With everything feeling more expensive these days, it’s natural to worry about how rising costs might impact the housing market. Many people are concerned that high prices and tighter budgets could cause more homeowners to fall behind on their mortgage payments, leading to a wave of foreclosures.

But before you start worrying about a housing market crash, here’s a look at what’s really happening. And the good news is: the latest foreclosure data shows there’s no wave on the horizon.

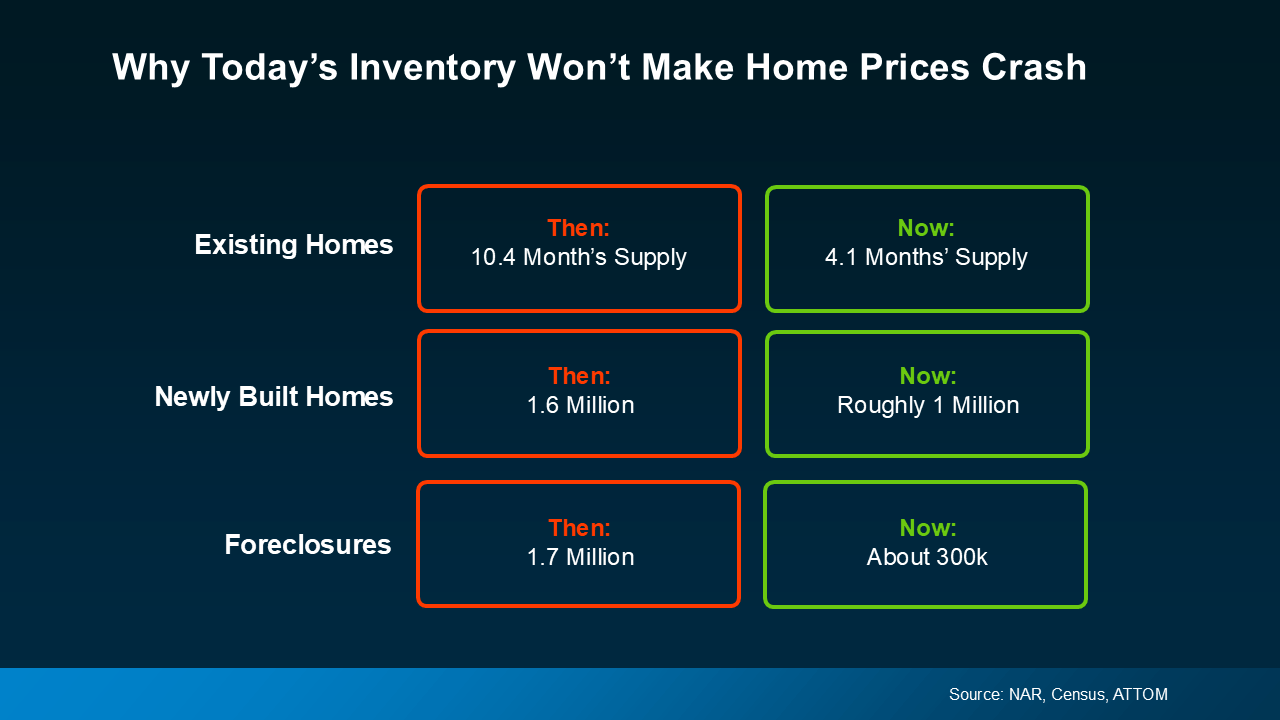

How Today’s Market Is Different from 2008

