If you have questions about what to expect for the rest of the year, connect with a local agent to have a conversation about what it means for you and your plans.

When you decide to buy your first home, you may come across a number of terms and conditions you’re not familiar with. While you may have a general idea of what an inspection is, maybe you’re not sure why you need one or how it’s different from an appraisal. To keep it simple, here’s an explainer of each one and what they mean for you as a homebuyer.

Home Inspection

Once you’re under contract on a home you’d like to buy, getting an inspection is a key part of the process. An inspection gives you a clear idea of the safety and overall condition of the home – which is important for such a big transaction. As a recent Realtor.com article explains:

“A home inspection is something that protects your financial interest in what will likely be the largest purchase you make in your life—one in which you need as much information as possible.”

If anything is questionable in the inspection process – like the age of the roof, the state of the HVAC system, or just about anything else – you have the option to discuss and negotiate any potential issues or repairs with the seller before the transaction is final. And don’t worry – you don’t have to go through that process alone. Your real estate agent will be your advocate and negotiate with the seller for you.

Home Appraisal

While the inspection tells you about the current state of the house, an appraisal gives you its value. Bankrate explains:

“When buying or selling a home, an appraisal verifies that the sale price of the home is in line with fair market value. This ensures the homebuyer doesn’t pay more than the home is worth, and the mortgage lender doesn’t lend more than it is worth.”

Regardless of what you’re willing to pay for a house, if you’ll be using a mortgage to fund your purchase, the appraisal protects you from overpaying and the bank from lending you more than the home is worth.

And if there’s ever any confusion or discrepancy between the appraisal and the agreed-upon price in your contract, your trusted real estate professional will help you navigate any additional negotiations to try to close the gap.

Bottom Line

The inspection and the appraisal are different but equally important steps when buying a home – and you don’t need to manage them by yourself. Connect with an agent today so you have expert guidance from start to finish.

Should you buy a home now or should you wait? That’s a big question on many people’s minds today. And while what timing is right for you will depend on a lot of other personal factors, here’s something you may not have considered.

If you’re able to buy at today’s rates and prices, it may be better to focus on time in the market, rather than timing the market.

The Downside of Trying To Time the Market

Trying to time the market isn’t a good strategy because things can change. Here’s an example. For the better part of this year, projections have said mortgage rates will come down. And while experts agree that’s still what’s ahead, shifts in various market and economic factors have pushed back the timing of when that’ll happen. Here’s how that’s impacted homebuyers who’ve been sitting on the sidelines. As U.S. News says:

“Those who put off buying a home during the past few years as they were holding out for lower mortgage rates have been left out of the market . . . mortgage rates have stayed higher for longer than previously expected, keeping monthly housing payments elevated. In other words, affordability didn’t improve for those who chose to wait.”

This is why timing the market may not pay off if you’re ready and able to buy now.

The Proof Is in the Pudding: How Homeowners Benefit from Rising Home Prices

Delaying your plans also means missing out on the equity you’d gain if you went ahead with your purchase today. And the potential equity gains that are at stake may surprise you.

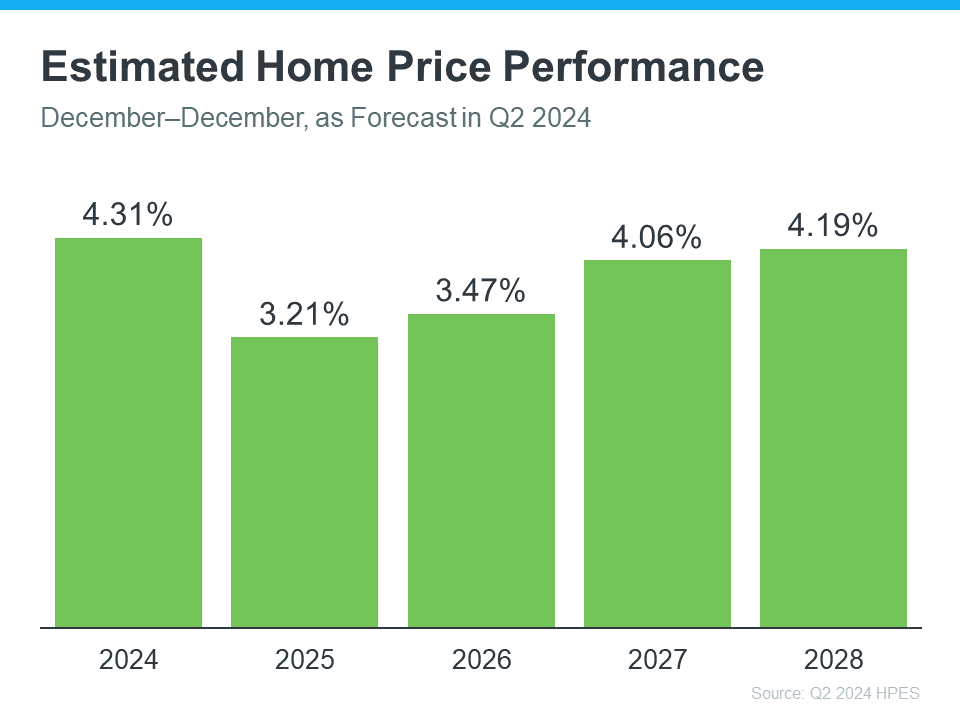

Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2028 (see the graph below):

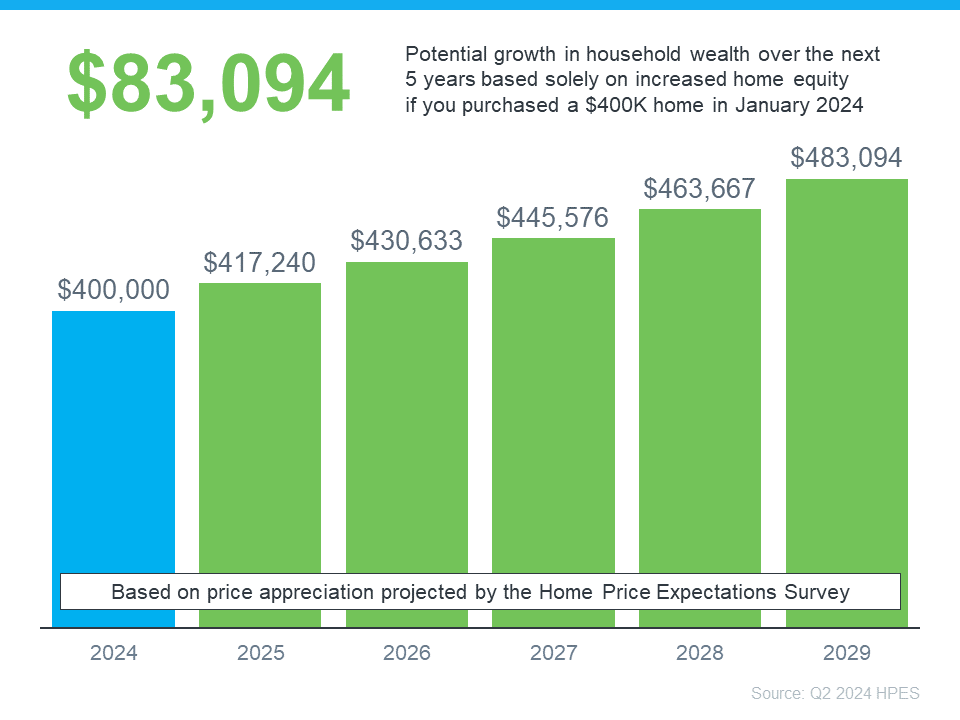

To give these numbers context, let’s take a look at a breakdown of what you stand to gain once you buy. The graph below uses a typical home’s value to show how a home could appreciate over the next few years using those HPES projections:

In this example, let’s say you went ahead and bought a $400,000 home at the beginning of this year. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number.

