(Updated 10/21/25)

When you’re house hunting, your mind is probably racing with thoughts about finding the perfect neighborhood, securing a great mortgage rate, and imagining where your furniture will go. But there’s one thing that might not be on your radar yet could significantly impact your monthly budget: homeowners association fees.

If you’ve ever driven through a pristine neighborhood with perfectly manicured lawns, sparkling community pools, and immaculate common areas, you’ve likely witnessed the magic of an active HOA at work. But that magic comes with a price tag, and understanding what you’re getting into before you sign on the dotted line can save you from some serious financial surprises down the road.

Let’s dive into everything you need to know about HOA fees, from what they actually cover to whether they’re worth the investment for your lifestyle.

What Is a Homeowners Association

Think of a homeowners association as the neighborhood’s management team. It’s essentially a nonprofit organization that creates, maintains, and enforces the rules for a specific community or residential area. These associations are incredibly common in planned communities, condominium buildings, and many newer subdivisions.

Here’s the thing about HOAs: when you buy a property in a community with one, membership isn’t optional. You’re automatically enrolled, which means you’re automatically on the hook for those monthly or annual fees. It’s kind of like joining a club you didn’t necessarily ask to join, but now you’re in it for the long haul as long as you own that property.

The whole point of having an HOA is twofold. First, they’re responsible for keeping all those shared spaces looking good and functioning properly. Second, they establish and enforce rules designed to protect everyone’s property values. That means your neighbor can’t decide to paint their house hot pink or let their yard turn into a jungle, because those decisions could potentially bring down the value of your home too.

Breaking Down HOA Fees

HOA fees are regular payments that homeowners make to their association, typically on a monthly basis, though some communities collect them quarterly or annually. These aren’t just arbitrary charges dreamed up to annoy homeowners. They’re carefully calculated amounts designed to cover all the costs associated with running and maintaining the community.

You might also hear these fees called “common charges” or “maintenance charges,” especially in condominium communities. Whatever name they go by, the concept is the same: everyone chips in to keep the community running smoothly.

The amount you’ll pay varies wildly depending on where you live and what the HOA provides. Some neighborhoods charge as little as a hundred bucks a month, while luxury communities with extensive amenities can hit you with fees exceeding several thousand dollars monthly. Yeah, you read that right – thousands.

HOA Membership Perks

Before we get too deep into the costs, let’s talk about what you’re actually getting for your money. Because despite what you might hear from HOA horror stories on the internet, there are genuine benefits to living in an HOA community.

Someone Else Handles the Maintenance

Imagine never having to worry about mowing common area lawns, shoveling snow from shared walkways, or maintaining that beautiful landscaping you admired when you first toured the neighborhood. That’s exactly what your HOA fees cover in many communities. The association takes care of all the maintenance for shared spaces, which means you can actually relax on the weekends instead of doing yard work.

In condominium settings, this gets even better. Your HOA handles everything outside your unit’s walls, including roof repairs, exterior painting, and maintaining parking areas. You’re literally just responsible for what’s inside your four walls.

Amenities You Couldn’t Afford Solo

Want a pool in your backyard? That’ll cost you tens of thousands of dollars to install, plus ongoing maintenance costs. But in an HOA community, you might get access to not just one pool, but multiple pools, along with hot tubs, tennis courts, a state-of-the-art fitness center, and a clubhouse perfect for hosting parties.

When you break down the math, paying your HOA fee for access to all these amenities often costs way less than trying to replicate them yourself. Plus, you don’t have to worry about the maintenance or insurance headaches that come with owning these features individually.

Your Property Value

This is a big one that people don’t always think about. HOAs enforce community standards that prevent individual homeowners from making changes that could negatively impact everyone’s property values. Your neighbor can’t decide to stop maintaining their property or make wild modifications that turn their house into the neighborhood eyesore.

Those well-maintained streets, professional landscaping, and overall community appearance you fell in love with? They’re not accidental. They’re the result of HOA standards and enforcement, which helps ensure your home maintains its value over time.