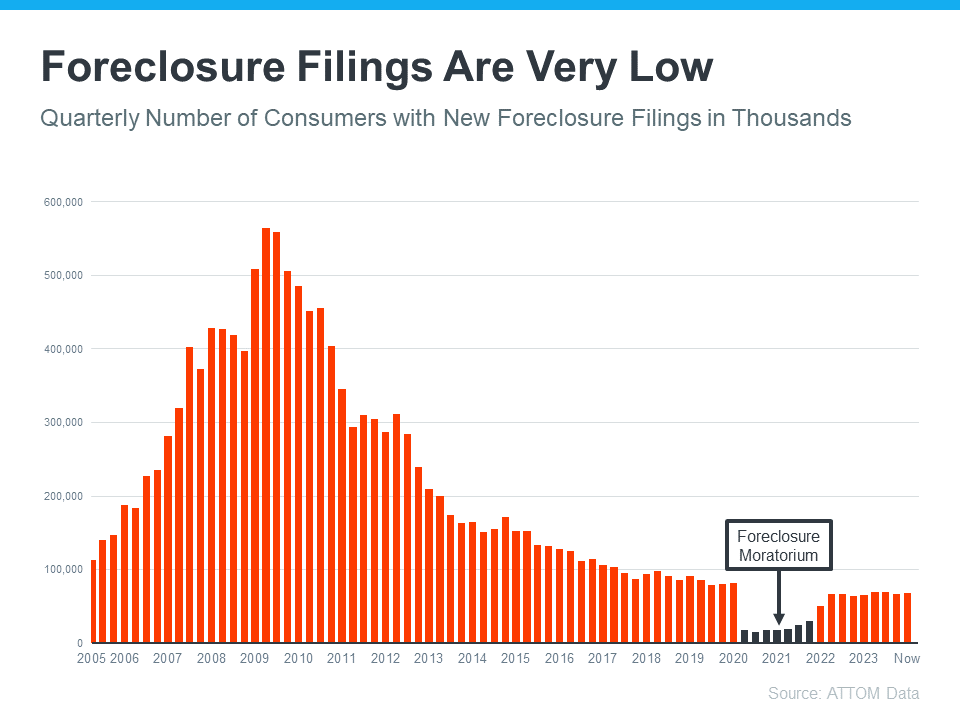

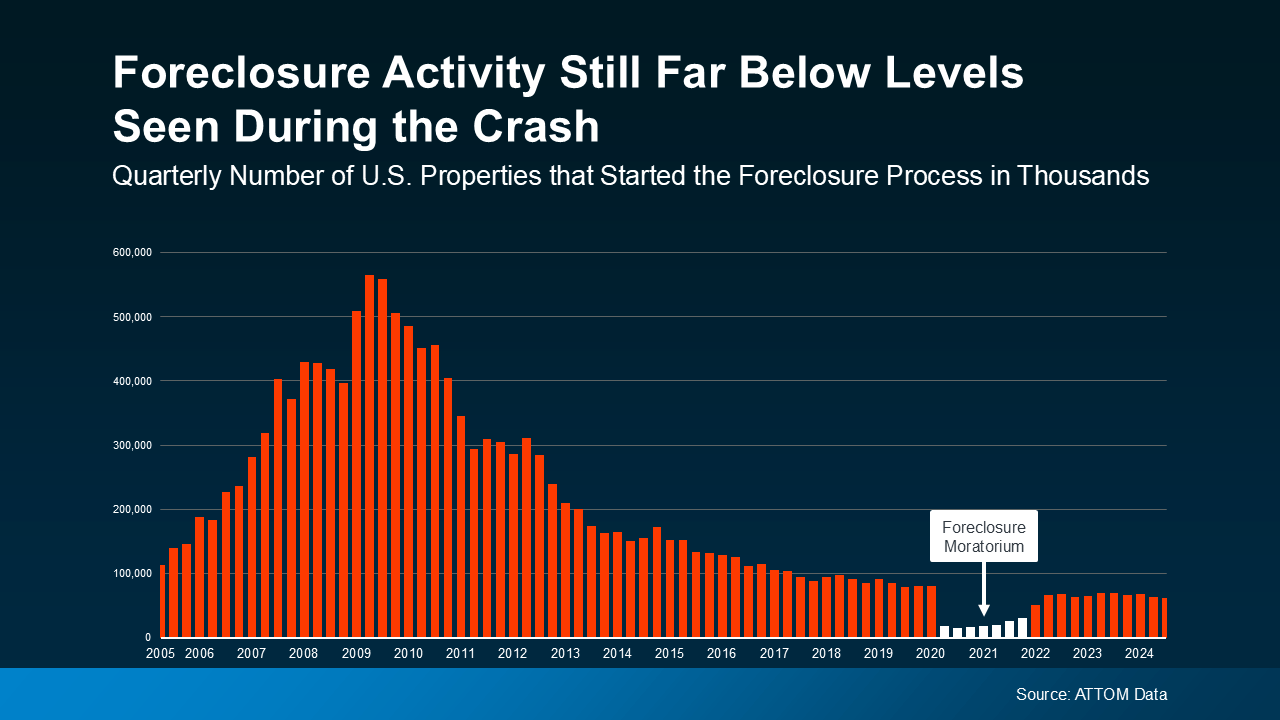

Let’s ease those fears by looking at the bigger picture. The graph below uses research from ATTOM, a property data provider, to show that the number of homeowners starting the foreclosure process is nowhere near what we saw coming out of 2008. Back then, there was a big spike in how many foreclosures were happening. Today, the number is much lower – it’s even dropped some in the latest report. There’s a big difference between what’s happening now, and what happened when the housing market crashed (see graph below):

