(Updated 9/30/25)

Ever scrolled through your news feed and felt your stomach drop after seeing yet another article screaming about foreclosure spikes? Yeah, we’ve all been there. Those attention-grabbing headlines have a knack for making you wonder if we’re heading for another 2008-style meltdown. But here’s the thing – when you actually dig into what the numbers are really saying, you’ll find the situation is nowhere near as dramatic as those clickbait titles want you to believe.

Let’s have a real talk about what’s actually happening with foreclosures right now, because you deserve to know the full story, not just the sensationalized version designed to rack up clicks.

What They’re Not Telling You

Sure, foreclosure activity has ticked up recently. The media loves pointing out that foreclosure starts jumped 7% in the first half of the year. Sounds scary, right? But here’s what those headlines conveniently leave out – they’re comparing today’s numbers to an incredibly unusual period when foreclosures were at absolute rock-bottom levels.

Think back to 2020 and 2021. Remember the foreclosure moratorium? The forbearance programs? These weren’t just minor policy tweaks – they were massive intervention programs that essentially put a pause button on foreclosures across the entire country. Millions of homeowners who might have otherwise faced foreclosure got the breathing room they desperately needed to get back on their feet during one of the most challenging economic periods in modern history.

So yeah, when those programs wrapped up, foreclosures naturally started climbing again. That’s not a crisis – that’s literally what everyone expected to happen. It’s like being surprised that traffic picks back up after a road closure ends. Of course it does!

The real question isn’t whether foreclosures are higher than during those unprecedented intervention years – it’s whether they’re at concerning levels compared to normal, healthy market conditions. And spoiler alert: they’re absolutely not.

Let’s Talk Real Numbers

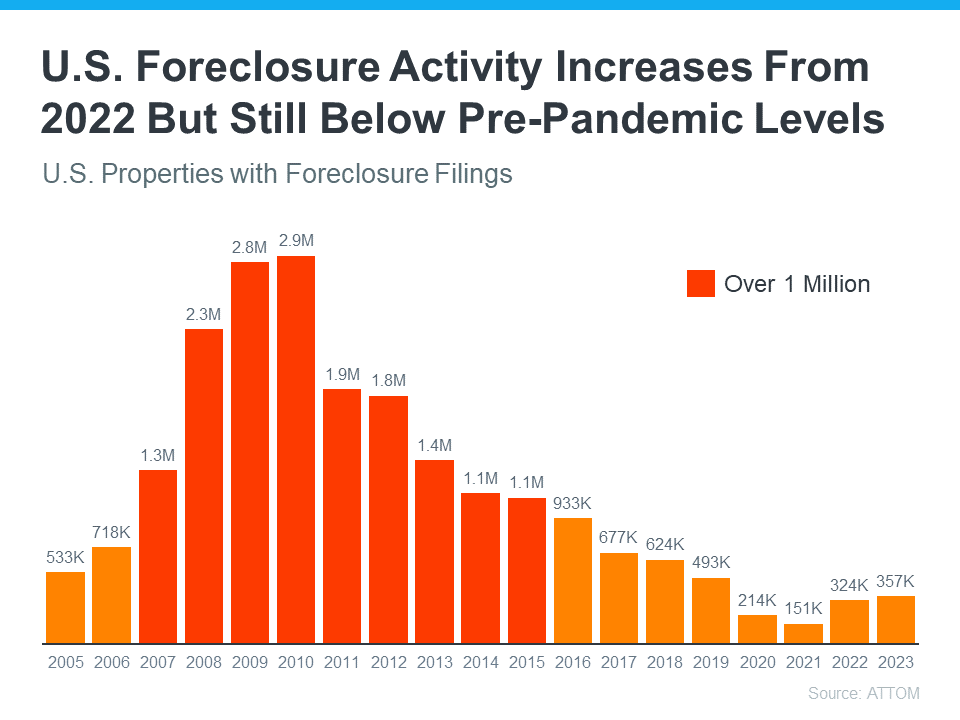

Here’s where things get interesting. In the first half of 2025, only 0.13% of homes had foreclosure filings. Let that sink in for a second. That’s not 1% – it’s not even close to 1%. We’re talking about roughly one-tenth of one percent. That’s such a tiny fraction that it barely registers.

To put this in more concrete terms, ATTOM data shows that about 1 in every 758 homes nationwide had a foreclosure filing during this period. Now compare that to 2010, right in the thick of the housing crisis, when it was 1 in every 45 homes. That’s a staggering difference – we went from roughly 2.2% of homes in foreclosure during the absolute worst of times to just 0.13% today.