Less Stress About Big Repairs

Many HOAs maintain reserve funds specifically for major repairs and unexpected emergencies. If the community’s roof needs replacing or there’s significant storm damage, the HOA has funds set aside to handle it. You’re contributing to these reserves through your monthly fees, but when something goes wrong, you’re not facing a massive unexpected bill all at once.

What Your Monthly HOA Fees Cover

The specifics vary from community to community, but HOA fees typically fund a pretty comprehensive list of services and expenses. Let’s break down where your money actually goes.

Municipal Services

In many HOA communities, your fees cover services you’d otherwise pay for separately. We’re talking about trash removal, water and sewer services, and sometimes even basic utilities. Some communities include cable or internet in their HOA fees too. This means fewer bills to track each month, which is a nice bonus for the organizationally challenged among us.

Keeping Common Areas Beautiful

All those gorgeous shared spaces need constant attention. Your fees pay for landscaping services, seasonal plantings, lawn care, and general upkeep of common areas. In regions with harsh winters, snow removal from shared roads and parking areas comes out of HOA fees too.

The community pool doesn’t clean itself, the fitness equipment needs maintenance, and someone has to make sure the clubhouse stays in good shape. All of that ongoing maintenance comes directly from the collective pool of HOA fees.

Insurance Coverage for Shared Spaces

Your HOA is legally required to carry insurance covering injuries or damage that occur in common areas. If someone slips and falls in the lobby or gets hurt at the community pool, the HOA’s insurance covers it. This is separate from your personal homeowners insurance, which you’ll still need to protect your individual unit or home.

Security and Safety

Depending on your community, HOA fees might fund security services ranging from gated entry systems and surveillance cameras to actual security personnel. Some luxury communities employ door attendants, valet services, or roving security guards. Obviously, the more extensive the security setup, the higher your fees will be.

Building a Financial Safety Net

A portion of every HOA fee payment goes into reserve funds. Think of this as the community’s savings account for big-ticket items and emergencies. When the elevator needs replacing, the parking lot requires resurfacing, or unexpected damage occurs, the HOA dips into these reserves rather than hitting homeowners with massive special assessments.

How Much Will You Really Pay

Let’s talk numbers. According to recent data, the national average monthly HOA fee sits around two hundred to three hundred dollars, with a median closer to eighty-three dollars. But these are just averages, and your actual costs could be drastically different.

If you’re buying a modest single-family home in a basic HOA community, you might pay less than a hundred dollars monthly. Meanwhile, a luxury high-rise condo in a major city could easily run you over a thousand dollars every month. Some ultra-luxury communities charge several thousand dollars monthly for access to premium amenities and services.

Location plays a huge role in determining fees. A community in New York City faces much higher operating costs than a similar community in a smaller Midwestern city. Higher wages, more expensive utilities, increased property taxes – all these factors drive up HOA fees in expensive metropolitan areas.

The type and extent of amenities matter too. A community with just basic lawn maintenance will obviously charge less than one offering multiple pools, a full-service gym with personal trainers, concierge services, and regular community events.