This data helps paint the picture of why time in the market really matters.

The Advice You Need To Hear If You’re Ready and Able To Buy Now

Prices are expected to continue climbing, just at a more moderate pace. And while a moderate rise in prices may not be fun for you now, once you own a home, that growth will be a huge perk. That’s the time in the market piece.

Sure, you could try timing the market, but the equity you’ll be missing out on in the meantime is something to seriously consider. If you’re ready and able to buy now, you have to decide: is it really worth waiting?

Rather than focusing on timing the market. It’s better to have time in the market.

As U.S. News Real Estate sums up:

“There’s never a one-size-fits-all answer to whether now is the right time to buy a home. . . . There’s also no way to predict precisely what the market will do in the near future . . . Perfectly timing the market shouldn’t be the goal. This decision should be determined by your personal needs, financial means and the time you have to find the right home.”

Bottom Line

If you’re debating whether to buy now or wait, remember it’s time in the market, not timing the market. And if you want to get the ball rolling and set yourself up for those big equity gains, connect with an agent to make it happen.

You want your house to sell fast. And you may be wondering how long the whole process is going to take. One way to get your answer? Work with a local real estate agent.

They have the expertise to tell you how quickly homes are selling in your area and what’s impacting timelines for other sellers. That way you have realistic expectations and can work together to come up with a plan that’s based on today’s market.

Here’s a high-level overview of just one of the factors a great agent will walk you through – the supply of homes for sale and how that impacts your process.

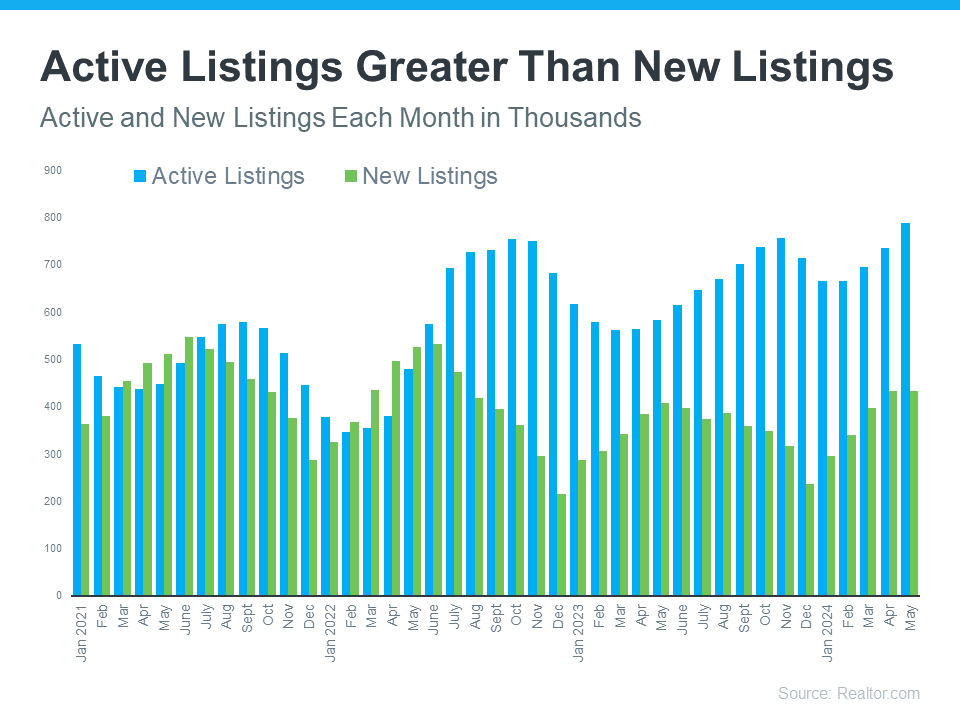

The Growing Supply of Homes for Sale

Over the past few months, the number of homes for sale has increased. This is good news when you move because it means you’ll have more options as you search for your next home. But it also means buyers have more to choose from, so if your house doesn’t stand out – it may take a bit longer to sell.

Available inventory is made up of new listings (homes that were just put up for sale) and active listings (homes that were already on the market but haven’t sold yet). And if you look at data from Realtor.com you can see a good portion of the recent growth is from active listings that are sticking around (see the blue bars in the graph below):

How It’s Impacting Listings Today

Think of the homes on the market like loaves of bread for sale in a bakery. When a fresh batch of bread is put out, everyone wants the newest and hottest one. But if a loaf sits there too long, it starts to get stale, and fewer people want to buy it.

The same goes for homes. New listings are the freshest and most sought-after. But if a home isn’t priced correctly, doesn’t show well, or it doesn’t have an effective sales or marketing strategy behind it, it can sit on the market and become less appealing to buyers over time.

An Agent Will Help Your House Stand Out and Sell Quickly

Timing is important to you. You want to get this done, fast. By leaning on a pro, they’ll make sure your listing is fresh and doesn’t stick around long enough to go stale. As the National Association of Realtors (NAR) explains:

“Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home.”

Your agent will factor the recent inventory growth into their plan and create a customized selling strategy for your house. The supply of homes for sale can vary a lot by area. So they’ll do things like share their valuable insights into what’s happening with supply in your market, help you price your home correctly, and create a marketing plan that gets your home noticed.

Don’t let your listing get stale—reach out to a real estate agent today to make sure your listing is fresh and appeals to buyers from the start. It makes a big difference.

Bottom Line

If you want your house to sell fast, you need to work with a pro. Connect with a local agent, so you’ve got someone who understands the current market trends and how to build a strategy around those factors, so your house is set up to sell quickly.

