As you think ahead to your own move, you may have noticed some houses sell within days, while others linger. But why is that? As Redfin says:

“. . . today’s housing market has been topsy-turvy since the pandemic. Low inventory (though rising) and high prices have created a strange mix: Some homes are flying off the market, while others sit for weeks.”

That may leave you wondering what you should expect when you sell. Let’s break it down and give you some actionable tips on how to make sure your house is one that sells quickly.

Homes Are Still Selling Faster Than Pre-Pandemic

The first thing you should know is that, in most markets, things have slowed down a little bit. While you may remember how quickly homes sold a few years ago, that’s not what you should expect today.

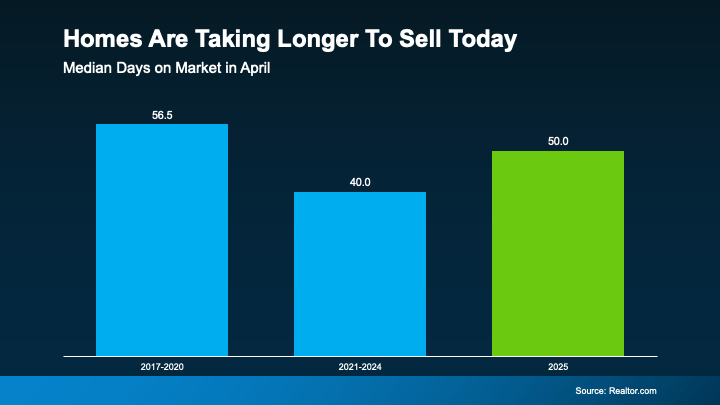

Now that inventory has grown, according to Realtor.com, homes are taking a bit longer to sell in today’s market (see graph below):

But before you get hung up on the ten-day difference compared to the past few years, Realtor.com will help put this into perspective:

But before you get hung up on the ten-day difference compared to the past few years, Realtor.com will help put this into perspective:

“In April, the typical home spent 50 days on the market . . . This marks the 13th straight month of homes taking longer to sell on a year-over-year basis. Still, homes are moving more quickly than they did before the pandemic . . .”

By this comparison, if your house does take a little more time to sell this year, it’s not really a concern. It’s actually still faster than the norm. Plus, it gives you a bit more time to find your next home, which is welcome relief when you’re trying to move, too.

Just remember, some homes sell in less time than this. Some take even longer. So, what’s the real difference? Why do some homes attract eager buyers almost instantly, while others sit and struggle?

It comes down to having the right agent and strategy. Here are a few tips you need to know.

1. Price It Right

One of the biggest reasons homes sit on the market is overpricing. Many sellers want to shoot for a higher price, thinking they can lower it later – but that backfires by turning buyers away.

What to do: Work with an agent to make sure your house is priced right. They’ll analyze recent comparable sales (what other homes have sold for recently in your area), so you know you’re pricing appropriately for today’s market and what buyers are willing to pay. As Chen Zhao, Economic Research Lead at Redfin, explains:

“My advice to sellers is to price your home fairly for the shifting market; you may need to price lower than your initial instinct to sell quickly and avoid giving concessions.”

2. Focus on the First Impression

A messy yard or a house that needs paint? It’ll turn buyers off. Since buyers decide within seconds whether they like a home, a good first impression is key.

What to do: Outside, clean up your front yard, tidy up your landscaping, power wash walkways, and add fresh mulch. Inside, declutter and depersonalize. And consider minor touch-ups like repainting in a neutral tone. Your agent will offer advice on what to tackle.

3. Strong Marketing & High-Quality Listing Photos

If your listing or your photos don’t look professional, you could have trouble drawing in buyers who think you’re trying to cut corners.

What to Do: Instead, lean on your agent’s skills, expertise, and resources. They’ll help you make sure you have:

- High-resolution listing photos showing the home in its best light.

- Detailed descriptions that highlight differentiating features of your house.

- Your listing on multiple platforms, including major real estate sites and social media.

4. The Location of the Home

You may have heard the phrase “location, location, location” when it comes to real estate. And there’s definitely some truth to that. Homes in highly sought-after neighborhoods tend to sell faster.

