer repayment timeline. If you locked in a 3% mortgage a few years ago and today’s rates are hovering around 6-7%, a cash-out refi means giving up that low rate on your entire balance, not just the cash you’re pulling out.

That trade-off hits hard. On a $300,000 mortgage, the difference between 3% and 7% adds up to hundreds of extra dollars every month for the next 30 years.

A cash-out refinance works best when current rates are close to (or lower than) your existing rate, or when you need a large lump sum and the math still pencils out after factoring in the rate change.

Home equity loan

A home equity loan is a second mortgage. You keep your existing mortgage exactly as it is and take out a separate loan against your equity. You get the money in one lump sum, typically at a fixed interest rate, with a fixed repayment term between 5 and 30 years.

The upside here is predictability. Fixed rate, fixed payment, same amount due every month until it’s paid off. You also don’t touch your original mortgage rate, which matters a lot if you locked in something low.

The downside is you now have two monthly mortgage payments. And because it’s a second lien (meaning your first mortgage gets paid before it does if things go sideways), interest rates on home equity loans tend to run higher than first mortgages.

Home equity loans make the most sense when you know exactly how much money you need upfront, like for a specific renovation project or a one-time expense.

Home equity line of credit (HELOC)

A HELOC also uses your home as collateral, but instead of a lump sum, you get a revolving line of credit. Think of it like a credit card backed by your house. You draw money as you need it, up to your approved limit, and you only pay interest on what you actually borrow.

HELOCs come in two phases. During the draw period (usually 5-10 years), you can borrow and repay freely, with payments often covering just interest. After that, you enter the repayment period (usually 10-15 years), where you pay back principal and interest on whatever balance remains.

There’s one thing that trips people up with HELOCs: most carry variable interest rates. Your payment can change month to month based on market conditions. That initial low rate might climb over the life of the loan. Some lenders offer fixed-rate options on portions of your HELOC balance, so ask about that if rate predictability matters to you.

A home equity line of credit works well for ongoing expenses or projects that happen in phases, like a multi-room renovation where costs come in waves over several months.

Reverse mortgage

Reverse mortgages are designed specifically for homeowners 62 and older. Instead of making monthly payments to a lender, the lender pays you, either as a lump sum, monthly installments, or a line of credit. You don’t repay the loan until you sell the home, move out, or pass away.

There’s no monthly mortgage payment, but you still have to cover property taxes, homeowners insurance, and home maintenance. Miss those obligations and you can face foreclosure just like with any other mortgage product.

Your loan balance grows over time because interest and fees get added to what you owe each month. That means your equity shrinks as the years pass. By law, you’ll never owe more than 95% of your home’s appraised value when the loan comes due, but your heirs will need to deal with the remaining balance, usually by selling the home.

Closing costs on reverse mortgages run higher than other options because borrowers are required to pay mortgage insurance. You’re also required to meet with a HUD-approved housing counselor before you can take one out, which is actually a good thing.

Reverse mortgages fit a narrow situation: retirees who plan to stay in their home long-term, need supplemental income, and aren’t focused on leaving the property to their children debt-free.

Smart ways to use home equity

Having access to equity is one thing. Spending it wisely is another. Here are the uses that tend to make financial sense.

Home improvements that add value

Reinvesting equity back into your property is one of the more logical uses because done right, you’re increasing the home’s value while also improving your living situation. Kitchen and bathroom renovations consistently return a good chunk of their cost at resale.

The key word there is “done right.” Not every renovation pays for itself. A $50,000 backyard pool might make your summers better, but it won’t add $50,000 to your home’s sale price. Talk to a local real estate agent before you start any major project so you can prioritize updates that actually move the needle when it’s time to sell.

Debt consolidation (with a big asterisk)

If you’re carrying high-interest credit card debt at 18-24% APR, replacing it with a home equity loan at 7-9% can save you a significant amount in interest. The math works on paper.

But this strategy has a serious risk baked in. You’re converting unsecured debt into debt secured by your home. If you can’t make the payments on a credit card, your credit score takes a hit. If you can’t make the payments on a home equity loan, you could lose your house.

There’s also a behavioral trap. Plenty of people consolidate their credit card debt using home equity, then run those credit cards right back up because the underlying spending habits haven’t changed. Now they have both the home equity loan and new credit card debt, which is a worse position than where they started.

Consolidation makes sense only when the interest rate savings are substantial and you’ve genuinely addressed whatever caused the debt in the first place.

Funding a major life expense

Some homeowners use equity to start a business, cover education costs, or help a family member with a down payment on their own home. These can be reasonable uses, especially when the alternative is higher-interest borrowing.

