(Updated 4/21/26)

Every few months, a national headline pops up about foreclosures rising. The numbers get shared on social media without context, and the comments fill up with people asking whether 2008 is about to repeat itself. If you own a home in Memphis, Germantown, or Collierville, that kind of coverage can make your stomach drop.

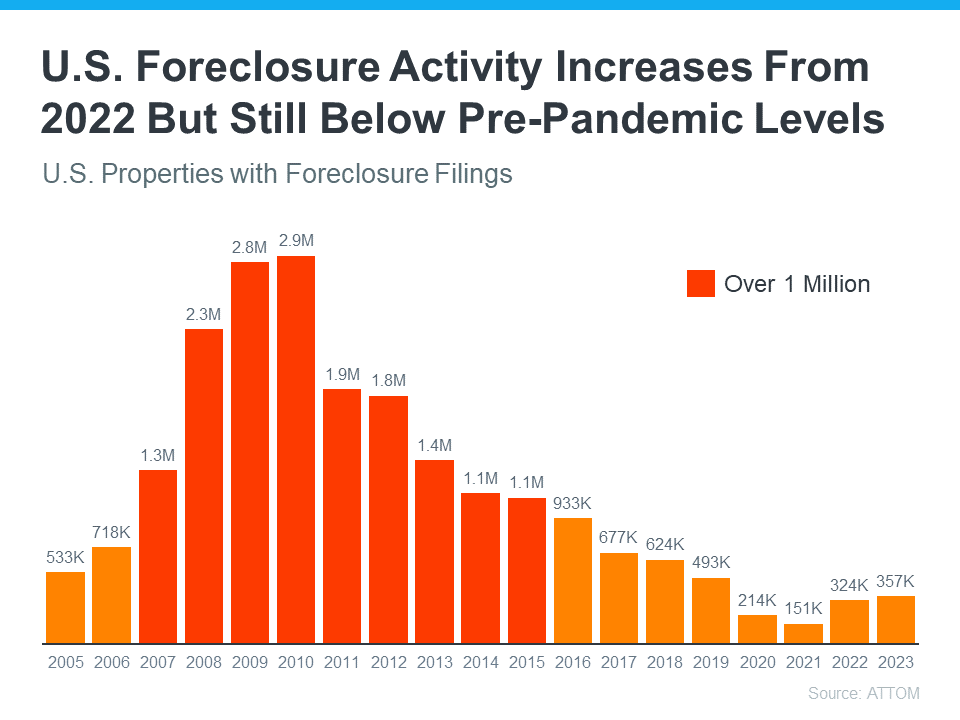

But foreclosure rates in 2026 tell a very different story than those headlines suggest. The data from the first half of 2025, which is the most recent full reporting period available, showed that only about 1 in 758 homes nationwide had any kind of foreclosure filing. That’s 0.13%. Compare that to the 2010 peak, when 1 in 45 homes was in foreclosure. We’re not in the same universe as the housing crisis, let alone the same neighborhood.

So why do the headlines keep coming? And what should you actually think about if you’re buying a home or already own one in the Memphis area? Let’s walk through the numbers and separate the noise from what matters.

Foreclosure filings rose, but from where

The statistic that fuels most of the panic is real: foreclosure starts jumped about 7% in the first half of 2025. That sounds alarming until you understand the baseline.

During the pandemic, the federal government put moratoriums in place that essentially froze all foreclosure activity. Filings dropped to artificially low levels that had never been seen before. When those protections expired, the numbers started climbing back toward normal. A 7% increase on a historically low number is still a historically low number.

Rick Sharga of CJ Patrick Company put it plainly: current foreclosure activity is running at roughly 60% of normal pre-pandemic levels. Not 60% above normal. Sixty percent of normal. The system is still well below where it sat during years that nobody considered problematic.

Think of it this way. If your neighborhood pool usually has 100 swimmers on a Saturday, and one summer it dropped to 30 because of a closure, and the next year it climbed back to 60, nobody would call that a swimming crisis. They’d call it a slow recovery. That’s what’s happening with foreclosures.

Memphis housing market foreclosures in context

For the Memphis metro specifically, the situation tracks closely with national trends. Memphis has historically had slightly higher foreclosure rates than some of the surrounding suburbs, partly due to the city’s larger share of investor-owned properties and older housing stock. But the same forces keeping national foreclosures low apply here too.

In Germantown and Collierville, where homeownership rates are high and median incomes are strong, foreclosure activity remains minimal. These are neighborhoods where homeowners tend to have significant equity cushions and stable employment, both of which make foreclosure much less likely even if someone hits a rough patch.

The Memphis metro didn’t see the same wild price spikes that hit Austin or Boise during 2021 and 2022, which means it also didn’t see the same correction risk. Steadier appreciation means fewer homeowners ended up underwater, which is the condition that actually triggers most foreclosure spirals.

Why 2026 isn’t 2008

People who lived through the last housing crash have every right to be wary. That experience left scars. But the conditions that caused the 2008 crisis simply don’t exist in today’s market.

Lending standards changed completely

Before the crash, lenders were handing out mortgages to anyone with a pulse. No income verification, no job verification, no assets required. The industry literally called them NINJA loans: No Income, No Job, no Assets. People bought homes they could never afford, often with adjustable-rate mortgages that started low and then spiked, making the monthly payment impossible.

That playbook is gone. The Dodd-Frank reforms that followed the crisis created strict underwriting requirements. Today, you have to document your income, verify your employment, and prove you can handle the payments. Lenders stress-test your ability to pay before they approve the loan. The mortgages being written right now are fundamentally sounder than anything from 2005 to 2007.