That’s not just a little better – that’s a completely different universe. We’re talking about foreclosure rates that are literally a fraction of what they were during the crash, and honestly, we’re not even back to what you’d see in a typical, run-of-the-mill year before the pandemic threw everything into chaos.

Rick Sharga, who heads up the CJ Patrick Company and knows his stuff when it comes to foreclosure data, puts it pretty clearly: foreclosure activity is still only running at about 60% of what we’d consider normal pre-pandemic levels. So if you’re worried we’re approaching crisis territory, the actual data is telling a very different story.

Why Today’s Market Isn’t Even Playing the Same Game

Remember what made the housing crash so devastating? It wasn’t just that foreclosures went up – it was the perfect storm of terrible conditions that all hit at once. Lenders were handing out mortgages like candy at Halloween, with barely any verification of whether people could actually afford the payments. We had NINJA loans (seriously, that stood for No Income, No Job, No Assets – imagine getting approved for a mortgage with literally none of those things!). We had adjustable-rate mortgages that people didn’t fully understand, which eventually ballooned into payments they couldn’t possibly manage.

And here’s what made it truly catastrophic: when people inevitably couldn’t make those payments, they found themselves underwater on their mortgages – owing more than their homes were worth. They were trapped. Couldn’t sell because they’d lose money. Couldn’t refinance because no lender would touch them. The only option left was to walk away and let the bank take the house. That’s when foreclosures absolutely exploded and the whole market came crashing down.

Fast forward to today, and it’s like we’re living in a completely different world. The lending landscape has been totally transformed.

The Safety Nets That Didn’t Exist Before

First off, lending standards today are actually, you know, standards. Lenders learned their lessons the hard way, and now they’re verifying income, checking debt-to-income ratios, requiring proper down payments – all the boring but important stuff that ensures people can actually afford the mortgages they’re taking out. Sure, it means qualifying for a loan is tougher than it used to be during the wild west days of lending, but it also means the people who do qualify are in much better shape to handle their payments over the long haul.

But here’s the real game-changer: equity. This is absolutely crucial to understand, so pay attention. Homeowners today are sitting on near-record levels of home equity. What does that mean in practical terms? It means most people owe way less on their mortgages than their homes are actually worth. Like, substantially less.

This is the polar opposite of what happened during the crash, and it changes everything. When someone hits financial trouble today – maybe they lose their job, face unexpected medical bills, whatever life throws at them – they actually have options. They can sell their house, potentially walk away with a nice chunk of cash, and move somewhere more affordable or figure out their next move without the black mark of foreclosure on their credit.

As Rick Sharga explains it, a major reason we’re seeing such comparatively low foreclosure numbers is precisely because homeowners have this unprecedented amount of equity cushioning them. It’s like having a financial safety net that simply didn’t exist for millions of people last time around.

Molly Boesel from CoreLogic backs this up with some interesting data about delinquency rates – those are people who are behind on their payments but haven’t yet hit foreclosure. She notes that U.S. mortgage delinquency rates have remained really healthy, with the overall rate basically unchanged from last year and serious delinquencies sitting at historic lows. Even more telling, borrowers who are in the later stages of being behind on payments are finding alternatives to just defaulting on their loans. That equity is giving them options.

The Real Estate Market Is Inherently Local

Now, here’s something important to keep in mind: while we’re talking about national numbers and trends, real estate is always, always, always a local game. Your specific market might be experiencing slightly different conditions based on what’s happening in your area economically, how the local job market is doing, and what the housing supply situation looks like in your community.

Some regions might see a bit more foreclosure activity because of local economic challenges. Others might be doing even better than the national average. That’s totally normal and to be expected – markets across the country aren’t going to all move in perfect lockstep.

But here’s why the national trends still matter: they tell us about the overall health and structure of the housing market system. And right now, that structure looks fundamentally sound in ways it absolutely did not back in 2007-2008.

What This All Means for You

Let’s get practical for a minute and talk about what this foreclosure situation means depending on where you’re sitting.

If You Currently Own a Home

Take a breath and relax a bit. The data we’re looking at suggests the housing market is operating on pretty stable ground. The overwhelming majority of homeowners are managing their mortgage payments just fine, and chances are you’ve got a decent equity cushion built up that provides some real financial security.

That said, if you are facing financial difficulties – and hey, life happens, no judgment – don’t stick your head in the sand and hope it goes away. Reach out to your mortgage servicer sooner rather than later. You might be surprised at the options available to you. There are also HUD-approved housing counselors out there who can walk you through programs and strategies you might not even know exist. The worst thing you can do is wait until you’re drowning before asking for help.