College tuition is a common one. Home equity loan and HELOC rates are typically lower than private student loan rates, and the interest may be tax-deductible if the funds are used for certain qualified purposes (check with a tax advisor on your specific situation).

Moving to a home that fits your life

If you’ve outgrown your current place or the kids have moved out and you’re rattling around in too much space, your equity can fund the down payment on the next home. Some homeowners in high-equity positions can buy their next house outright with cash from their sale.

This isn’t technically “tapping” equity through a loan product. You’re accessing it by selling. But it’s worth mentioning because selling is the cleanest, simplest way to turn equity into money, with no new debt attached.

When you should leave your equity alone

Not every situation calls for touching your equity, and honestly, some of the most common reasons people consider it don’t hold up under scrutiny.

Your existing debts have lower rates than what you’d borrow at

This is the scenario that catches a lot of people off guard. If you’re carrying debts at 4%, 5%, and 6%, and the best HELOC or home equity loan rate you can find is 7% or higher, consolidating those debts into a home equity product means you’re paying more interest, not less. You’re also moving from unsecured debt to debt secured by your home. That’s a bad trade in both directions.

You want to free up monthly cash flow without a real plan

Stretching payments over a longer term through equity borrowing can lower your monthly bills, but you’ll pay significantly more in total interest over time. If the goal is cash flow relief, look at your budget first. Cutting expenses or increasing income solves the problem without adding risk to your home.

The improvements are cosmetic and you have young kids

This one’s practical. If your children are still in the phase where walls get crayoned and floors get abused, expensive cosmetic renovations are going to take a beating before you see any return. Wait until the wear-and-tear years pass. Structural issues like a failing roof or foundation problems are different, those shouldn’t wait regardless.

You’re treating equity like a savings account

One of the most common misconceptions about home equity is that it’s money “just sitting there” waiting to be used. It’s not. Equity is wealth on paper that you can only access by taking on new debt or selling your home. Borrowing against it reduces your ownership stake and comes with interest, fees, and risk. Treat it as a last resort or a strategic tool, not a piggy bank.

The 20% equity rule

Regardless of which option you choose, most financial professionals recommend keeping at least 20% equity in your home at all times. This serves as a financial cushion if home values dip and helps you avoid owing more than your home is worth, a painful situation many homeowners experienced during the 2008 crash.

The good news is that most homeowners today are well above that threshold. According to the Intercontinental Exchange, mortgage holders collectively have $17.3 trillion in home equity, with $11.2 trillion considered “tappable” equity, meaning it can be accessed while still maintaining that 20% buffer.

Your lender will enforce their own version of this rule. Most won’t let you borrow more than 80-90% of your home’s value across all loans combined.

Costs you need to factor in

Every equity product comes with upfront costs that eat into the money you actually receive. Budget for these before you commit.

Closing costs on home equity loans, HELOCs, and cash-out refinances typically range from 3-6% of the loan amount. On a $100,000 loan, that’s $3,000-$6,000 before you’ve spent a dime on whatever you’re borrowing for.

You’ll likely pay for an appraisal, origination fees, title search, and credit report fees at minimum. Reverse mortgages tend to have the highest closing costs of the bunch because of the required mortgage insurance premium.

If you plan to sell your home within the next couple of years, these upfront costs may not be worth it. You’d be paying thousands to access money for a short period before the loan gets paid off at closing anyway. In that case, a HELOC with lower upfront costs might make more sense than a full refinance, or you might be better off just waiting to sell.

Before you borrow against your home

If you’re seriously considering using your equity, take two steps before you sign anything.

First, get a realistic picture of how much equity you actually have. Ask a local real estate agent for a market analysis of your home, or look at recent comparable sales in your area. This won’t replace the formal appraisal your lender will require, but it gives you a starting point.

Second, talk to a financial advisor. They can help you evaluate whether borrowing against your home is the right move for your specific situation, or whether there’s a better option you haven’t considered. This is especially important for retirees looking at reverse mortgages, where the long-term implications are significant.

The interest you pay on home equity products may be tax-deductible if the funds are used for home improvements, but the rules have specific requirements. A tax advisor can tell you whether your planned use qualifies.

Bottom line

Your home equity is probably one of the largest financial assets you have. That makes it worth protecting. Used strategically, for the right purpose and at the right time, it can fund renovations, eliminate expensive debt, or help you make a major life transition. Used carelessly, it can pile on debt and put your home at risk. The best use of equity is one where you’ve done the math, compared the rates, understood the fees, and have a clear plan for repayment. If the numbers don’t work in your favor right now, sitting tight is a perfectly valid financial decision. Your equity isn’t going anywhere.