Newly Built Homes and the HOA Trend

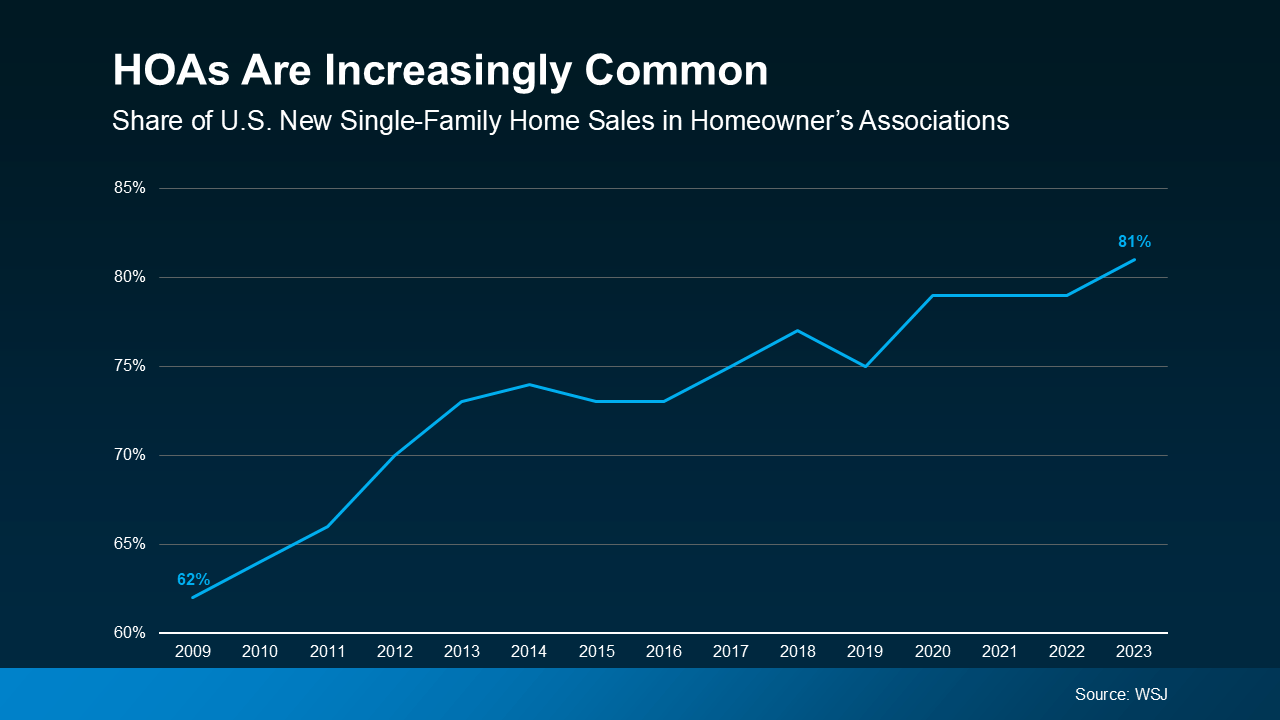

Here’s something interesting: if you’re looking at newly built homes, there’s a pretty high chance you’ll be dealing with an HOA. Recent statistics show that over eighty percent of new single-family homes are part of an HOA. That’s a dramatic shift from previous decades.

Developers favor HOAs because they help maintain the quality and appearance of new communities, which protects their reputation and helps them sell homes more easily. For buyers, this means if you’re shopping for new construction, you should basically assume there will be HOA fees unless specifically stated otherwise.

Even existing homes in older neighborhoods increasingly have HOAs. About four out of every ten homes nationwide are now part of some kind of homeowners association. It’s becoming less of a “sometimes” thing and more of a “probably” thing.

Additional Costs

Your monthly HOA fee isn’t always the only money you’ll pay to the association. There are a couple of other potential expenses you should know about before committing to an HOA community.

Special Assessments: The Unexpected Bills

Sometimes the HOA’s reserve funds aren’t enough to cover a major expense. Maybe there was unexpected storm damage, a critical system failed earlier than anticipated, or previous boards didn’t adequately fund the reserves. When this happens, the HOA can impose special assessments – basically extra charges to all homeowners to cover these costs.

Special assessments can be substantial, sometimes running into thousands of dollars per homeowner. They’re typically divided into payments rather than demanded as a lump sum, but they’re still an additional financial burden on top of your regular fees. Before buying into an HOA community, it’s smart to review the association’s financial records and reserve fund status to gauge the likelihood of future special assessments.

Fines for Rule Violations

Remember all those rules the HOA enforces? Breaking them can cost you money. Most HOA communities have detailed regulations about everything from what colors you can paint your house to how tall your grass can grow before you need to mow it.

Violate these rules, and you’ll likely receive a warning first. But continued violations typically result in fines. These can add up quickly, and in extreme cases, failure to pay fines can lead to the same consequences as failing to pay your regular HOA fees.

What Happens If You Don’t Pay

This is where things get serious. HOAs depend entirely on member fees for their operating budget. When homeowners don’t pay, it creates problems for everyone in the community. That’s why HOAs have significant authority to collect what they’re owed.