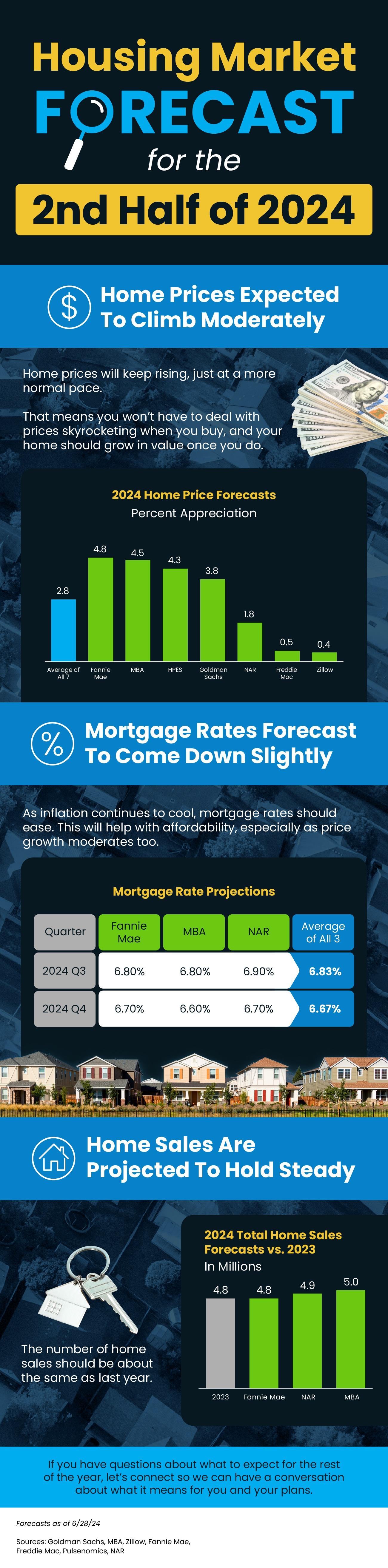

As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home sales.

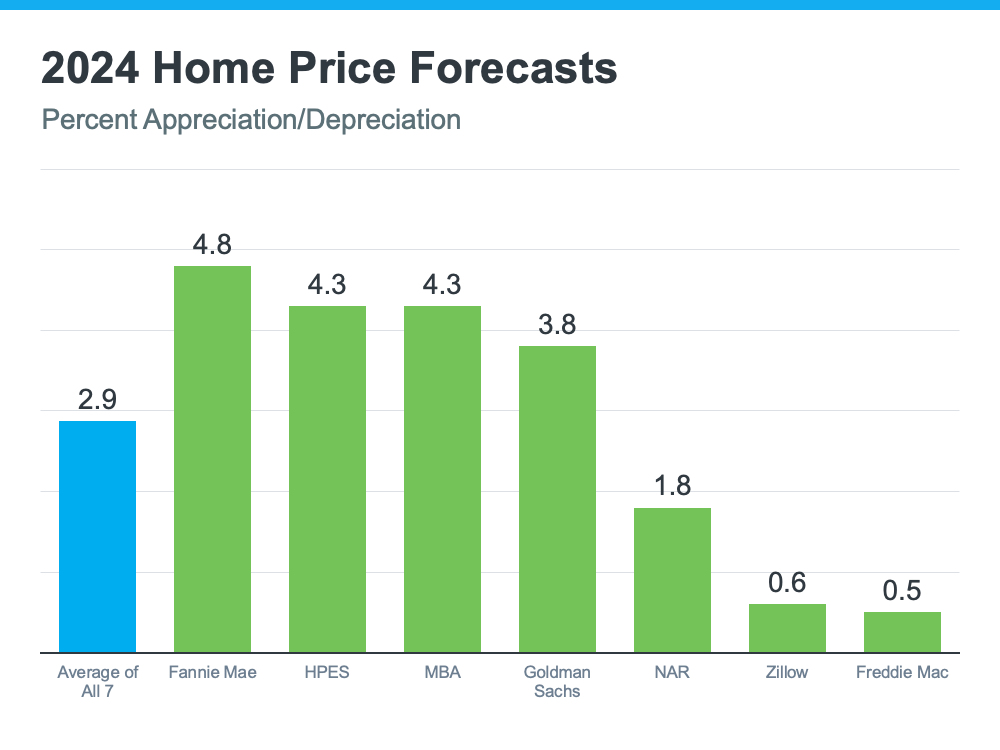

Home Prices Are Expected To Climb Moderately

Home prices are forecasted to rise at a more normal pace. The graph below shows the latest forecasts from seven of the most trusted sources in the industry:

The reason for continued appreciation? The supply of homes for sale. Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), explains:

“One thing that seems to be pretty solid is that home prices are going to continue to go up, and the reason is that we don’t have housing inventory.”

While inventory is up compared to the last couple of years, it’s still low overall. And because there still aren’t enough homes to go around, that’ll keep upward pressure on prices.

If you’re thinking of buying, the good news is you won’t have to deal with prices skyrocketing like they did during the pandemic. Just remember, prices aren’t expected to drop. They’ll continue climbing, just at a slower pace.

So, getting into the market sooner rather than later could still save you money in the long run. Plus, you can feel confident experts say your home will grow in value after you buy it.

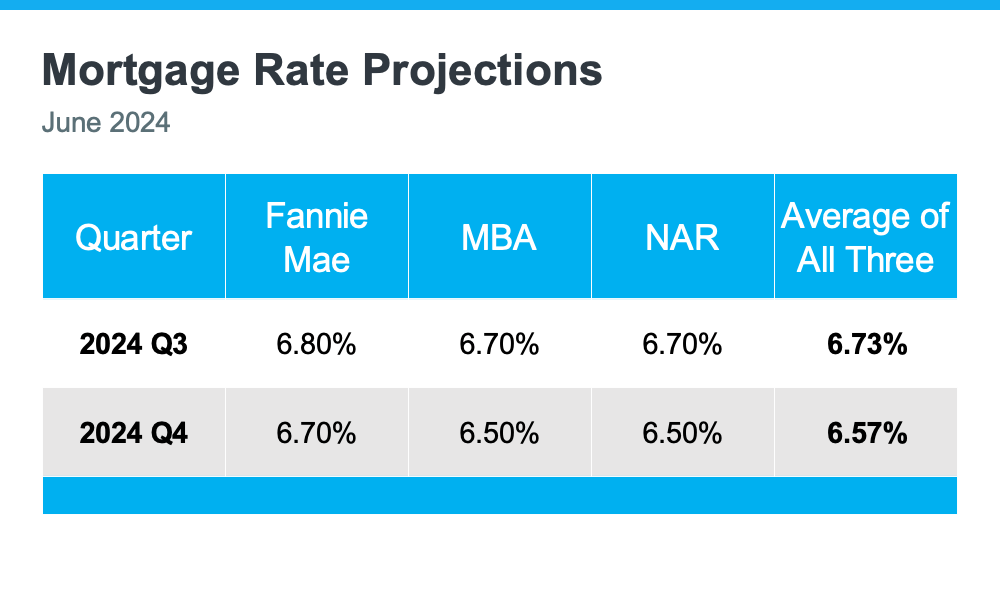

Mortgage Rates Are Forecast To Come Down Slightly

One of the best pieces of news for both buyers and sellers is that mortgage rates are expected to come down a bit, according to Fannie Mae, the Mortgage Bankers Association (MBA), and NAR (see chart below):