Just in case you’re wondering why the number of foreclosure filings has ticked up slightly since 2020 and 2021, here’s what you need to know. During those years, there was a moratorium (shown in white) designed to help millions of homeowners avoid foreclosure in challenging times. That’s why the numbers for just a few years ago were so incredibly low. If you look further back, it’s clear overall foreclosure filings are down significantly.

Just in case you’re wondering why the number of foreclosure filings has ticked up slightly since 2020 and 2021, here’s what you need to know. During those years, there was a moratorium (shown in white) designed to help millions of homeowners avoid foreclosure in challenging times. That’s why the numbers for just a few years ago were so incredibly low. If you look further back, it’s clear overall foreclosure filings are down significantly.

And if you’re wondering: how are there fewer foreclosures today, even when the cost of living has gotten so pricey? Here’s your answer. One of the main reasons is that homeowners today have a lot more equity built up in their homes than they did back in 2008. As an article from Bankrate explains:

“In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes.”

This equity acts like a safety net and is allowing many homeowners to avoid going into foreclosure if they’re facing financial hardships. Even if someone is struggling to make their monthly payments, they may be able to sell their home and avoid foreclosure altogether. This is a far cry from the conditions during the crash when homeowners owed more on their mortgages than their homes were worth.

What’s Ahead for the Housing Market

It’s true that today’s higher cost of living across the board is a challenge for many people right now. But this doesn’t mean we’re heading for a surge in foreclosures.

The equity cushion that people have is helping to keep foreclosure filings low. Today’s homeowners have more options to avoid going into foreclosure.

Bottom Line

Yes, everyday costs for gas and food have gotten more expensive—but that doesn’t mean the housing market is on the brink of another foreclosure crisis. Data shows the market is far from a foreclosure wave. Homeowners today are in a much stronger financial position than they were during the 2008 crash, thanks to significant equity.

Some consumers will simply wait it out before they make their purchase decision.

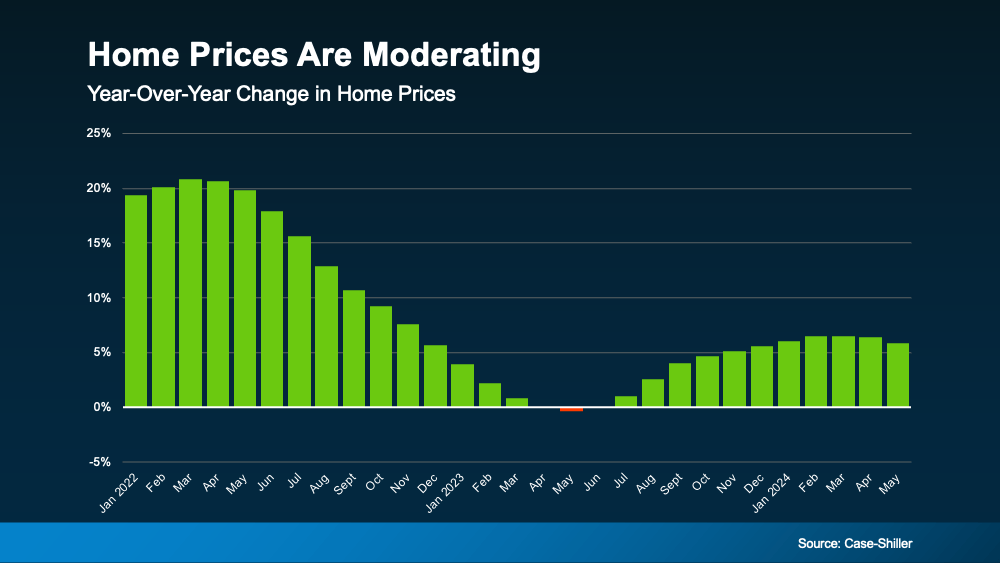

Some consumers will simply wait it out before they make their purchase decision. Home Prices

Home Prices

2. How Many Jobs the Economy Is Adding

2. How Many Jobs the Economy Is Adding