The Initial Consequences

Miss a payment and you’ll first receive a notice, usually with a late fee tacked on. If you don’t pay within thirty days, expect that late fee to increase. The HOA might also suspend your privileges, meaning you can’t use the pool, fitness center, or other community amenities until you’re current on your fees.

Legal Action

If you continue not paying, the HOA can take several legal actions. They might place a lien on your property, which becomes a matter of public record and makes it nearly impossible to sell or refinance your home until you’ve paid what you owe.

Some HOAs will file a lawsuit to collect unpaid fees. In extreme cases, and depending on your state’s laws, an HOA can actually foreclose on your home to collect unpaid dues. Yes, you could literally lose your house over unpaid HOA fees. It’s rare, but it happens.

The Downsides

While there are benefits to HOA living, it’s not all sunshine and roses. There are legitimate drawbacks that might make HOA communities a poor fit for some people.

The Cost Factor

The most obvious downside is simply the ongoing expense. Adding another two hundred to several thousand dollars to your monthly housing costs can strain your budget, especially when combined with your mortgage payment, property taxes, homeowners insurance, and utilities.

And remember, HOA fees typically increase over time. As operating costs rise and the community’s needs change, you can expect regular fee increases that you have little control over.

Loss of Personal Freedom

HOAs are all about rules, and some people find them overly restrictive. Want to paint your front door a bold color? You might need approval. Thinking about adding a fence? Better check if it’s allowed and what specifications you need to follow. Hoping to run a small business from home? Many HOAs prohibit or strictly limit this.

For people who value personal freedom and want complete control over their property, HOA restrictions can feel suffocating.

Potential for Mismanagement

HOAs are run by boards made up of fellow homeowners who volunteer their time. While many boards do an excellent job, some don’t. Poor financial management can lead to depleted reserve funds and frequent special assessments. Ineffective leadership can result in deteriorating common areas and declining property values.

You’re essentially trusting your neighbors to make good decisions that affect your home’s value and your monthly expenses. That doesn’t always work out well.

Is an HOA Right for You?

So how do you decide whether an HOA community is right for you? It really comes down to your personal preferences, lifestyle, and financial situation.

If you love the idea of maintained common areas, access to amenities, and not worrying about exterior maintenance, an HOA might be perfect for you. If you’re buying a condo or townhouse, you probably don’t have much choice since these properties almost always come with HOA fees.

On the flip side, if you’re someone who values complete autonomy over your property, doesn’t particularly want access to community amenities, and prefers to handle your own maintenance on your own schedule, you might be happier in a non-HOA neighborhood.

Before committing to any HOA community, do your homework. Request copies of the CC&Rs, review the HOA’s financial statements, check out the meeting minutes to see what issues the community faces, and talk to current residents if possible. Find out about any pending special assessments or upcoming major expenses.

Make sure you can comfortably afford the HOA fees on top of all your other housing expenses. Factor in the likelihood of fee increases over time. And be honest with yourself about whether you can live with the community’s rules and restrictions.

HOA Living?

Homeowners association fees are a reality for millions of Americans living in planned communities, condominiums, and many newer neighborhoods. These fees fund the maintenance, amenities, and services that keep these communities looking great and functioning smoothly.

Whether HOA fees represent good value depends entirely on what you’re getting for your money and how well it aligns with your lifestyle. For some people, having access to a beautiful pool, well-maintained grounds, and peace of mind about exterior maintenance is absolutely worth a few hundred dollars a month. For others, those same fees feel like money down the drain for services they don’t want or need.

The key is going into your home purchase with eyes wide open. Understand exactly what your HOA fees cover, what rules you’ll need to follow, and whether the community’s culture and priorities align with your own. When you find the right fit, an HOA community can enhance your living experience and protect your investment. Choose poorly, and you might find yourself stuck in a situation that drains your wallet and limits your freedom.

Take your time, ask lots of questions, and make sure you’re making a decision that supports both your immediate needs and your long-term goals. Your future self will thank you for doing the homework now rather than dealing with buyer’s remorse later.