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

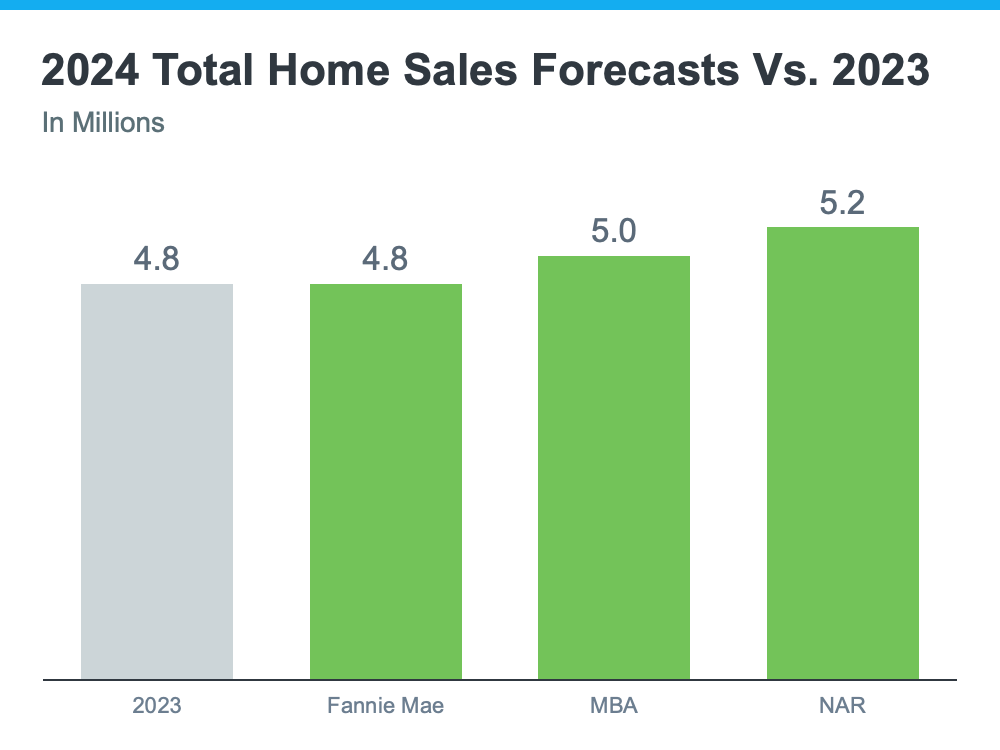

Home Sales Are Projected To Hold Steady

For 2024, the number of home sales will be about the same as last year and may even rise slightly. The graph below compares the 2024 home sales forecasts from Fannie Mae, MBA, and NAR to the 4.8 million homes that sold last year:

The average of the three forecasts is about 5 million sales in 2024 – a small increase from 2023. Lawrence Yun, Chief Economist at NAR, explains why:

“Job gains, steady mortgage rates and the release of inventory from pent-up home sellers will lead to more sales.”

With more inventory available and mortgage rates expected to go down, a few more homes are expected to be sold this year compared to last year. This means more people will be able to move. Let’s work together to make sure you’re one of them.

Don’t take all of this responsibility on. Instead, connect with an agent so you have someone with the knowledge and experience you’ll need on your side.

Summer is officially here and that means it’s the perfect time to start planning where you want to vacation and unwind this season. If you’re excited about getting away and having some fun in the sun, it might make sense to consider if owning your own vacation home is right for you.

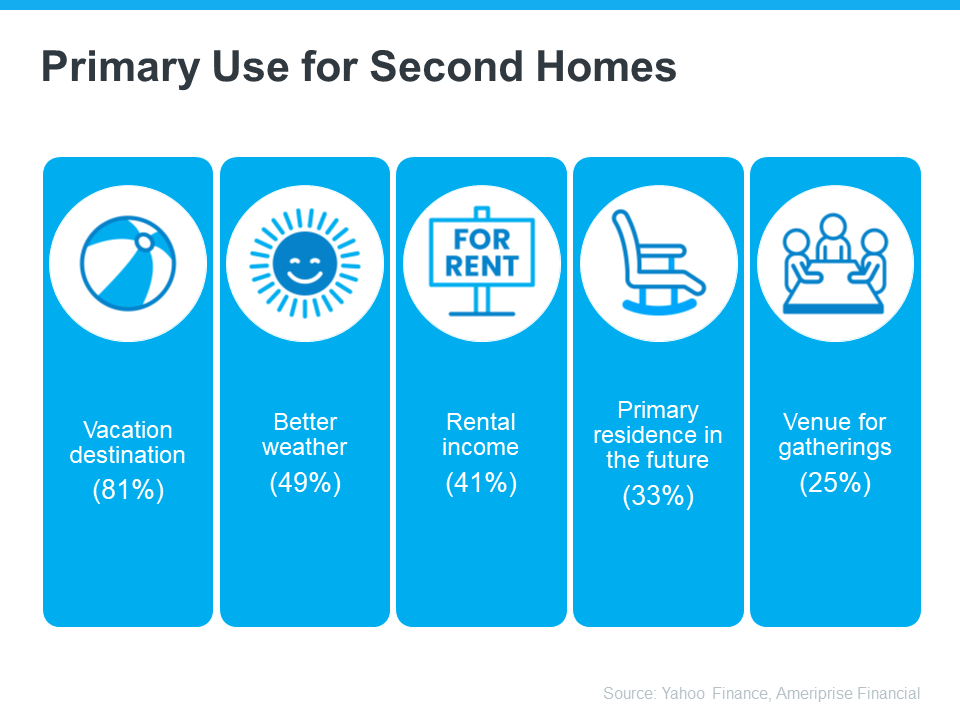

An Ameriprise Financial survey sheds light on why people buy a second, or vacation, home (see below):

Vacation destination or a place to get away from the stresses of everyday life (81%) – Having a second home to use as a vacation spot can be a special place where you go to relax and take a break from your daily routines and stressors. It also means you won’t have to worry about finding somewhere to stay when you go there.

Better weather (49%) – Buying in a place where there may be nicer weather can be a great escape, especially if it’s cold or rainy where you usually live. It lets you enjoy sunny days and warm temperatures, even when it’s not so nice back home.

Rental income (41%) – You can rent it out to other people when you’re not using it, which can help you make some extra money.

Primary residence in the future (33%) – You can eventually move into the home full-time during retirement. That means you can enjoy vacations there now and have a getaway ready for your future.

Having a venue for gatherings with family and friends (25%) – It would be a special spot where you can have parties, regular family trips, and create fun memories.

Ways To Buy Your Vacation Home

And you don’t have to be wealthy to buy a vacation home. Bankrate shares two tips for how to make this dream more achievable for anyone who’s interested:

Buy with loved ones or friends: If you’re okay with sharing the vacation home, you can go in on the purchase price together and pool your resources to make it more affordable.

Put a savings plan in place: This will require patience and persistence but consider adding a vacation home savings plan to your budget and contributing to it monthly.