What to do: While you can’t change where your house is located, your agent can highlight the best features of your neighborhood or community in your listing. By showcasing what’s great about your area, they can help draw buyers into what life would look like in your house.

Bottom Line

Homes that sell quickly don’t necessarily have better features – they have better agents and a better strategy.

Are you thinking about selling? Connect with an agent to talk about how to get your home sold quickly and for top dollar.

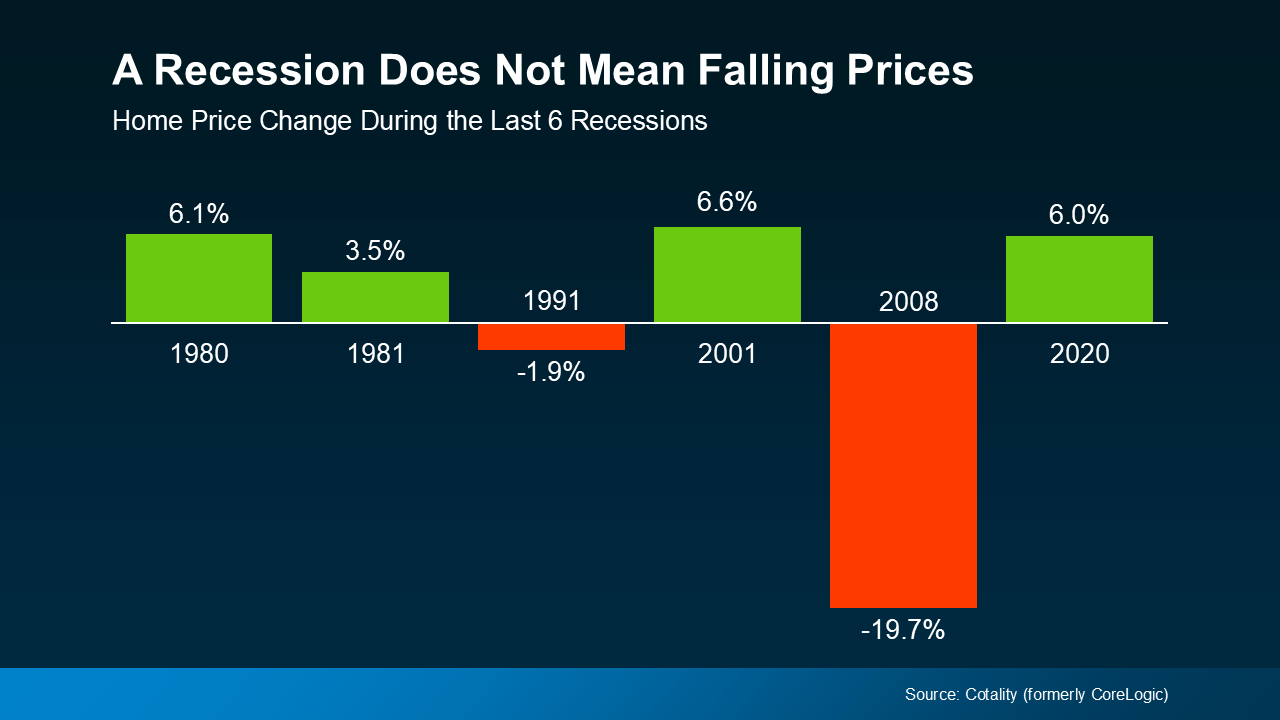

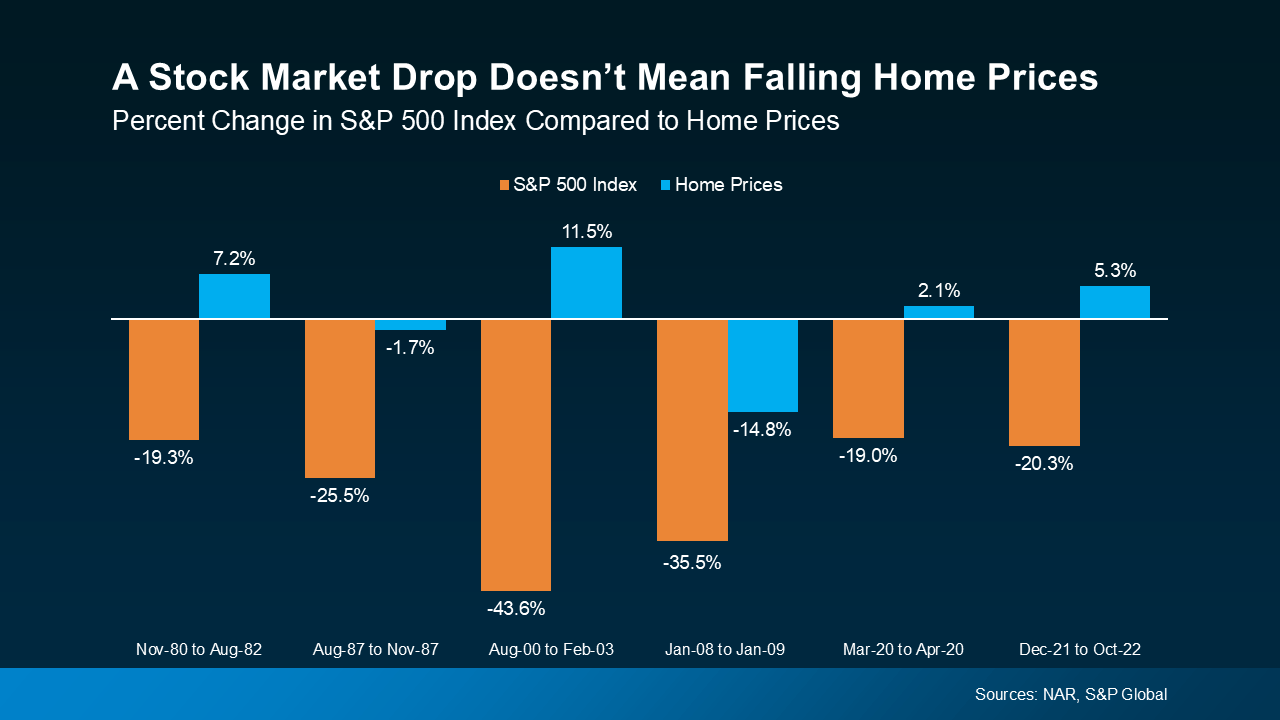

Even when the stock market falls more substantially, home prices don’t always come down with it.

Even when the stock market falls more substantially, home prices don’t always come down with it.