If You’re Thinking About Buying

The current foreclosure environment is actually a pretty good indicator that you’re not walking into a house of cards waiting to collapse. Now, that doesn’t mean home prices can’t fluctuate – they absolutely can and do – but the market isn’t showing the kind of systemic distress that preceded the last crash.

One thing to keep in mind though: because foreclosure rates are so low, there isn’t much distressed property inventory out there. If you were hoping to snag a foreclosure deal, you might find pickings pretty slim depending on your market. But overall market stability is usually a better foundation for making a major purchase decision anyway.

If You’re Just Trying to Make Sense of the Market

Whether you’re an investor, a market watcher, or just someone who likes to stay informed about economic trends, view these foreclosure numbers as one piece of the puzzle – and a pretty encouraging piece at that. Combined with the strong equity positions most homeowners enjoy and the much more responsible lending practices in place today, we’re looking at a market structure that’s significantly more resilient than what existed before the last crisis.

Does that mean nothing can ever go wrong? Of course not. Economic cycles are natural, and various factors could push foreclosure rates up or down over time. But the fundamental architecture of today’s housing market is just built differently than it was back then.

Context Matters More Than Clickbait

Look, I get why those scary headlines exist. Drama sells. Fear gets clicks. An article titled “Foreclosures Surge to Crisis Levels!” is going to get way more attention than “Housing Market Continues Operating Within Normal Parameters.” That’s just the reality of how media works in our attention-economy world.

But here’s the problem: context matters, and those headlines usually strip away all the context that would help you actually understand what’s happening. A 7% increase sounds absolutely terrifying until you realize we’re talking about an increase from historically low levels. It’s like if I told you skateboarding injuries in my town increased 100% – sounds like a skateboarding epidemic, right? Less scary when you find out it went from one injury last year to two this year.

The media knows that steady, stable market conditions don’t generate the same engagement as crisis narratives. Unfortunately, that can really warp people’s perception of reality, especially if you’re relying primarily on news headlines to understand market conditions.

The Foundation Is Solid

Today’s housing market is built on some pretty strong fundamentals that didn’t exist during the last cycle:

Stricter lending standards mean borrowers are more qualified and better able to sustain their payments over time. The days of lending to anyone with a pulse are thankfully behind us.

Significant homeowner equity provides a crucial safety net that lets people sell rather than face foreclosure when financial hardship hits.

Available support programs give homeowners and lenders tools to work through temporary difficulties without immediately jumping to foreclosure proceedings.

Strong demographic trends – particularly millennials hitting their prime home-buying years – continue to support housing demand and property values.

Better economic fundamentals – while not perfect, employment levels remain relatively strong, and many homeowners locked in low rates that make their payments manageable even in tighter times.

None of this makes the market bulletproof, but it does create a foundation that can weather normal economic ups and downs without collapsing.

Don’t Let Fear Drive Your Decisions

Here’s what it all comes down to: yes, foreclosures have increased recently. But that increase is coming from abnormally low pandemic-era levels, and we’re still nowhere near the crisis numbers we saw during the housing crash. In fact, we’re not even back to normal pre-pandemic levels yet.

Here’s what it all comes down to: yes, foreclosures have increased recently. But that increase is coming from abnormally low pandemic-era levels, and we’re still nowhere near the crisis numbers we saw during the housing crash. In fact, we’re not even back to normal pre-pandemic levels yet.

The housing market has fundamentally changed since the last crisis. Better lending practices, substantial homeowner equity, and various support mechanisms have created a much more stable environment. While challenges always exist and no market is immune to economic pressures, the current foreclosure data suggests we’re operating from a position of relative strength rather than systemic weakness.

If you’re a homeowner feeling anxious about those headlines, remember that the vast majority of homeowners are doing just fine. If you’re struggling, reach out for help – you have more options than you might think. If you’re considering buying, don’t let fear of a crash that isn’t actually happening keep you from making sound decisions.

And if you really want to understand what’s happening in your specific market? Talk to a local real estate professional who knows the ins and outs of your area. They can help you separate the actual facts from the fear-mongering and make decisions based on real data rather than sensationalized headlines.

Because at the end of the day, in real estate like in so many areas of life, the most dramatic headlines aren’t always – or even usually – the most accurate representations of reality. The numbers tell a much less scary, much more stable story than those clickbait titles would have you believe.