Finding Your Dream Spot with a Little Help from an Agent

If the idea of basking in the sun at your very own vacation home sounds appealing, you might want to start looking now. Summer’s when everyone’s trying to buy their slice of paradise, so it’s best to start early.

Your first move is to team up with a real estate agent. They know all the ins and outs of the area you want to be in, and which homes you should look at. Plus, they can give you the lowdown on everything you need to know about having a second home and how it can benefit you. The same article from Bankrate says:

“Buying real estate in a new area — or even one you’ve vacationed in for many years — requires expert guidance. That makes it a good idea to work with an experienced local lender who specializes in loans for vacation homes and a local real estate professional. Local lenders and Realtors will understand the required rules and specifics for the area you are buying, and a local Realtor will know what properties are available.”

Bottom Line

If the idea of owning your own vacation home appeals to you, connect with a real estate agent.

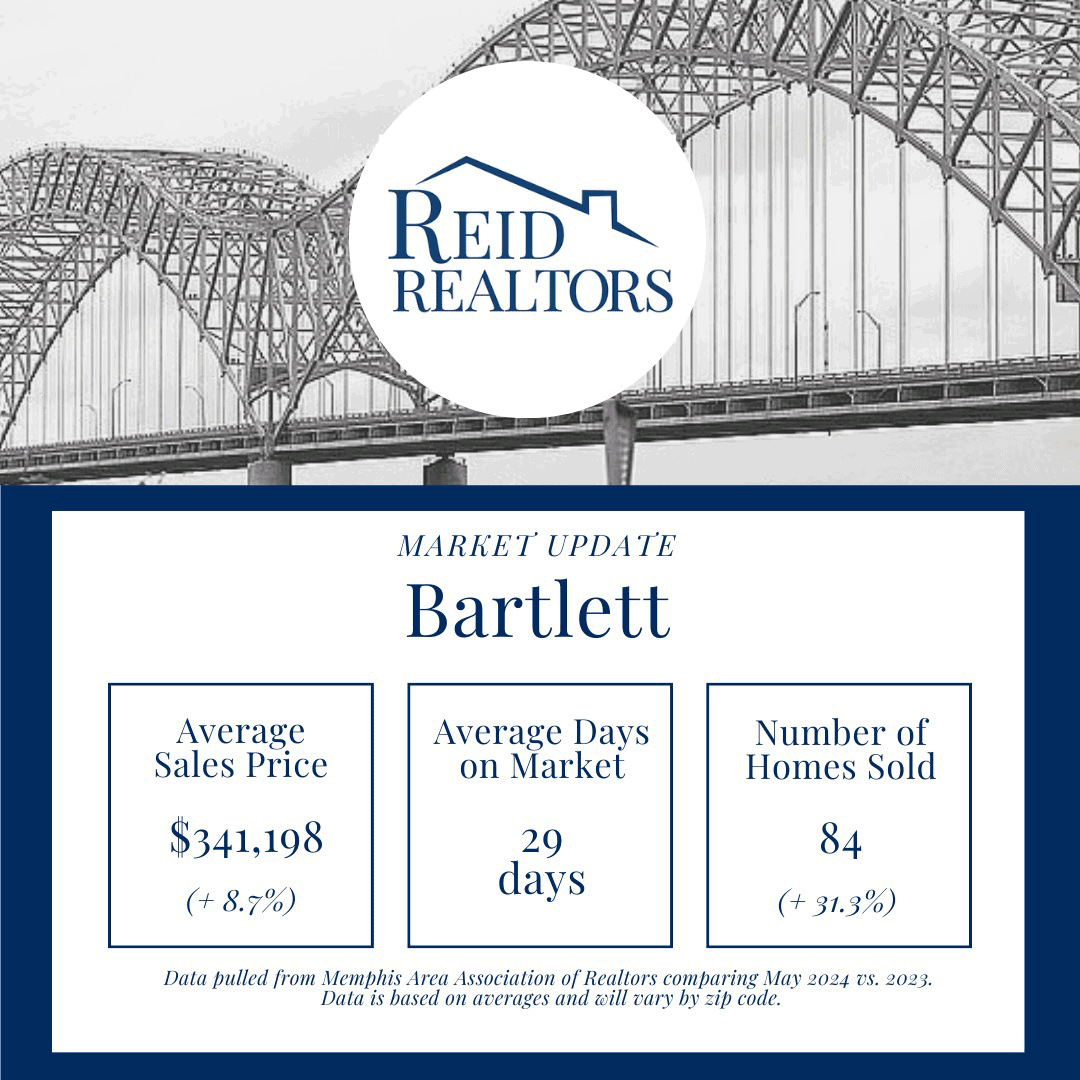

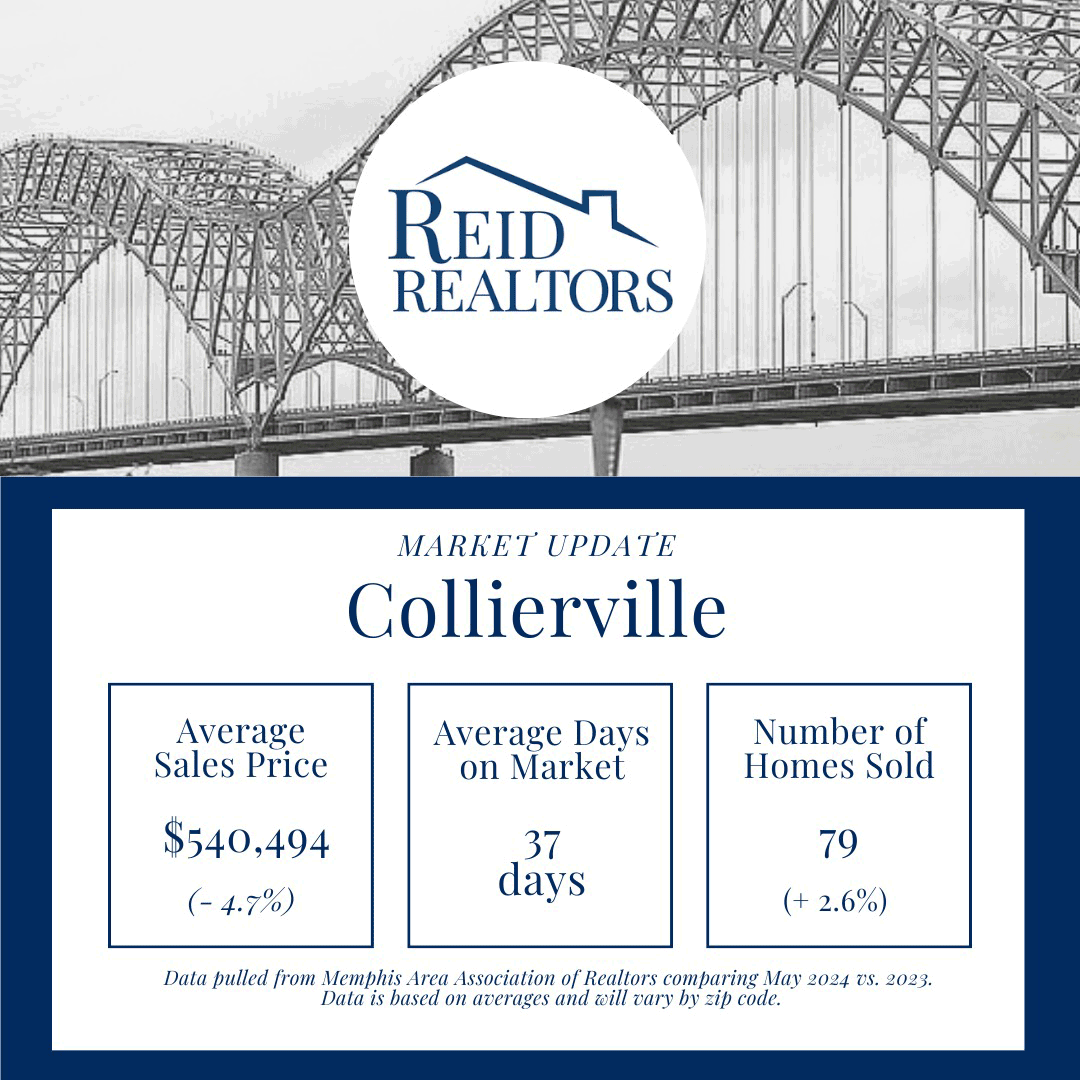

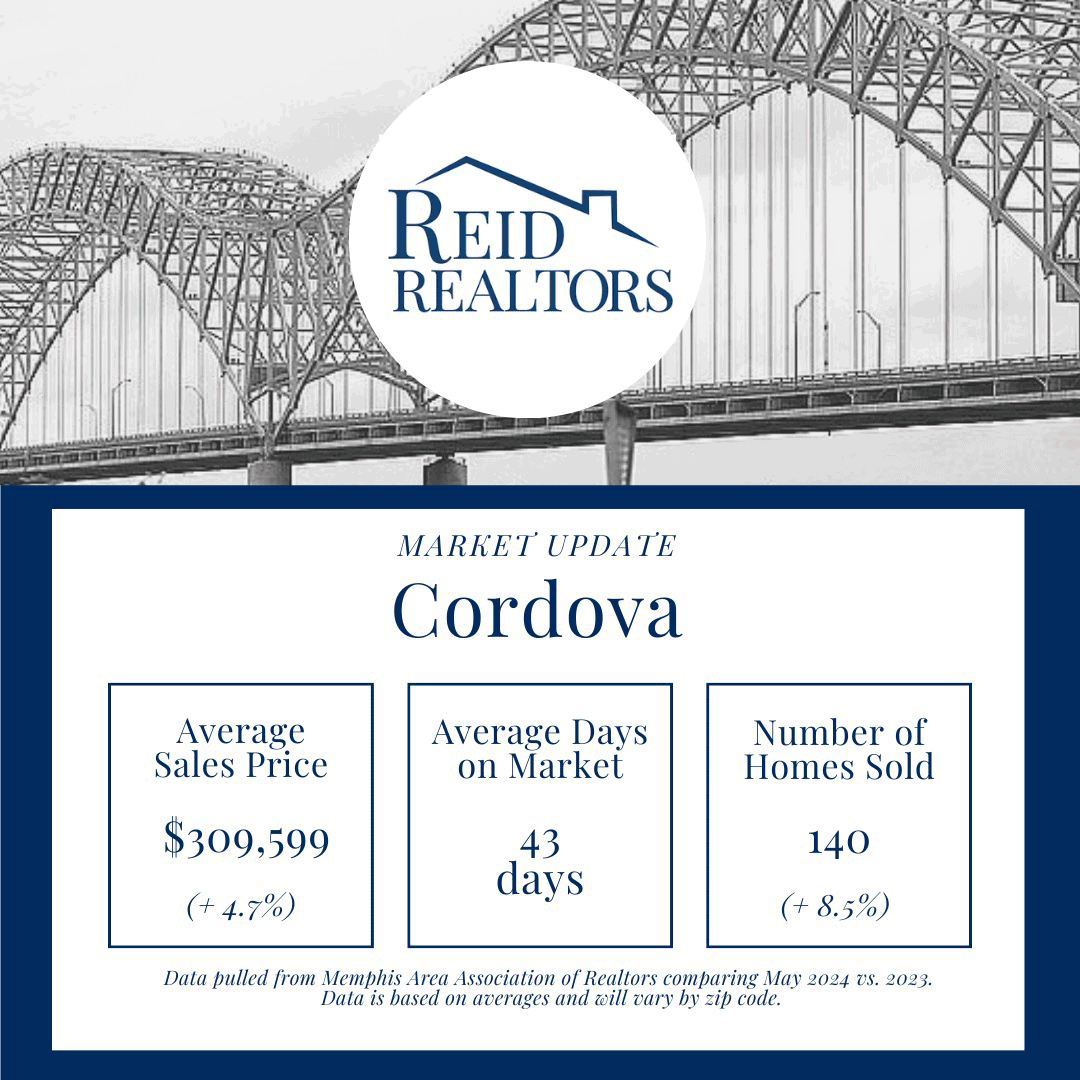

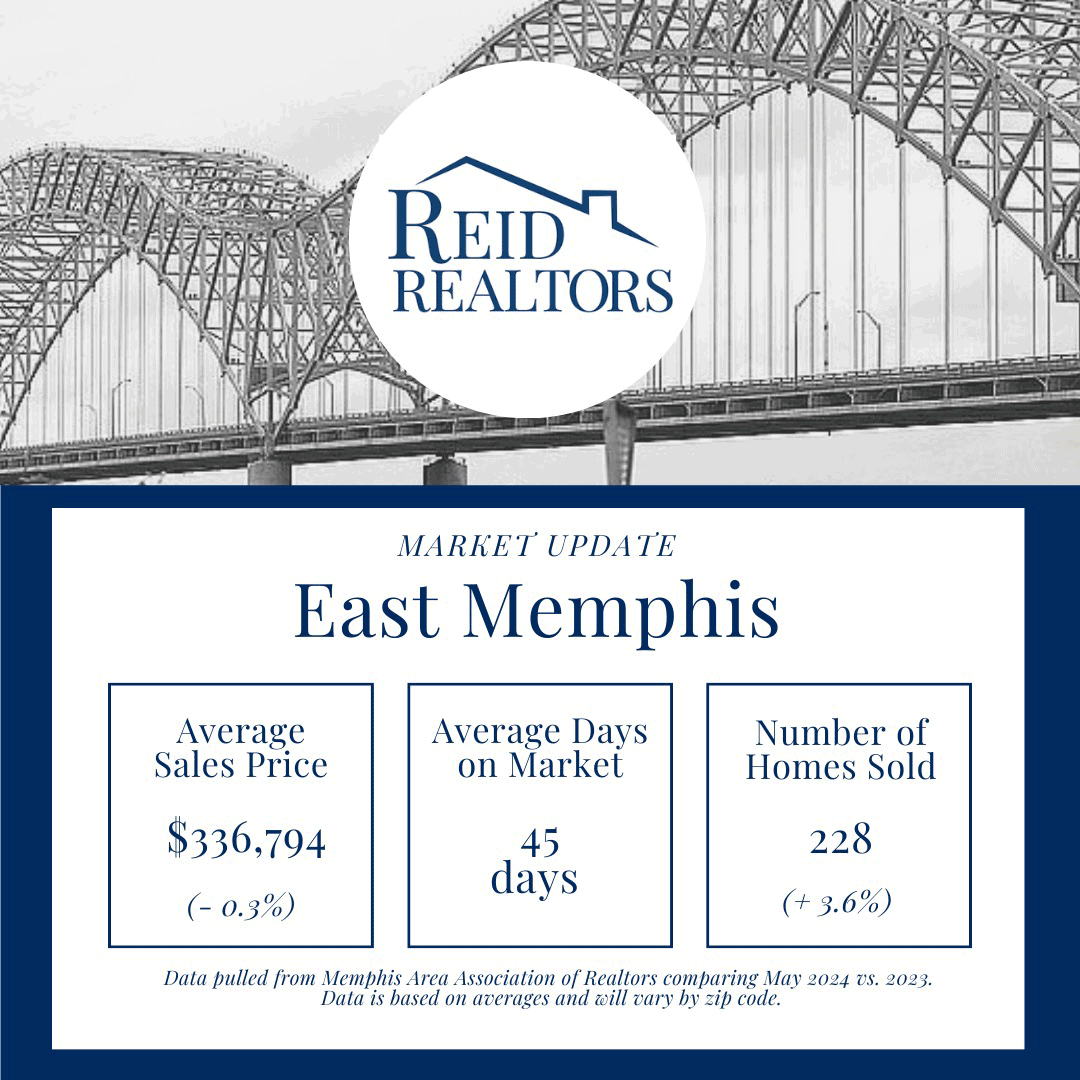

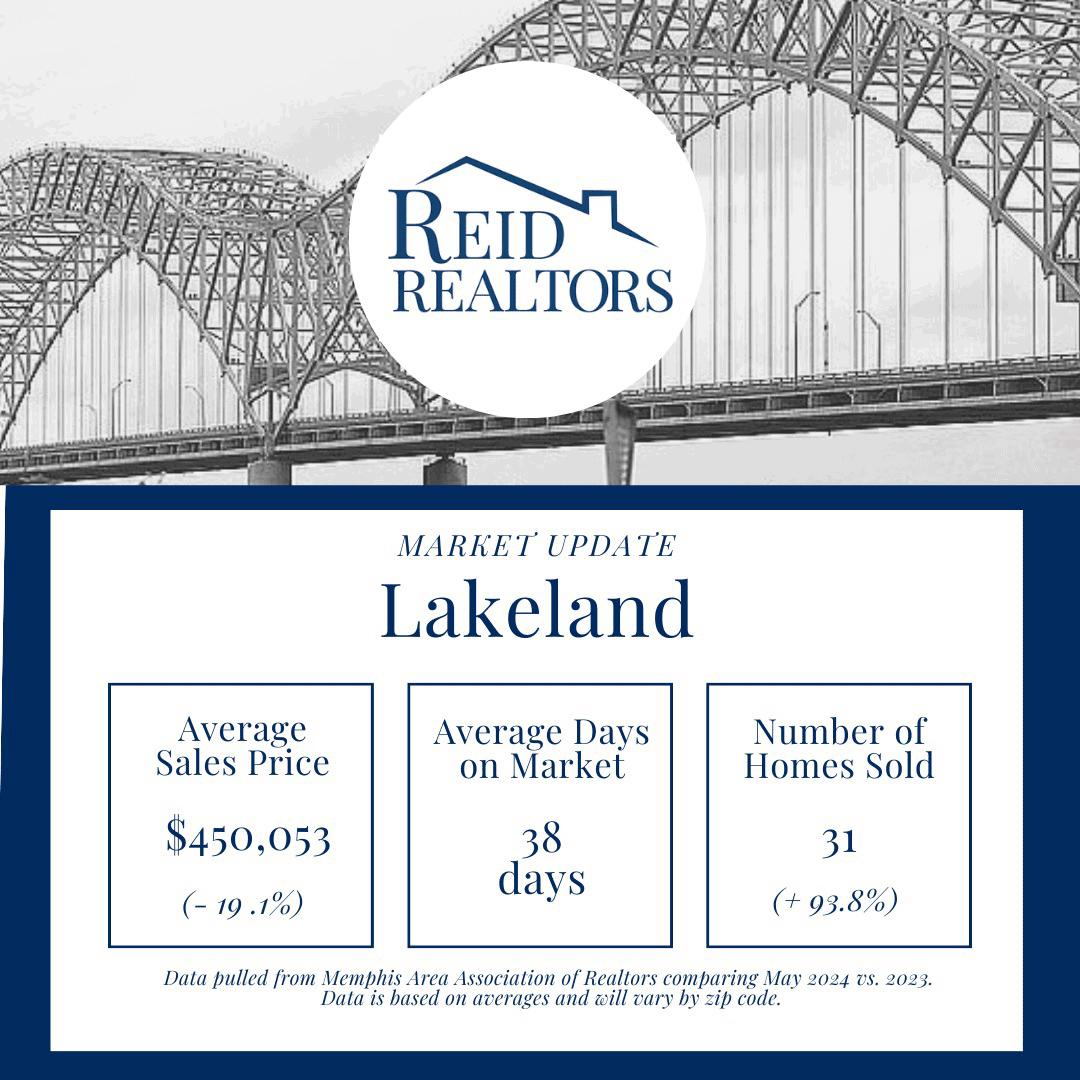

Your Real Estate Market UpdateFrom your Reid Realtors team

We’re about a month into summer break and we are feeling the heat. Not only the weather but the market has picked up. Still, there are some common themes, challenges and opportunities we want you to know about.

Here’s a few highlights:

The market overall is becoming a healthier and more stable market with home prices correcting themselves from historic highs following the pandemic.

Homes are selling but with affordability still being a top concern for buyers, homes are selling at a more conservative price point and buyers have higher expectations on move-in ready homes.

Buyers still have leverage with a smaller pool of buyers in the current market and homes sitting on the market longer.

Let’s dive into more numbers and insights below.

The Numbers

Below highlights overall themes and trends based on the Greater Memphis Area. For information by suburb, click the link below to see your area specifically.

Numbers by Market:

When comparing data Year over Year, you can see that there has been increase in homes (units) sold – up 8% in May and up 9.9% year to date. Average Sales Price in May is slightly up 4.5% but year to date is around the same YOY with just a .1% increase. As you’ll also see in our detailed report on our website, some markets are seeing average sales price remain the same or dip below years past.

We are in a healthier market.

Should home owners be concerned when seeing home values starting to normalize or the pace of growth slow down? Our short answer is no.