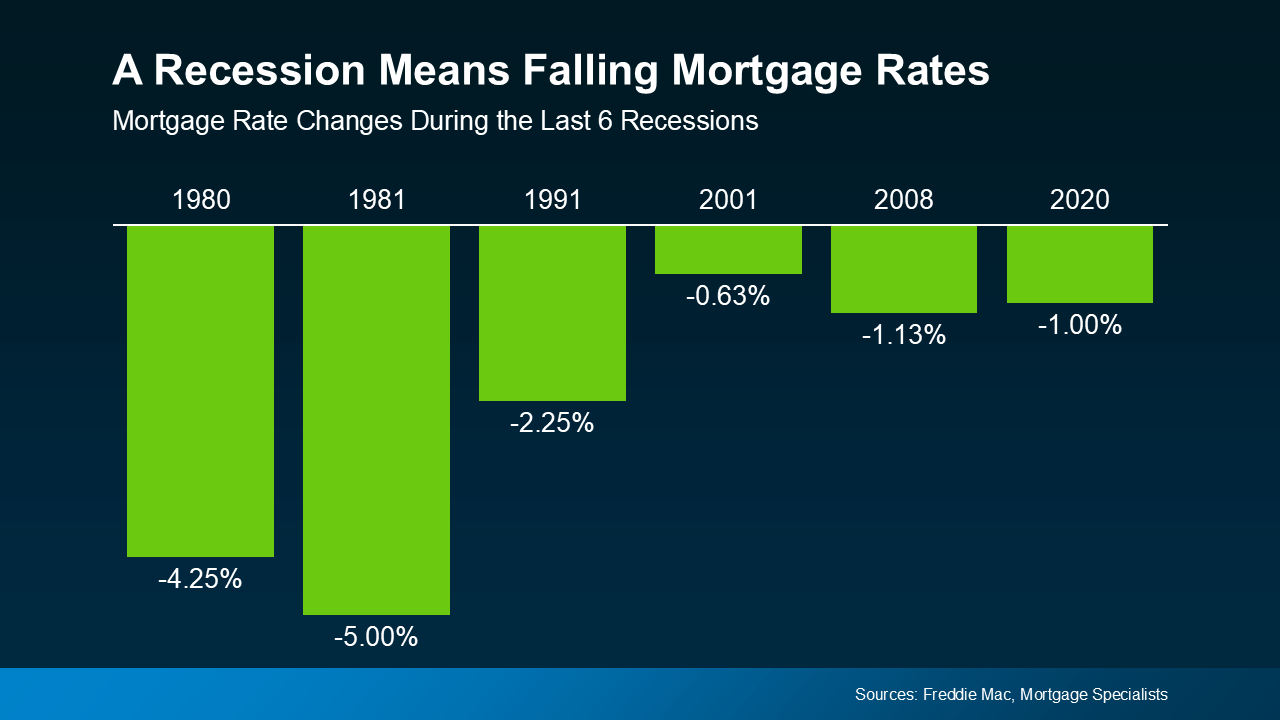

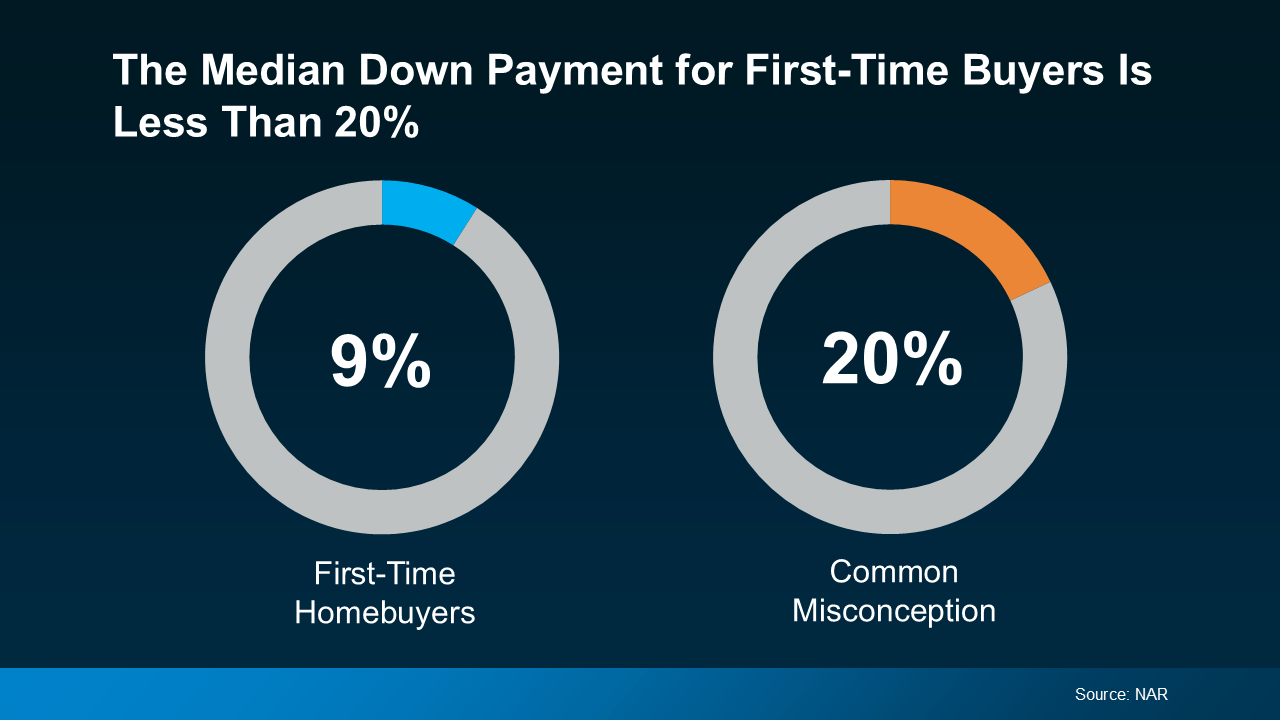

The takeaway? You may not need to save as much as you originally thought.

The takeaway? You may not need to save as much as you originally thought.