Homeowner equity is a massive buffer

This is the part most foreclosure headlines ignore entirely. American homeowners are sitting on record levels of equity. When someone has $100,000 or $200,000 in equity in their home, they don’t just let it go to foreclosure. They sell.

Selling before foreclosure is the rational move when you have equity, and most homeowners do. Even someone who loses a job or goes through a divorce will almost always list the house, pocket the equity, and move on rather than let the bank take the property. That option didn’t exist for millions of homeowners in 2008 because their homes were worth less than they owed.

In the Memphis area, anyone who bought before 2022 has likely accumulated meaningful equity through both appreciation and principal paydown. That equity acts as a safety net. It doesn’t prevent financial hardship, but it gives homeowners a way out that doesn’t involve foreclosure.

Support programs exist now that didn’t before

During the pandemic, the federal government learned a lot about how to keep people in their homes. Forbearance programs, loan modification options, and state-level assistance programs all expanded. Many of those programs or their successors still exist in some form.

A homeowner who falls behind on payments in 2026 has more options available than a homeowner in the same situation in 2007. Servicers are better trained to work with borrowers. The system, while imperfect, is set up to find alternatives to foreclosure rather than fast-track it.

Are foreclosures increasing or normalizing

This is the honest answer: yes, foreclosure numbers are going up. And that’s expected.

We spent several years at artificial lows. The pandemic paused the normal foreclosure process entirely for a period. As that pause works its way through the system, filings are returning toward typical levels. They haven’t reached typical levels yet, and most analysts don’t expect them to overshoot.

Molly Boesel at CoreLogic has noted that serious delinquency rates remain near historic lows. Serious delinquencies, meaning homeowners who are 90 or more days behind on their mortgage, are the leading indicator of foreclosure. When that number stays low, large-scale foreclosure waves don’t follow.

The delinquency picture looks stable right now. Not perfect, because no market ever is. But there’s no sign of the cascading defaults that preceded the 2008 collapse. The mortgages being serviced today are held by borrowers who qualified under strict standards, and most of them have equity to fall back on.

What Memphis buyers should know

If you’ve been watching the market from the sidelines, worried that a wave of foreclosures might crash prices, the data doesn’t support that fear. That doesn’t mean prices can’t fluctuate. Markets move for all kinds of reasons. But a 2008-style crash driven by foreclosures would require conditions that simply aren’t present.

You’re not going to see a flood of distressed properties hitting the Memphis market and driving prices down 30%. The math doesn’t work for that outcome when foreclosure rates are this low and equity levels are this high.

What you might see is more inventory in general, which is a good thing for buyers. More homes for sale means more choices, less pressure to bid over asking, and better odds of finding a home that fits your needs and budget. That increased inventory comes from the lock-in effect easing and more homeowners choosing to sell, not from banks repossessing houses.

If you’re looking in Germantown, Collierville, or East Memphis, the spring 2026 market is shaping up to offer more options than buyers have had in several years. That’s worth paying attention to.

What homeowners should know

If you already own a home in the Memphis area, the foreclosure data should be reassuring, not alarming. Your home’s value isn’t about to crater because of a foreclosure wave that isn’t coming.

Memphis real estate market stability has held up well through the post-pandemic adjustment period. Prices moderated after the 2021-2022 run-up, which was healthy and expected. But the foundation underneath the market, strong employment, limited inventory, steady population growth in the suburban corridor, remains solid.

If you’re considering selling your home, the current market conditions are workable. You’re not competing against a glut of foreclosed properties being dumped at discount prices. You’re selling into a market where supply is still below historical norms and demand from relocating families, first-time buyers, and investors continues to support pricing.

If you’re not selling and just want peace of mind, here it is: homeowners with a fixed-rate mortgage, reasonable monthly payments, and equity in their home are in a strong position right now. The fact that foreclosure filings ticked up from pandemic-era floors doesn’t change that.

How to read foreclosure headlines going forward

The foreclosure stories won’t stop. They get clicks, and the numbers will keep rising as activity normalizes. Every quarter, someone will publish a report showing a percentage increase, and the headlines will strip out all the context.

When you see those stories, ask two questions. First, what’s the baseline? A 10% increase from an all-time low is very different from a 10% increase from a normal level. Second, what’s the absolute number? The percentage change grabs attention, but the actual rate of foreclosure, currently well under 1%, tells you whether this is a real problem or a statistical footnote.

For Memphis specifically, keep an eye on local inventory and median home prices rather than national foreclosure headlines. Those two numbers will tell you far more about what’s happening in your neighborhood than a report about foreclosure filings across all 50 states.

You can always check the Reid Realtors blog for local market updates that put the national data into Memphis context.

Stability runs deeper than headlines

It’s natural to worry when headlines use words like “surge” and “spike” around foreclosures. The 2008 crash is still recent enough that the emotional memory is strong. But emotional memory and market data are telling very different stories right now.

Foreclosure rates in 2026 are a fraction of what they were during the crisis. Lending standards are tighter. Homeowner equity is at record levels. Delinquency rates are healthy. The gap between today’s market and the conditions that created 2008 is enormous.

None of this means the housing market is risk-free. No market ever is. Interest rates, employment shifts, and local economic changes can all affect home values. But a foreclosure-driven collapse? The numbers just don’t support it. Not nationally, and not in the Memphis area.

Talk to a local expert

Whether you’re thinking about buying your first home, considering a move across the Memphis metro, or just trying to understand what your current home is worth, the best move is a conversation with someone who tracks this market daily. National headlines don’t capture what’s happening on the ground in your neighborhood.

Get in touch with our team at Reid Realtors and we’ll walk you through the numbers that matter for your specific situation. No panic, no hype, just honest local market knowledge.