Real Estate has always been a longevity investment. Since 2020, the real estate market has experienced unprecedented growth and a growth rate that was not sustainable. Buying at the high end of the market in years past means weighing your options now on what renovations will or will not impact your long term ROI (return on investment), and understanding your 3-5 year real estate goals. In many cases, we see younger families moving more but it may be wise to wait for your home to appreciate in value over the next few years.

However, we understand that life happens. Dreams don’t wait and moving needs or desires may find you moving sooner than you expected. And in this case as a seller in this market, here’s more on what you can expect.

Pricing & staging is crucial for sellers.

If you’re considering listing your home in this market, it is now crucial to price your home correctly. Most homes that hit the market see the most activity within the first two weeks of the home being listed. If you home is overpriced, buyers will know and you may prevent showings. Conversely, if you do get showings on your home, after consulting with a professional, many buyers will not be willing to pay over market value in this market.

Once you know your home is priced correctly, staging plays a major role in getting buyers in the door and under contract. If you are willing to stage, this may also increase your starting price point depending upon any improvements made to the home. Staging can take on a variety of forms from hiring a stager, to decluttering and removing unwanted items and rearranging your items, and of course aesthetic improvements such as painting and landscaping that may be more costly but go along way.

It’s important to talk through your options with your agent to see what’s the best fit for your home and with your timeline and resources.

Pricing and staging will drive demand for your home.

Buyers have leverage.

It is certainly still a buyers market. This means that with such a small pool of buyers due to interest rates, buyers have the advantage of taking their time, waiting on the right home and taking advantage of home sitting on the market longer.

It also means buyers can be more selective, ask for repairs, and have more negotiation power on price.

There are currently 3,128 units available with an average sales price at $410,859 indicating we have a wide range of inventory in the Memphis market at both lower and higher price points. If you’d like to jump into the market, contact us and we’d be happy to help you navigate the ever-changing market.

There’s no denying it’s gotten more challenging to buy a home, especially with today’s mortgage rates and home price appreciation. And that may be one of the big reasons you’re eager to look into grants and assistance programs to see if there’s anything you qualify for that can help. But unfortunately, many homebuyers feel like they don’t know where to start.

A recent Bank of America Institute study asked prospective buyers where they lack confidence in the process and need more information. And this is what topped the list:

53% said they need help understanding homebuying grant programs.

So, here’s some information that can help you close that gap.

What Is Down Payment Assistance?

As the Mortgage Reports explains:

“Down payment assistance (DPA) programs offer loans and grants that can cover part or all of a home buyer’s down payment and closing costs. More than 2,000 of these programs are available nationwide. . . DPA programs vary by location, but many home buyers could be in line for thousands of dollars in down payment assistance if they qualify.”

And here’s some more good news. On top of all of these programs, you probably don’t need to save as much for your down payment as you think. Contrary to what you may have heard, typically you don’t have to put 20% down unless it’s specified by your loan type or lender. So, you likely don’t need to save as much upfront, and there are programs designed to make your down payment more achievable. Sounds like a win-win.

First-Time and Repeat Buyers Are Often Eligible

It’s also worth mentioning, that it’s not just first-time homebuyers that are eligible for many of these programs. That means whether you’re looking to buy your first house or your fifth, there could be an option for you. As Down PaymentResourcenotes:

“You don’t have to be a first-time buyer. Over 39% of all [homeownership] programs are for repeat homebuyers who have owned a home in the last 3 years.”

Additional Down Payment Resources That Can Help

Here are a few of the down payment assistance programs that are helping many buyers achieve their dream of homeownership, even now:

Teacher Next Door is designed to help teachers, first responders, health providers, government employees, active-duty military personnel, and Veterans reach their down payment goals.

Fannie Mae provides down payment assistance to eligible first-time homebuyers living in majority-Latino communities.

Freddie Mac also has options designed specifically for homebuyers with modest credit scores and limited funds for a down payment.

The 3By30 program lays out actionable strategies to add 3 million new Black homeowners by 2030. These programs offer valuable resources for potential buyers, making it easier to secure down payments and realize their dream of homeownership.

For Native Americans, Down Payment Resource highlights 42 U.S. homebuyer assistance programs across 14 states that ease the path to homeownership by providing support with down payments and other associated costs.

If you want more information on any of these, the best place to start is by contacting a trusted real estate professional.

They’ll be able to share more details about what may be available, including any other programs designed to serve specific professions or communities. And even if you don’t qualify for these types of programs, they can help see if there are any other federal, state, and local options available you should look into.

Bottom Line

Affordability is still a challenge, so if you’re looking to buy, you’re going to want to make sure you’re taking advantage of any and all resources available.

The best way to find out what’s out there is to connect with a team of real estate professionals, including a trusted lender and a local agent.

Chances are you’re hearing a lot about mortgage rates right now. You may even see some headlines talking about last week’s Federal Reserve (the Fed) meeting and what it means for rates. But the Fed doesn’t determine mortgage rates, even if the headlines make it sound like they do.

The truth is, mortgage rates are impacted by a lot of factors: geo-political uncertainty, inflation and the economy, and more. And trying to pin down when all those factors will line up enough for rates to come down is tricky.

That’s why it’s generally not worth it to try to time the market. There’s too much at play that you can’t control. The best thing you can do is control the controllables.

And when it comes to rates, here’s what you can influence to make your moving plans a reality.

Your Credit Score

Credit scores can play a big role in your mortgage rate. As an article from CNET explains:

“You can’t control the economic factors influencing interest rates.But you can get the best rate for your situation, and improving your credit score is the right place to start. Lenders look at your credit score to decide whether to approve you for a loan and at what interest rate. A higher credit score can help you secure a lower interest rate, maybe even better than the average.”

That’s why it’s even more important to maintain a good credit score right now. With rates where they are, you want to do what you can to get the best rate possible. If you want to focus on improving your score, your trusted loan officer can give you expert advice to help.

Your Loan Type

There are many types of loans, each offering different terms for qualified buyers. The Consumer Financial Protection Bureau (CFPB) says:

“There are several broad categories of mortgage loans, such as conventional, FHA, USDA, and VA loans. Lenders decide which products to offer, and loan types have different eligibility requirements. Rates can be significantly different depending on what loan type you choose.”

When working with your team of real estate professionals, make sure you find out what’s available for your situation and which types of loans you may qualify for.

Your Loan Term

Another factor to consider is the term of your loan. Just like with loan types, you have options. Freddie Mac says:

“When choosing the right home loan for you, it’s important to consider the loan term, which is the length of time it will take you to repay your loan before you fully own your home. Your loan term will affect your interest rate, monthly payment, and the total amount of interest you will pay over the life of the loan.”

Depending on your situation, the length of your loan can also change your mortgage rate.

Bottom Line

Remember, you can’t control what happens in the broader economy. But you can control the controllables.

Let’s connect to go over the things you can do that’ll make a difference. By being strategic with these factors, you may be able to combat today’s higher rates and lock in the lowest one you can.